Downloaded 19 times

![118_Scrap_MAY/JUNE 2015 www.scrap.org

To understand TDF’s resurgence, it’s help-

ful to recall the market conditions in 2011. The

TDF market—and the tire recycling industry as a

whole—took a “big hit” that year, a tire recycling

industry source says, due to “a variety of economic

factors at the time,” which slashed demand from

TDF’s main consuming sectors, such as cement

kilns, pulp and paper mills, and utilities. In par-

ticular, lower construction spending cut demand

for cement, prompting the closure of some kilns,

which are major consumers of TDF. “The slow-

down in construction meant we didn’t need

anywhere near as much cement, so those markets

slowed down,” Sheerin says. The recession, in

fact, had resulted in the “permanent loss of some

older cement kilns,” says Michael Blumenthal of

MarShay Inc. (Nyack, N.Y.), a scrap tire consulting

firm, and “they are never coming back.”

RMA calls TDF a “cleaner and more

economical alternative to coal,” offering a higher

Btu energy value and a lower greenhouse-gas

impact than coal. It also tends to be a lower-cost

alternative to competing fuels such as wood/bio-

mass, coal, natural gas, and petroleum coke. From

2011 to 2013, however, higher prices for compet-

ing fuels and improvements in the quality and

reliable delivery of TDF helped boost consump-

tion of the material almost 49 percent. Cement

kilns continued to be the largest TDF-consuming

sector in 2013, buying 726,000 tons (equivalent to

44.3 million tires), with their demand increasing

138 percent from 2011. Despite that jump, electric

utilities posted the strongest increase in TDF use

from 2011 to 2013, rising 260 percent, to 576,000

tons (35.2 million tires). Pulp and paper mills

increased their TDF consumption 21 percent, to

716,000 tons (43.7 million tires), but dedicated

tires-to-energy facilities reduced their demand 50

percent, to 102,000 tons (6.2 million tires), in the

two-year period. The closure of Exeter Energy’s

tires-to-energy plant in Sterling, Conn.—which

consumed 8 million to 10 million tires a year—

was a principal reason for that sector’s decline,

the tire recycling industry source says.

One positive development for TDF was a

decision in 2013 from the U.S. Environmental

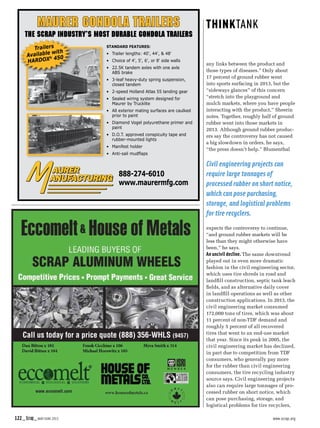

Market or Disposition 2005 2007 2009 2011 2013

Tire-Derived Fuel 2,145,000 2,484,000 2,085,000 1,427,000 2,120,000

Ground Rubber 553,000 789,000 1,354,000 929,000 975,000

Exported 112,000 102,000 102,000 302,000 246,000

Civil Engineering 640,000 562,000 285,000 295,000 172,000

Electric-Arc Furnace 19,000 27,000 27,000 66,000 66,000

Reclamation Project Unknown 133,000 130,000 54,000 49,000

Baled (with market) Unknown Unknown 28,000 2,000 30,000

Agricultural 48,000 7,000 7,000 7,000 7,000

Punched/Stamped 101,000 2,000 2,000 2,000 2,000

Total to Market 3,618,000 4,106,000 4,020,000 3,084,000 3,667,000

Total Generated 4,411,000 4,596,000 5,171,000 3,781,000 3,824,000

% to Market/Utilized 82 89 78 82 96

Baled (no market/inventoried) 42,000 9,000 16,000 33,000 No data

Landfilled 591,000 594,000 653,000 492,000 328,000

U.S. Scrap Tire Market Summary, 2005-2013*

(short tons)

Source: Rubber Manufacturers Association, 2013 U.S. Scrap Tire Management Summary.

*Totals differ slightly from RMA’s original summary due to rounding.

“If EPA had said [tire-derived fuel] was a waste material,

it would have killed the TDF market, and we would have

had the next great scrap tire crisis,” Michael Blumenthal

says. “What EPA did preserved the market.”](https://image.slidesharecdn.com/scraptiresmj2015-150611110949-lva1-app6891/85/Blumenthal-on-Scrap-Tire-Markets-2-320.jpg)

The U.S. tire recycling market experienced a robust recovery in 2013, with 96% of end-of-life tires finding beneficial use, primarily driven by a surge in tire-derived fuel (TDF) consumption. The TDF market was buoyed by improved economic conditions and significant demand from cement kilns and electric utilities, while other recycling sectors faced declines. Despite the overall industry rebound, concerns regarding health implications associated with ground rubber continued to pose challenges for non-TDF markets.