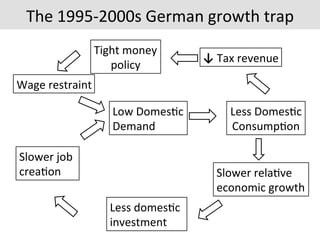

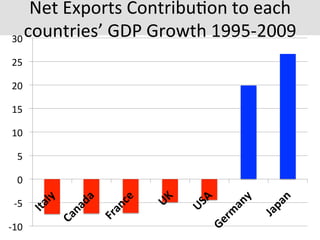

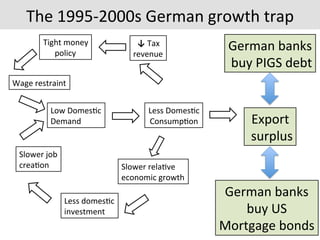

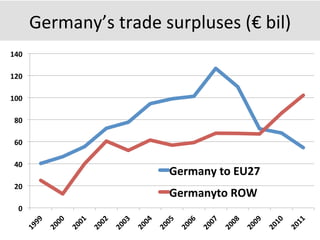

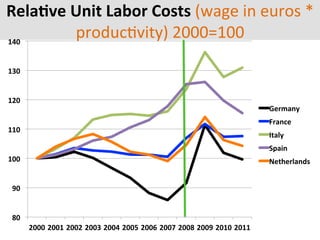

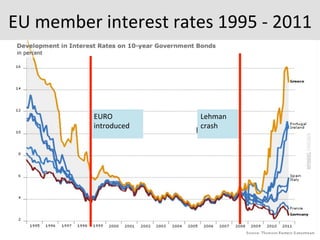

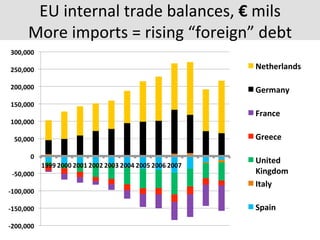

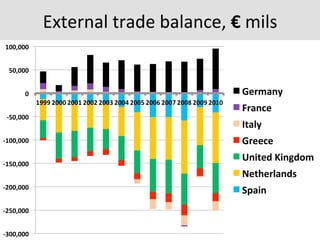

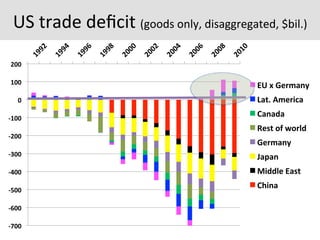

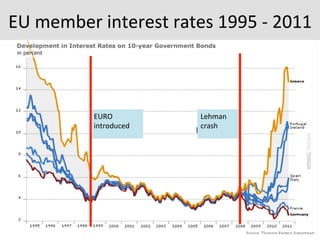

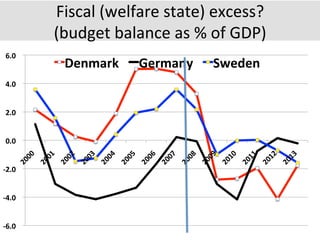

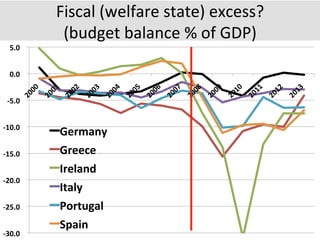

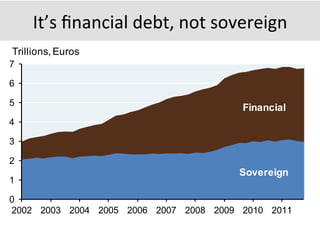

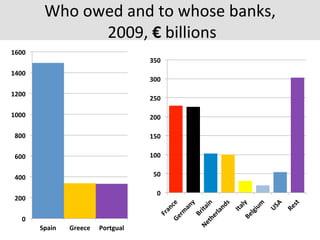

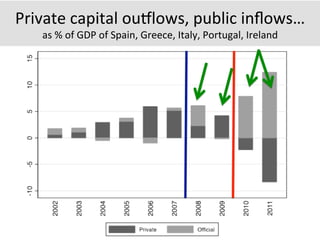

The document discusses the connections between the US financial crisis and the euro crisis in Europe. It argues that Germany's export-led growth model, which relied on wage restraint and trade surpluses, contributed to imbalances within Europe. German banks invested heavily in the debt of peripheral European countries like Greece, Spain, and Italy. When the US housing bubble burst, it exposed vulnerabilities in the global financial system and ultimately led to Europe's sovereign debt crisis.