Download as PDF, PPTX

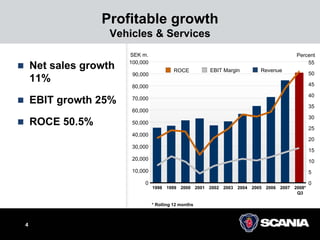

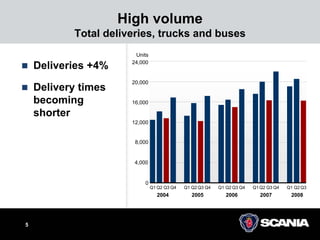

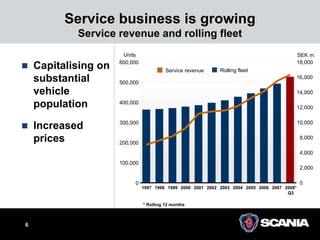

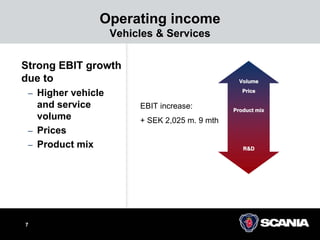

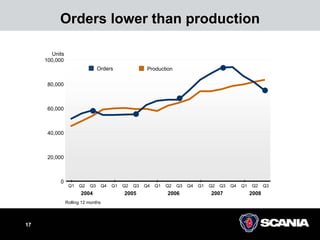

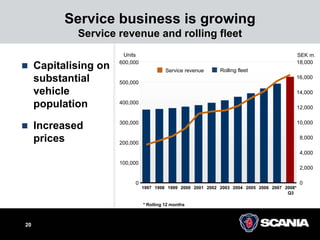

The interim report summarizes the company's performance in the first three quarters of 2008. Key highlights include operating margins reaching an all-time high of 15.8% and EBIT growth of 25%. Revenue and profitability increased due to higher vehicle and service volumes, price increases, and favorable product mix. However, order bookings for trucks have declined 51% in Western Europe and 34% in Central and Eastern Europe. While flexible production has helped, earnings forecasts for 2009 are not provided due to economic uncertainty. The service business continues growing with increased traffic and workshop utilization.