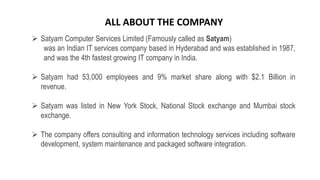

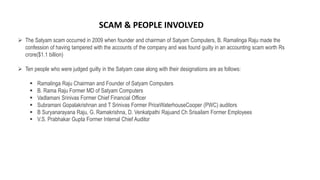

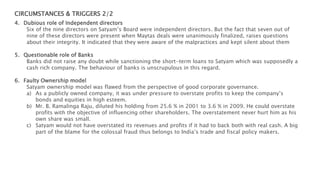

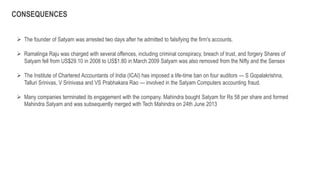

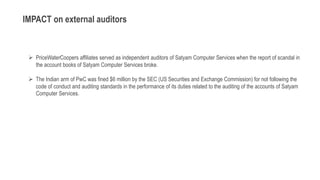

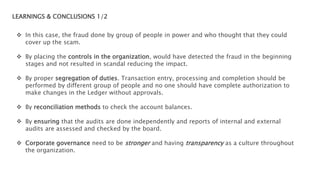

Satyam Computer Services was an Indian IT company established in 1987 that grew to be the 4th largest IT company in India. In 2009, it was discovered that the founder had falsified the company's accounts for 9 years, overstating revenues and profits. The accounting fraud, valued at $1.1 billion, led to the arrest of the founder. The scandal severely damaged investor confidence and Satyam was acquired by Tech Mahindra. The auditors involved also faced penalties for not detecting the fraud. The scandal highlighted the need for stronger corporate governance and internal controls in Indian companies.