Download free for 30 days

Sign in

Upload

Language (EN)

Support

Business

Mobile

Social Media

Marketing

Technology

Art & Photos

Career

Design

Education

Presentations & Public Speaking

Government & Nonprofit

Healthcare

Internet

Law

Leadership & Management

Automotive

Engineering

Software

Recruiting & HR

Retail

Sales

Services

Science

Small Business & Entrepreneurship

Food

Environment

Economy & Finance

Data & Analytics

Investor Relations

Sports

Spiritual

News & Politics

Travel

Self Improvement

Real Estate

Entertainment & Humor

Health & Medicine

Devices & Hardware

Lifestyle

Change Language

Language

English

Español

Português

Français

Deutsche

Cancel

Save

Submit search

EN

Uploaded by

AnangSubardjo2

PPTX, PDF

15 views

Romney Accounting Information System Ed 15

Romney Accounting Information System Ed 15

Business

◦

Read more

0

Save

Share

Embed

Embed presentation

Download

Download to read offline

1

/ 26

2

/ 26

3

/ 26

4

/ 26

5

/ 26

6

/ 26

7

/ 26

8

/ 26

9

/ 26

10

/ 26

11

/ 26

12

/ 26

13

/ 26

14

/ 26

15

/ 26

16

/ 26

17

/ 26

18

/ 26

19

/ 26

20

/ 26

21

/ 26

22

/ 26

23

/ 26

24

/ 26

25

/ 26

26

/ 26

More Related Content

PPTX

Romney accounting information system ch 01

by

YoseAtTheKahyangan

PPTX

Accounting Information System Romney_15e_accessible_fullppt_01.pptx

by

AleaHuero1

PPTX

Romney_15e_accessible_fullppt_01.pptx

by

adilkazuto

PDF

Romney_15e_accessible_fullppt_01_accessible.pdf

by

anhhoang31231025466

PPTX

romney_ais14_stppt_01.pptx_SIA week 1_upload

by

rarasavitri843

PPTX

ppt romney ais keren banget pokoknya keren deh

by

aryandanil

PPTX

LECTURE ONE(1) for accounting information

by

ShaibuAlhassan2

PPTX

Chapter 1

by

Dr. Muath Asmar

Romney accounting information system ch 01

by

YoseAtTheKahyangan

Accounting Information System Romney_15e_accessible_fullppt_01.pptx

by

AleaHuero1

Romney_15e_accessible_fullppt_01.pptx

by

adilkazuto

Romney_15e_accessible_fullppt_01_accessible.pdf

by

anhhoang31231025466

romney_ais14_stppt_01.pptx_SIA week 1_upload

by

rarasavitri843

ppt romney ais keren banget pokoknya keren deh

by

aryandanil

LECTURE ONE(1) for accounting information

by

ShaibuAlhassan2

Chapter 1

by

Dr. Muath Asmar

Similar to Romney Accounting Information System Ed 15

PDF

Accounting Information Systems 13Th Chapter 1

by

Don Dooley

PPTX

unit-1 ppt.pptx for management for MBA students for information

by

khyatishah223526

PDF

Ais section ch1

by

Zakaria Hasaneen

PPT

Accpounting for Information Systems Fraud Error

by

meize1

PPT

Ppt 01 ge

by

habtamu hailemariam

PPTX

AIS Chapter 01 Overview Accounting Information System

by

ArisSuryaPutra1

PDF

(eBook PDF) AYB221 Acc Systems and Tech CB

by

pepciujanega

PPT

CH 01 AIS-part 1.ppt

by

ssuser81be21

PDF

(eBook PDF) AYB221 Acc Systems and Tech CB

by

ojnuvtnb034

PDF

(eBook PDF) AYB221 Acc Systems and Tech CB

by

talajachot

PDF

(eBook PDF) AYB221 Acc Systems and Tech CB

by

elecromonii

PPTX

laudonmis17pptch01 Introduction to MIS.pptx

by

IgoFebrianto1

PDF

RS_AIS_ch1.pdf - Mengenal SIA - Introduction to AIS

by

spr4yit

PDF

Solution Manual for Accounting Information Systems 11th Edition by Bodnar

by

nguemrochow

PPTX

Essentials of MIS Chapter 1 Lauden and Lauden

by

AliDashti35

PPTX

Essentials of MIS Chapter 2 Lauden and Lauden

by

AliDashti35

PPT

Intro to Information Systems

by

tclanton4

PDF

AIS 15th edition Marshall B. Romney, 2022.pdf

by

ErlianaBanjarnahor1

PPTX

Introduction to Information Systems and People

by

eXtaS15

PPTX

FY bms ch1.pptx INFORMATION TECHNOLOGY IN BUSINESS MANAGEMENT

by

pushkarpssingh

Accounting Information Systems 13Th Chapter 1

by

Don Dooley

unit-1 ppt.pptx for management for MBA students for information

by

khyatishah223526

Ais section ch1

by

Zakaria Hasaneen

Accpounting for Information Systems Fraud Error

by

meize1

Ppt 01 ge

by

habtamu hailemariam

AIS Chapter 01 Overview Accounting Information System

by

ArisSuryaPutra1

(eBook PDF) AYB221 Acc Systems and Tech CB

by

pepciujanega

CH 01 AIS-part 1.ppt

by

ssuser81be21

(eBook PDF) AYB221 Acc Systems and Tech CB

by

ojnuvtnb034

(eBook PDF) AYB221 Acc Systems and Tech CB

by

talajachot

(eBook PDF) AYB221 Acc Systems and Tech CB

by

elecromonii

laudonmis17pptch01 Introduction to MIS.pptx

by

IgoFebrianto1

RS_AIS_ch1.pdf - Mengenal SIA - Introduction to AIS

by

spr4yit

Solution Manual for Accounting Information Systems 11th Edition by Bodnar

by

nguemrochow

Essentials of MIS Chapter 1 Lauden and Lauden

by

AliDashti35

Essentials of MIS Chapter 2 Lauden and Lauden

by

AliDashti35

Intro to Information Systems

by

tclanton4

AIS 15th edition Marshall B. Romney, 2022.pdf

by

ErlianaBanjarnahor1

Introduction to Information Systems and People

by

eXtaS15

FY bms ch1.pptx INFORMATION TECHNOLOGY IN BUSINESS MANAGEMENT

by

pushkarpssingh

Recently uploaded

DOCX

_18 Buying USA LinkedIn Accounts Can Boost Your Social.docx

by

timofeyzhuravlev1

DOCX

_Buy Old Gmail Accounts with Real Age and Trust with 2fa

by

pvasmmpath

PDF

Artificial Intelligence and the Great Divergence, a report by the White House

by

Chris Skinner

DOCX

Why Should I Buy Old Gmail Accounts_losangeless _______________.docx

by

joshuabellc7

DOCX

How to Buy Facebook Verified Accounts_ A Guide.docx

by

Digital Marketing in the USA

DOCX

Top 10 Sites to Buy Aged Snapchat Accounts in 2026.docx

by

BuyGmailAccounts10

PPTX

Thermal Energy International - TMG - Q2 2026 Earnings Call

by

Marketing847413

PDF

Raman Bhaumik - A Licensed Pharmacist In Multiple States

by

Raman Bhaumik

DOCX

Top 7 Site To Buy Verified OnlyFans Creator Accounts In 2026.docx

by

rcx255gljjv5jo2oh3tv

DOCX

How to Buy Apple ID Accounts in 2026.docx

by

Digital Marketing in the USA

PDF

Where to Buy Gmail Accounts Online: A 2026 Guide

by

usaseoshops

PDF

How to Buying Old Gmail Accounts That Are Aged and Low-Cost_.pdf

by

https://propvaservice.com/product/buy-old-gmail-accounts/

PDF

Dr. Michael T. Conner - Serves As CEO

by

Dr. Michael T. Conner

PPTX

Explore Hubspot’s Customer Agent for B2B

by

Boundify

DOCX

Buy Verified PayPal Accounts for Secure Online Use docx

by

mugdhobiswas17

PDF

Startup 8 - Student's Book - ENGLISH - Advanced 2

by

englishcloudresource

DOCX

Buy Old Gmail Account _A Step by Step Guide Best 5 Site Usa.docx

by

pvatopone77

PDF

Using-pension-savings-to-support-home-ownership.pdf

by

Henry Tapper

PDF

Kirill Klip GEM Royalty TNR Gold Copper Presentation

by

Kirill Klip

DOCX

Buy Verified PayPal Account Online_ A Comprehensive ....docx

by

Business

_18 Buying USA LinkedIn Accounts Can Boost Your Social.docx

by

timofeyzhuravlev1

_Buy Old Gmail Accounts with Real Age and Trust with 2fa

by

pvasmmpath

Artificial Intelligence and the Great Divergence, a report by the White House

by

Chris Skinner

Why Should I Buy Old Gmail Accounts_losangeless _______________.docx

by

joshuabellc7

How to Buy Facebook Verified Accounts_ A Guide.docx

by

Digital Marketing in the USA

Top 10 Sites to Buy Aged Snapchat Accounts in 2026.docx

by

BuyGmailAccounts10

Thermal Energy International - TMG - Q2 2026 Earnings Call

by

Marketing847413

Raman Bhaumik - A Licensed Pharmacist In Multiple States

by

Raman Bhaumik

Top 7 Site To Buy Verified OnlyFans Creator Accounts In 2026.docx

by

rcx255gljjv5jo2oh3tv

How to Buy Apple ID Accounts in 2026.docx

by

Digital Marketing in the USA

Where to Buy Gmail Accounts Online: A 2026 Guide

by

usaseoshops

How to Buying Old Gmail Accounts That Are Aged and Low-Cost_.pdf

by

https://propvaservice.com/product/buy-old-gmail-accounts/

Dr. Michael T. Conner - Serves As CEO

by

Dr. Michael T. Conner

Explore Hubspot’s Customer Agent for B2B

by

Boundify

Buy Verified PayPal Accounts for Secure Online Use docx

by

mugdhobiswas17

Startup 8 - Student's Book - ENGLISH - Advanced 2

by

englishcloudresource

Buy Old Gmail Account _A Step by Step Guide Best 5 Site Usa.docx

by

pvatopone77

Using-pension-savings-to-support-home-ownership.pdf

by

Henry Tapper

Kirill Klip GEM Royalty TNR Gold Copper Presentation

by

Kirill Klip

Buy Verified PayPal Account Online_ A Comprehensive ....docx

by

Business

Romney Accounting Information System Ed 15

1.

Accounting Information Systems Fifteenth

Edition Chapter 1 Accounting Information Systems: An Overview Copyright © 2021, 2018, 2015 Pearson Education, Inc. All Rights Reserved

2.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Learning Objectives • Distinguish between data and information: – Discuss the characteristics of useful information. – Explain how to determine the value of information. • Explain the decisions an organization makes: – The information needed to make them. – The major business processes present in most companies. • Explain how an AI S adds value to an organization: – How it affects and is affected by corporate strategy. – The role of AI S in a value chain.

3.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Distinguishing Between Data and Information • Data are facts collected, recorded, and stored in the system – A fact could be a number, date, name, and so on. For example: 2/22/14 AB C Company 123, 99, 3, 20, 60

4.

Copyright © 2021,

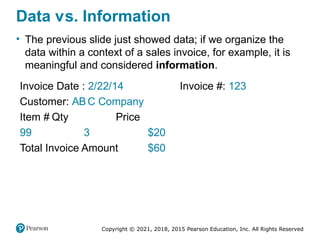

2018, 2015 Pearson Education, Inc. All Rights Reserved Data versus. Information • The previous slide just showed data; if we organize the data within a context of a sales invoice, for example, it is meaningful and considered information. Invoice Date : 2/22/14 Invoice #: 123 Customer: ABC Company Item # Qty Price 99 3 $20 Total Invoice Amount $60

5.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Decision Quality • Information helps us make better decisions. • Too much information causing information overload can reduce decision quality. • Information Technology (I T) is used to help decision makers more effectively filter and condense information.

6.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Value of Information • Information is valuable when the benefits exceed the costs of gathering, maintaining, and storing the data. Benefit (i.e., improved decision making) - Cost (i.e., time and resources used to get the information) = value of information

7.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved What Makes Information Useful? (1 of 2) There are 14 general characteristics that make information useful: 1. Access restricted: limit access to authorized parties 2. Accurate: accurate, correct, and free of error 3. Available: available to users when needed 4. Reputable: perceived as true and credible 5. Complete: does not omit important aspects of events or activities 6. Concise: clear, succinct, brief, but comprehensive 7. Consistent: presented in the same format over time

8.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved What Makes Information Useful? (2 of 2) 8. Current: up to the present data and time 9. Objective: unbiased, unprejudiced, and impartial 10.Relevant: reduces uncertainty and improves decision making 11.Timely: provided in time for decision maker to make decisions 12.Useable: easy to use for different task 13.Understandable: easily comprehended and interpreted 14.Verifiable: two independent people can produce the same information

9.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Machine-Readable Format • Data is most useful when it is in a machine-readable format that can be read and processed by a computer. • XBR L is an example of a machine-readable format that can improve many of the characteristics that make information useful.

10.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Information Needs and Business Processes • Business organizations use business processes to get things done. A business process is a set of related, coordinated, and structured activities and tasks performed by people, machines, or both to achieve a specific organizational goal. • Key decisions and information needed often come from these business processes.

11.

Copyright © 2021,

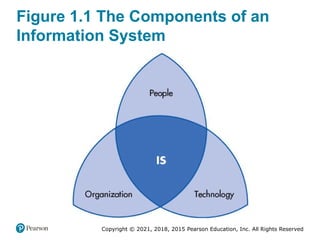

2018, 2015 Pearson Education, Inc. All Rights Reserved Figure 1.1 The Components of an Information System

12.

Copyright © 2021,

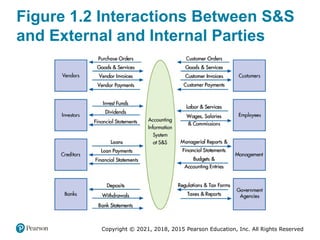

2018, 2015 Pearson Education, Inc. All Rights Reserved Transactional Information Between Internal and External Parties in an AIS • Business organizations conduct business transactions, which is an agreement between two entities to exchange goods, services, or any other event that can be measured in economic terms by an organization. • Transaction data is used to create financial statements and is called transaction processing. • The flow of information between these users for the various business activities involves a give-get exchange grouped into business processes or transaction cycles.

13.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Figure 1.2 Interactions Between S&S and External and Internal Parties

14.

Copyright © 2021,

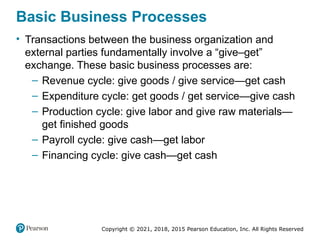

2018, 2015 Pearson Education, Inc. All Rights Reserved Basic Business Processes • Transactions between the business organization and external parties fundamentally involve a “give–get” exchange. These basic business processes are: – Revenue cycle: give goods / give service—get cash – Expenditure cycle: get goods / get service—give cash – Production cycle: give labor and give raw materials— get finished goods – Payroll cycle: give cash—get labor – Financing cycle: give cash—get cash

15.

Copyright © 2021,

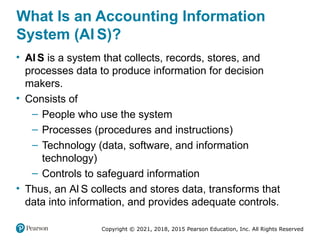

2018, 2015 Pearson Education, Inc. All Rights Reserved What Is an Accounting Information System (AI S)? • AI S is a system that collects, records, stores, and processes data to produce information for decision makers. • Consists of – People who use the system – Processes (procedures and instructions) – Technology (data, software, and information technology) – Controls to safeguard information • Thus, an AI S collects and stores data, transforms that data into information, and provides adequate controls.

16.

Copyright © 2021,

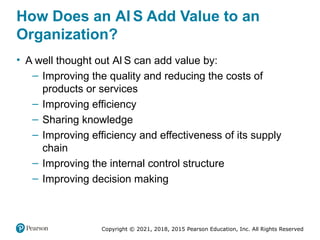

2018, 2015 Pearson Education, Inc. All Rights Reserved How Does an AI S Add Value to an Organization? • A well thought out AI S can add value by: – Improving the quality and reducing the costs of products or services – Improving efficiency – Sharing knowledge – Improving efficiency and effectiveness of its supply chain – Improving the internal control structure – Improving decision making

17.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Artificial Intelligence • Artificial intelligence (AI) is the use of computer systems to simulate human intelligence processes such as learning, reasoning, and self-improvement. • AI can be used in the following fields – Business – Education – Finance – Healthcare

18.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Data Analytics • Data analytics is the use of software and algorithms to find and solve problems and improve business performance. • Analytics can help improve decision making by – Identifying a problem/issue for management to resolve. – Collecting the data needed to solve the problem, analyze it, and make recommendations to management on how to resolve it. – Integrating actionable insights into the systems used to make decisions.

19.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Blockchain • Blockchain represents individual digital records, called blocks, linked together using cryptography in a single list, called a chain. • Blockchain has several significant advantages, including – accuracy, transparency, data consistency, trust, – no need for third parties, single set of books, reduced cost, – decentralization, efficiency, privacy, security, and provenance • There are also significant challenges to its adoption including political and regulatory issues.

20.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Cloud Computing, Virtualization, and the Internet of Things • Cloud computing is the use of a browser to remotely access software, data storage, hardware, and applications. • Virtualization is the running of multiple systems simultaneously on one physical computer. • Internet of Things (IoT) refers to the embedding of sensors in a multitude of devices (lights, heating and air conditioning, appliances, etc.) so that those devices can now connect to the Internet.

21.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved AI S and Corporate Strategy • An AI S is influenced by an organization’s strategy. • A strategy is the overall goal the organization hopes to achieve (e.g., increase profitability). • Once an overall goal is determined, an organization can determine actions needed to reach their goal and identify the informational requirements (both financial and nonfinancial) necessary to measure how well they are doing in obtaining that goal.

22.

Copyright © 2021,

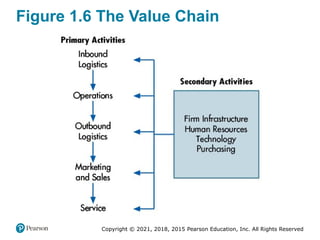

2018, 2015 Pearson Education, Inc. All Rights Reserved AI S in the Value Chain • The value chain links together the different activities within an organization that provide value to the customer. – Value chain activities are primary and support activities. Primary activities provide direct value to the customer. Support activities enable primary activities to be efficient and effective. • A supply chain is an extended system that includes the organization’s value chain as well as its suppliers, distributors, and customers.

23.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Figure 1.6 The Value Chain

24.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Key Terms (1 of 2) • System • Goal conflict • Goal congruence • Data • Information • Machine-readable • Information overload • Information technology (I T) • Value of information • Information system • Business process • Transaction • Transaction processing • Give-get exchange • Business processes or transaction cycles • Revenue cycle • Expenditure cycle • Production or conversion cycle • Human resource/payroll cycle • Financing cycle • General ledger and reporting system • Accounting information system (AI S) • Accounting • Artificial intelligence

25.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Key Terms (2 of 2) • Data analytics • Data dashboard • Blockchain • Virtualization • Cloud computing • Internet of Things (IoT) • Value chain • Primary activities • Support activities • Supply chain

26.

Copyright © 2021,

2018, 2015 Pearson Education, Inc. All Rights Reserved Copyright This work is protected by United States copyright laws and is provided solely for the use of instructors in teaching their courses and assessing student learning. Dissemination or sale of any part of this work (including on the World Wide Web) will destroy the integrity of the work and is not permitted. The work and materials from it should never be made available to students except by instructors using the accompanying text in their classes. All recipients of this work are expected to abide by these restrictions and to honor the intended pedagogical purposes and the needs of other instructors who rely on these materials.

Download