Recommended

PPT

PPTX

Romney_15e_accessible_fullppt_01.pptx

PPTX

Romney accounting information system ch 01

PPTX

LECTURE ONE(1) for accounting information

PPTX

ppt romney ais keren banget pokoknya keren deh

PDF

Romney_15e_accessible_fullppt_01_accessible.pdf

PPTX

romney_ais14_stppt_01.pptx_SIA week 1_upload

PPTX

PPTX

AIS Chapter 01 Overview Accounting Information System

PPTX

Accounting Information System Romney_15e_accessible_fullppt_01.pptx

PPTX

Romney Accounting Information System Ed 15

PPT

Accounting Information Systems(AIS)

PPT

AIS CH_01 Accounting Information Systems an overview.PPT

PPTX

The information system: An accountant's perspective

PPT

CH 1.ppt,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,

PPT

IntroductionAccountingInformationSystems.ppt

PDF

RS_AIS_ch1.pdf - Mengenal SIA - Introduction to AIS

PPT

Accounting Information Systems; Basic Concept

PDF

(eBook PDF) AYB221 Acc Systems and Tech CB

PDF

(eBook PDF) AYB221 Acc Systems and Tech CB

PPT

Ais Romney 2006 Slides 01 Overview

PDF

(eBook PDF) AYB221 Acc Systems and Tech CB

PDF

Accounting Information Systems 13Th Chapter 1

PDF

PPT

PPT

PDF

PPT

PDF

19 January 2026 Andreas Schleicher Digital Education Outlook 2026.pdf

PPTX

Activity on Job position in Odoo 19 Recruitment

More Related Content

PPT

PPTX

Romney_15e_accessible_fullppt_01.pptx

PPTX

Romney accounting information system ch 01

PPTX

LECTURE ONE(1) for accounting information

PPTX

ppt romney ais keren banget pokoknya keren deh

PDF

Romney_15e_accessible_fullppt_01_accessible.pdf

PPTX

romney_ais14_stppt_01.pptx_SIA week 1_upload

PPTX

Similar to Accpounting for Information Systems Fraud Error

PPTX

AIS Chapter 01 Overview Accounting Information System

PPTX

Accounting Information System Romney_15e_accessible_fullppt_01.pptx

PPTX

Romney Accounting Information System Ed 15

PPT

Accounting Information Systems(AIS)

PPT

AIS CH_01 Accounting Information Systems an overview.PPT

PPTX

The information system: An accountant's perspective

PPT

CH 1.ppt,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,

PPT

IntroductionAccountingInformationSystems.ppt

PDF

RS_AIS_ch1.pdf - Mengenal SIA - Introduction to AIS

PPT

Accounting Information Systems; Basic Concept

PDF

(eBook PDF) AYB221 Acc Systems and Tech CB

PDF

(eBook PDF) AYB221 Acc Systems and Tech CB

PPT

Ais Romney 2006 Slides 01 Overview

PDF

(eBook PDF) AYB221 Acc Systems and Tech CB

PDF

Accounting Information Systems 13Th Chapter 1

PDF

PPT

PPT

PDF

PPT

Recently uploaded

PDF

19 January 2026 Andreas Schleicher Digital Education Outlook 2026.pdf

PPTX

Activity on Job position in Odoo 19 Recruitment

PPTX

Accounting Theory Group Presentation - Why Study Accounting Theory

PDF

Types of Artificial Intelligence: Capabilities and Functionality Explained

PDF

BÀI GIẢNG POWERPOINT CHÍNH KHÓA PHIÊN BẢN AI TIẾNG ANH 6 CẢ NĂM, THEO TỪNG BÀ...

PDF

GIÁO ÁN KẾ HOẠCH BÀI DẠY NĂNG LỰC SỐ MÔN TIẾNG ANH LỚP 11 CẢ NĂM - GLOBAL SUC...

PPTX

special senses-eye, ear, nose, tongue.pptx

PPTX

How to create Article in Odoo 18 Knowledge App

PPTX

NMR Spectroscopy: Principles and Applications

PPTX

Contract Act 1872 - Sections 10, 11 13-by Judge Nazmul Hasan.pptx

PPTX

Insertion of Suppositories..........pptx

PPTX

ANTISEPTICS AND DISINFECTANTS CHAPTER NO.05.pptx

PDF

Geography unit 7-Population-Distribution`.pdf

PDF

ĐỀ MINH HỌA KỲ THI TỐT NGHIỆP TRUNG HỌC PHỔ THÔNG NĂM 2026 MÔN TIẾNG ANH 2026...

PPTX

The Creation Pattern Physical Health.pptx

PPTX

VITAMINS CHAPTER NO.05 PHARMACOGNOSY D. PHARMACY

PPTX

Pneumonia, Social and Preventive Pharmacy .pptx

PPTX

YSPH VMOC Special Report - Measles - The Americas 1-18-2026

PDF

RPT FORM 1 English (2026 academic session) SMKTS.pdf

PPTX

Nanomaterials and its types - Dr.M.Jothimuniyandi

Accpounting for Information Systems Fraud Error 1. 2. Learning Objectives

Distinguish between data and information.

Discuss the characteristics of useful information.

Explain how to determine the value of information.

Explain the decisions an organization makes and the information needed to make them.

Identify the information that passes between internal and external parties and an AIS.

Describe the major business processes present in most companies.

Explain what an accounting information system (AIS) is and describe its basic functions.

Discuss how an AIS can add value to an organization.

Explain how an AIS and corporate strategy affect each other.

Explain the role an AIS plays in a company’s value chain.

Copyright © 2012 Pearson Education 1-2

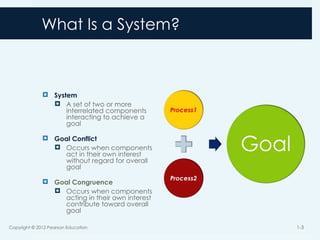

3. What Is a System?

System

A set of two or more

interrelated components

interacting to achieve a

goal

Goal Conflict

Occurs when components

act in their own interest

without regard for overall

goal

Goal Congruence

Occurs when components

acting in their own interest

contribute toward overall

goal

Copyright © 2012 Pearson Education 1-3

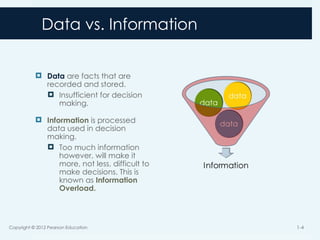

4. Data vs. Information

Data are facts that are

recorded and stored.

Insufficient for decision

making.

Information is processed

data used in decision

making.

Too much information

however, will make it

more, not less, difficult to

make decisions. This is

known as Information

Overload.

Copyright © 2012 Pearson Education 1-4

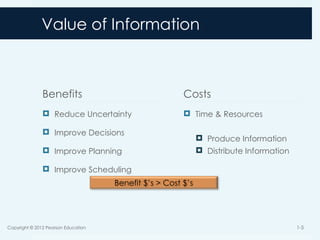

5. Value of Information

Benefits

Reduce Uncertainty

Improve Decisions

Improve Planning

Improve Scheduling

Costs

Time & Resources

Produce Information

Distribute Information

1-5

Benefit $’s > Cost $’s

Copyright © 2012 Pearson Education

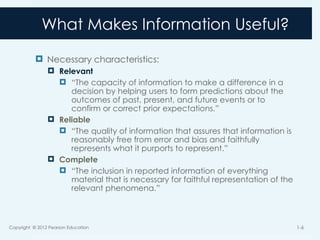

6. What Makes Information Useful?

Necessary characteristics:

Relevant

“The capacity of information to make a difference in a

decision by helping users to form predictions about the

outcomes of past, present, and future events or to

confirm or correct prior expectations.”

Reliable

“The quality of information that assures that information is

reasonably free from error and bias and faithfully

represents what it purports to represent.”

Complete

“The inclusion in reported information of everything

material that is necessary for faithful representation of the

relevant phenomena.”

Copyright © 2012 Pearson Education 1-6

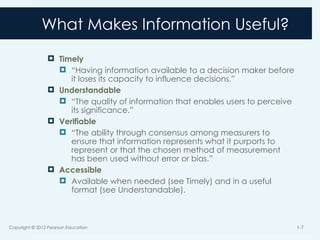

7. What Makes Information Useful?

Timely

“Having information available to a decision maker before

it loses its capacity to influence decisions.”

Understandable

“The quality of information that enables users to perceive

its significance.”

Verifiable

“The ability through consensus among measurers to

ensure that information represents what it purports to

represent or that the chosen method of measurement

has been used without error or bias.”

Accessible

Available when needed (see Timely) and in a useful

format (see Understandable).

Copyright © 2012 Pearson Education 1-7

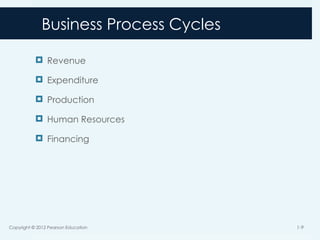

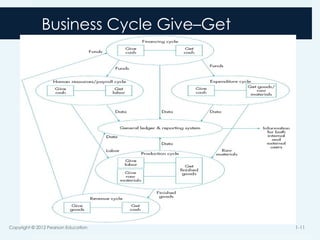

8. 9. Business Process Cycles

Revenue

Expenditure

Production

Human Resources

Financing

Copyright © 2012 Pearson Education 1-9

10. 11. 12. Accounting Information Systems

Collect, process, store, and report data and information

If Accounting = language of business

AIS = information providing vehicle

Accounting = AIS

Copyright © 2012 Pearson Education 1-12

13. Components of an AIS

People using the system

Procedures and Instructions

For collecting, processing, and storing data

Data

Software

Information Technology (IT) Infrastructure

Computers, peripherals, networks, and so on

Internal Control and Security

Safeguard the system and its data

Copyright © 2012 Pearson Education 1-13

14. AIS and Business Functions

Collect and store data about organizational:

Activities, resources, and personnel

Transform data into information enabling

Management to:

Plan, execute, control, and evaluate

Activities, resources, and personnel

Provide adequate control to safeguard

Assets and data

Copyright © 2012 Pearson Education 1-14

15. AIS Value Add

Improve Quality and Reduce Costs

Improve Efficiency

Improve Sharing Knowledge

Improve Supply Chain

Improve Internal Control

Improve Decision Making

Copyright © 2012 Pearson Education 1-15

16. Improve Decision Making

Identify situations that require action.

Provide alternative choices.

Reduce uncertainty.

Provide feedback on previous decisions.

Provide accurate and timely information.

Copyright © 2012 Pearson Education 1-16

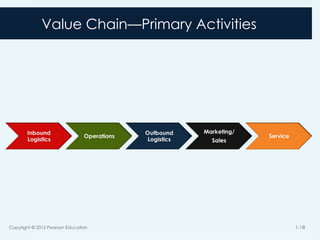

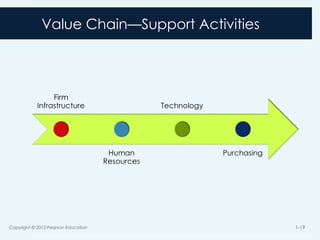

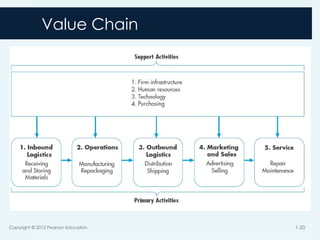

17. Value Chain

The set of activities a product or service moves along

before as output it is sold to a customer

At each activity the product or service gains value

Copyright © 2012 Pearson Education 1-17

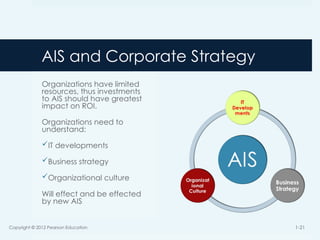

18. 19. 20. 21. AIS and Corporate Strategy

Organizations have limited

resources, thus investments

to AIS should have greatest

impact on ROI.

Organizations need to

understand:

IT developments

Business strategy

Organizational culture

Will effect and be effected

by new AIS

Copyright © 2012 Pearson Education 1-21

Editor's Notes #6 Point out to students that these characteristics are from the SFAC #2 Quality of Accounting Information (maybe have them read it). http://www.fasb.org/pdf/aop_CON2.pdf #7 Point out to students that these characteristics are from the SFAC #2 Quality of Accounting Information (maybe have them read it).