Download as PDF, PPTX

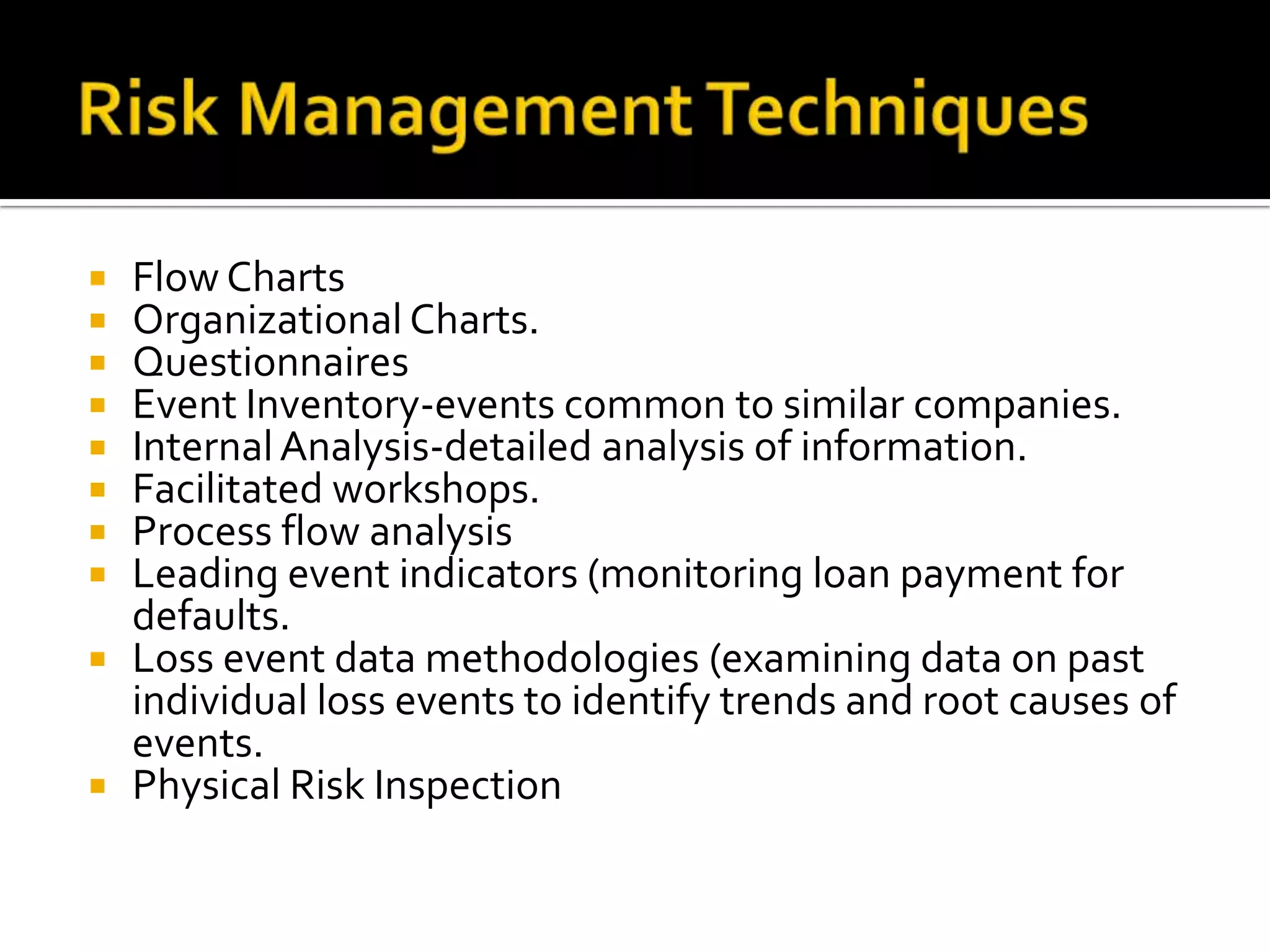

The document discusses various techniques for identifying risks, including flowcharts, organizational charts, questionnaires, checklists, physical risk inspections, and event inventories. Flowcharts and organizational charts can help locate areas of risk concentration and dependencies. Questionnaires are useful for collecting information from different staff but need to be designed carefully. Physical risk inspections allow assessing risks firsthand but are time-consuming. Event inventories examine past loss events to identify trends. The techniques have advantages and disadvantages, so a combination is often best to comprehensively identify risks.