Downloaded 51 times

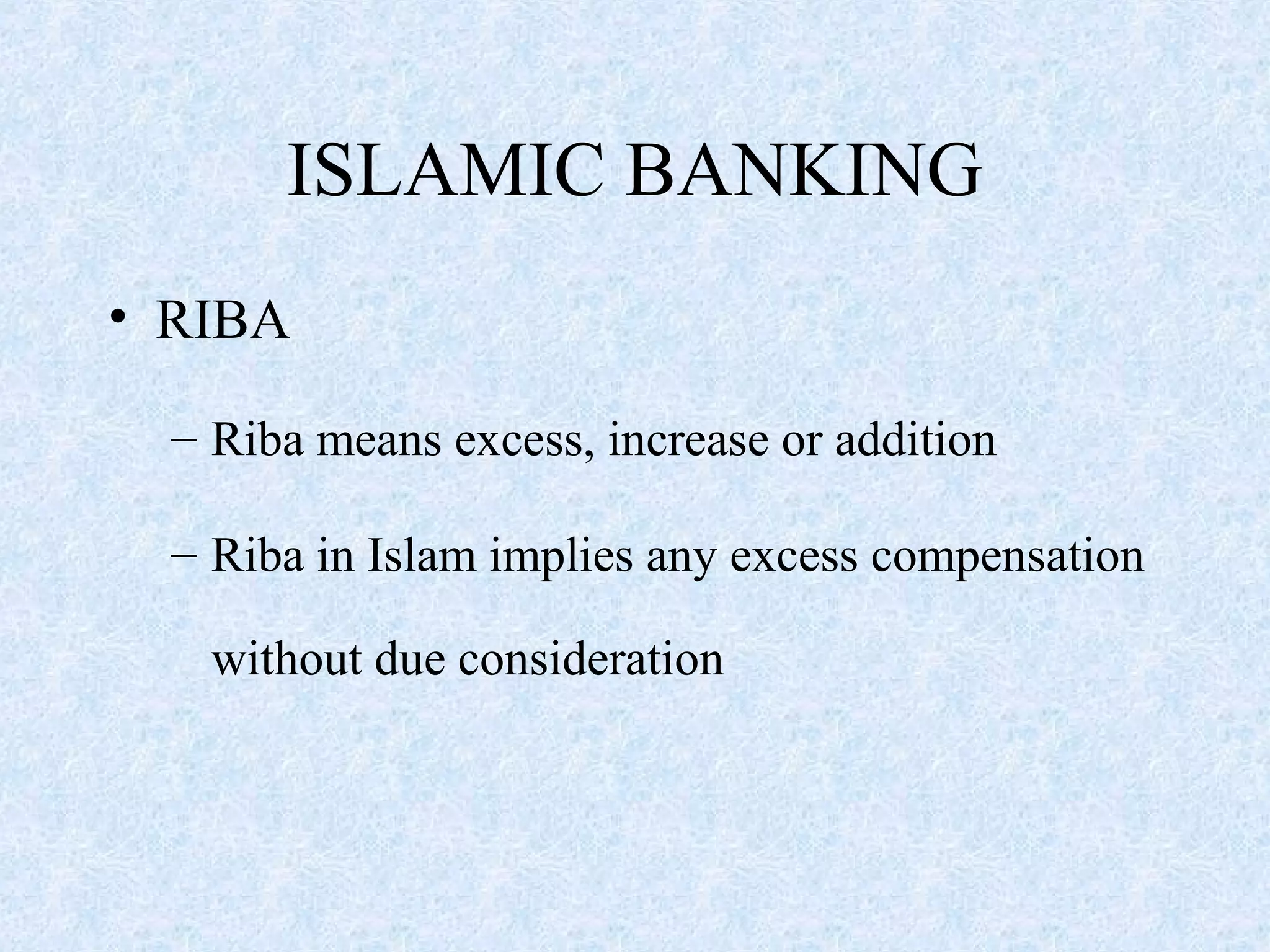

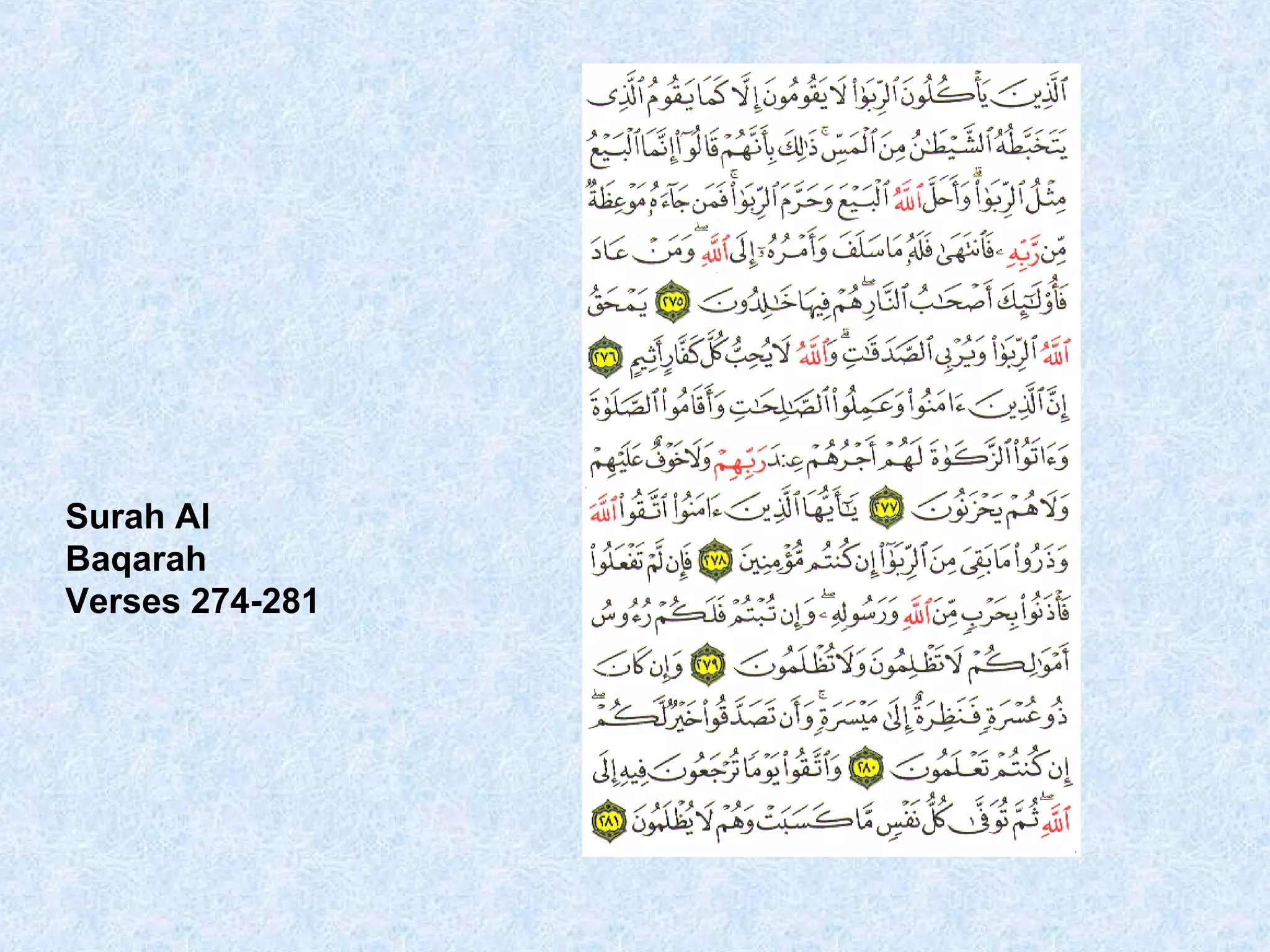

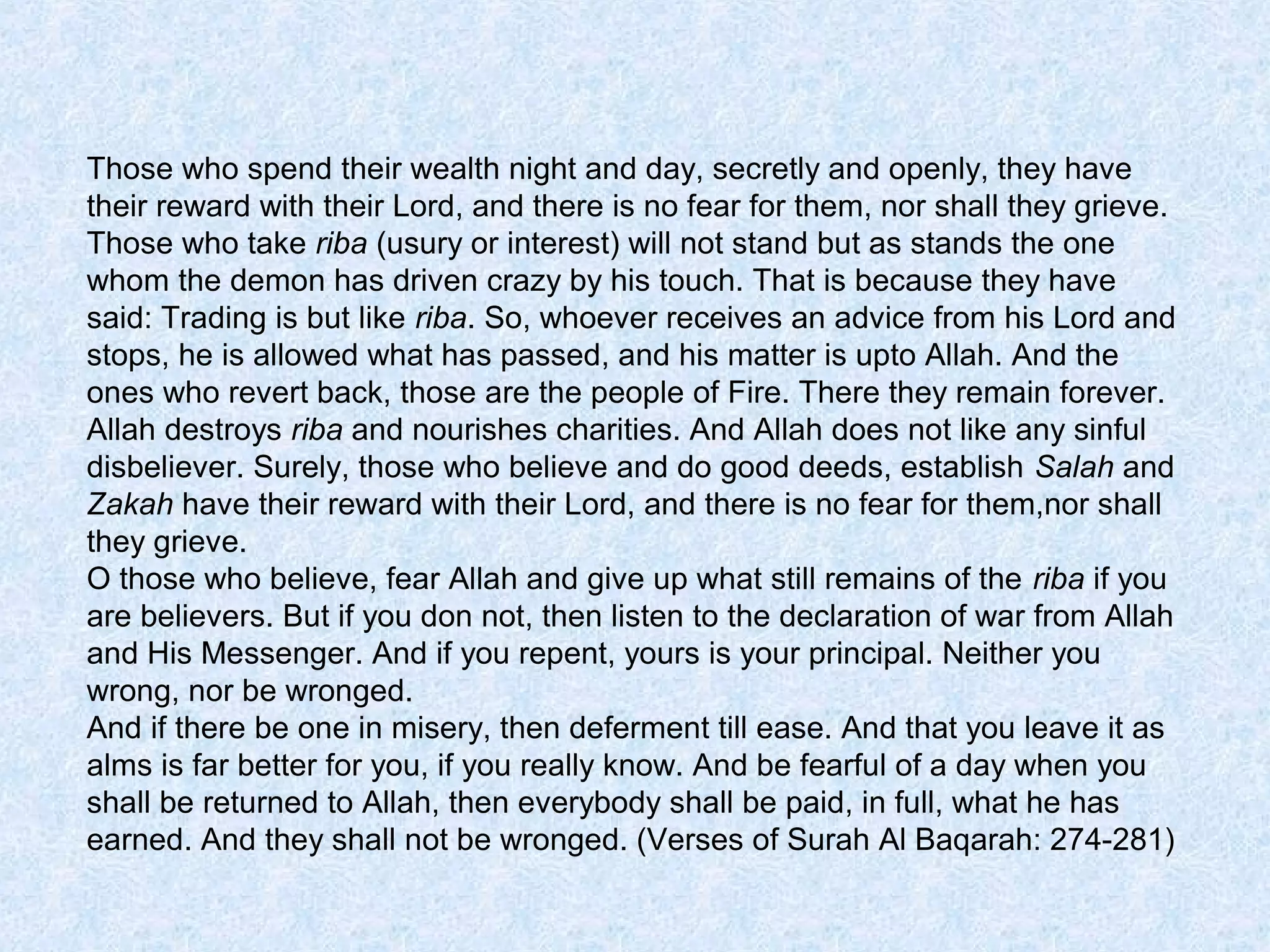

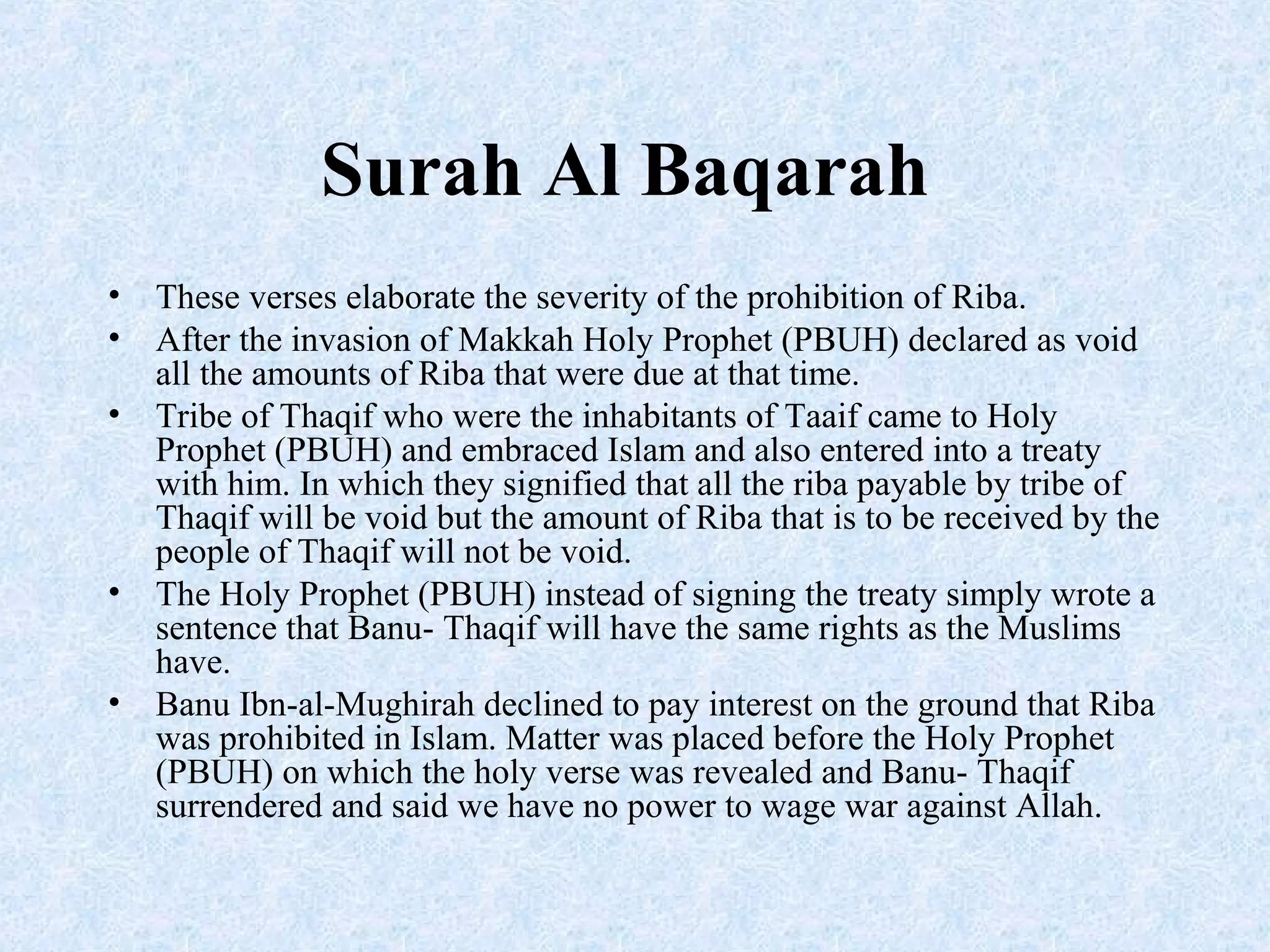

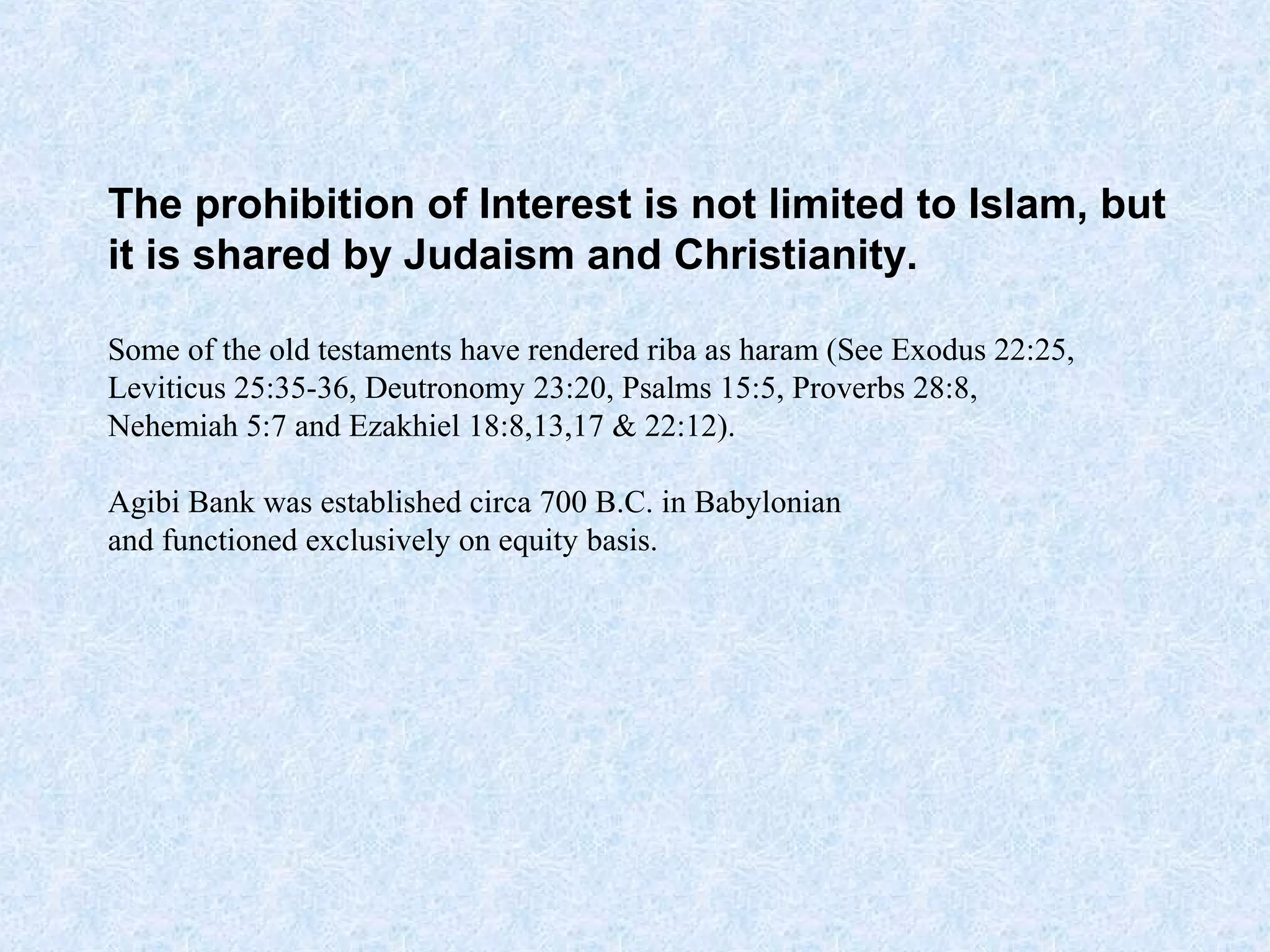

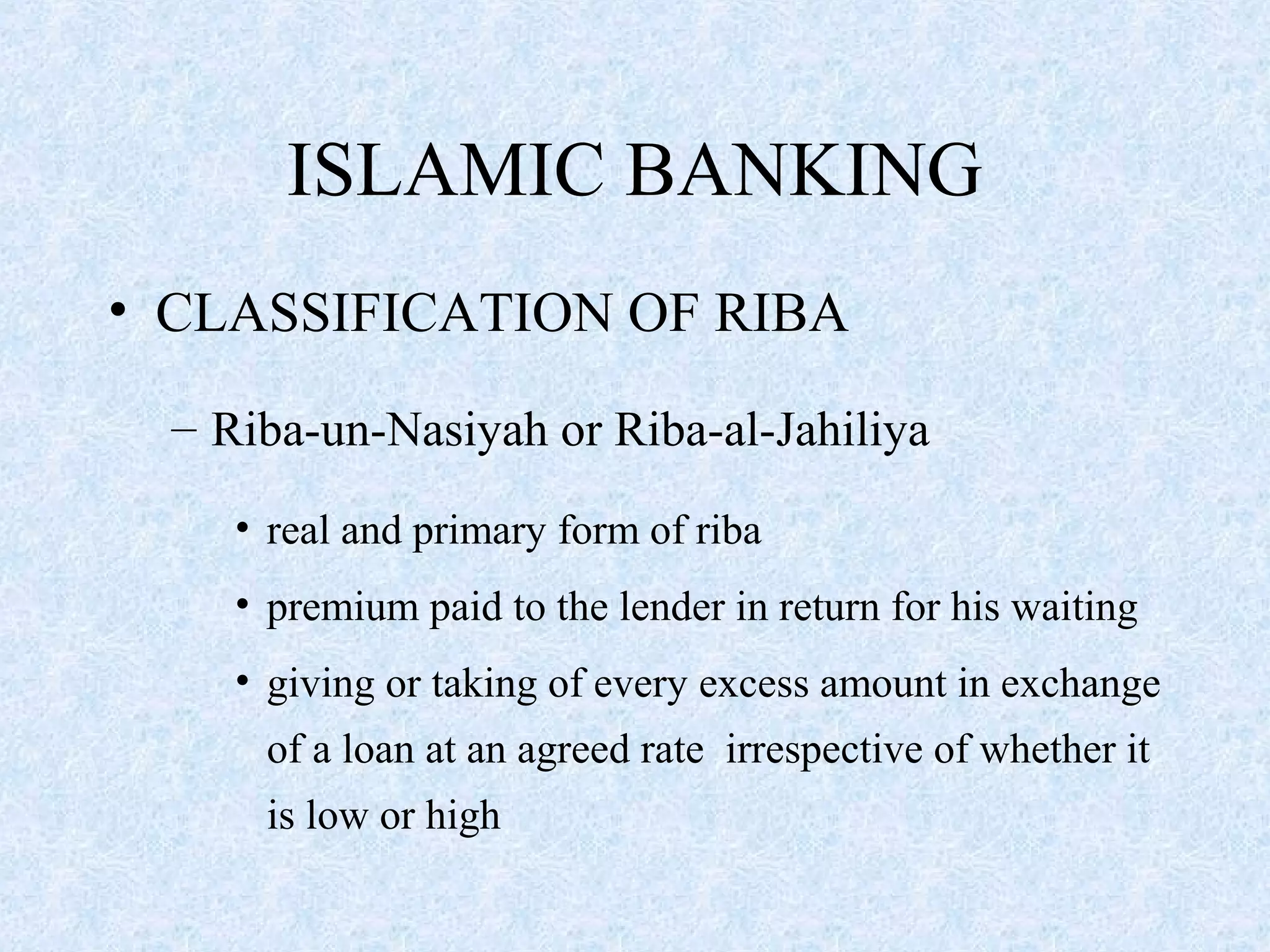

This document discusses the Islamic concepts of Riba, Gharar and Qimar. It defines Riba as any excess compensation without due consideration, especially interest charged on loans. The document outlines verses from the Quran that prohibit Riba and classify two types of Riba - Riba al-Nasiyah (interest charged on loans) and Riba al-Fadl (excess received when exchanging specific commodities). It also discusses the prohibition of Gharar (uncertainty) in contracts and defines Qimar as events where there is a possibility of total loss for one party.