Downloaded 21 times

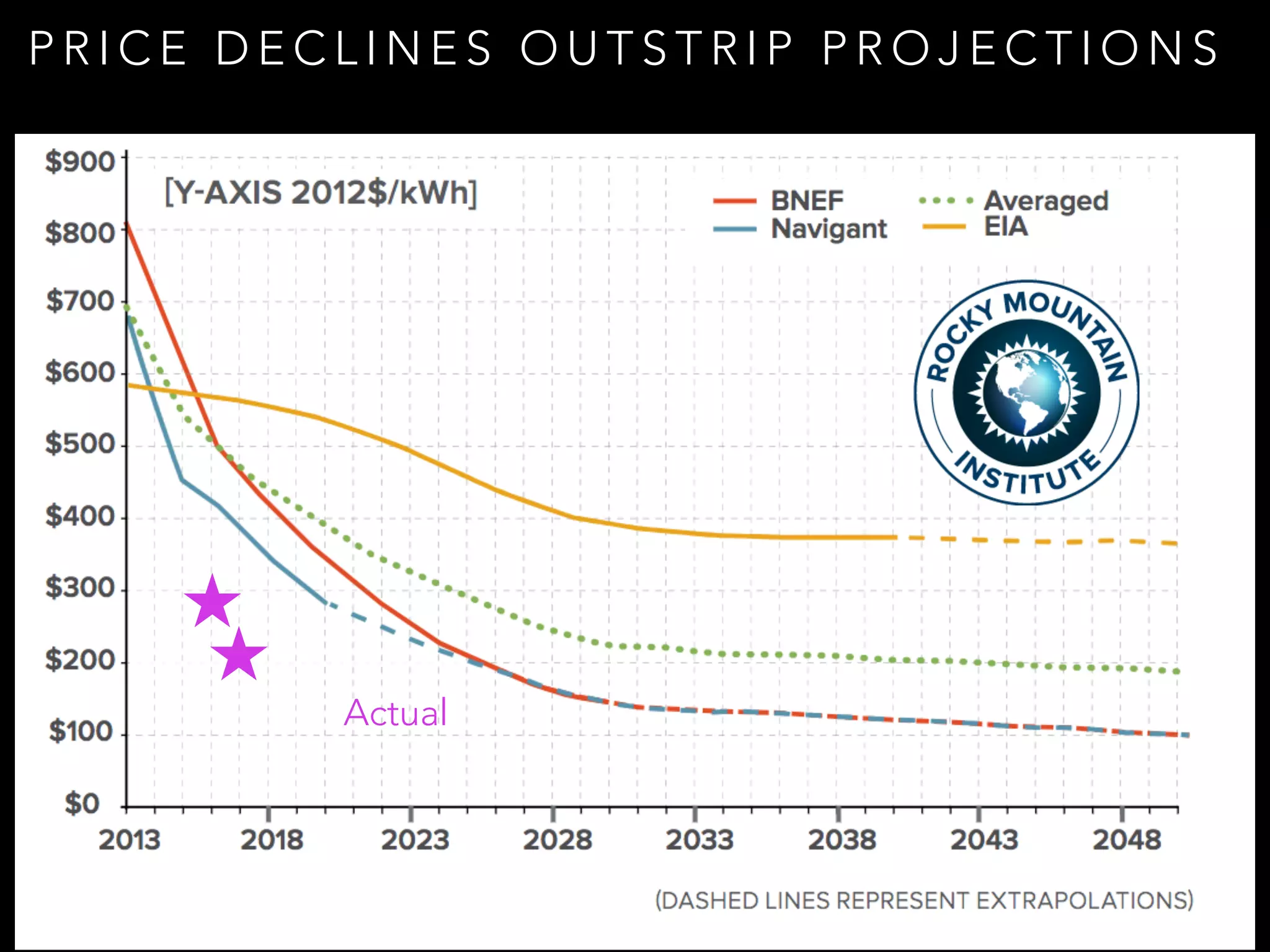

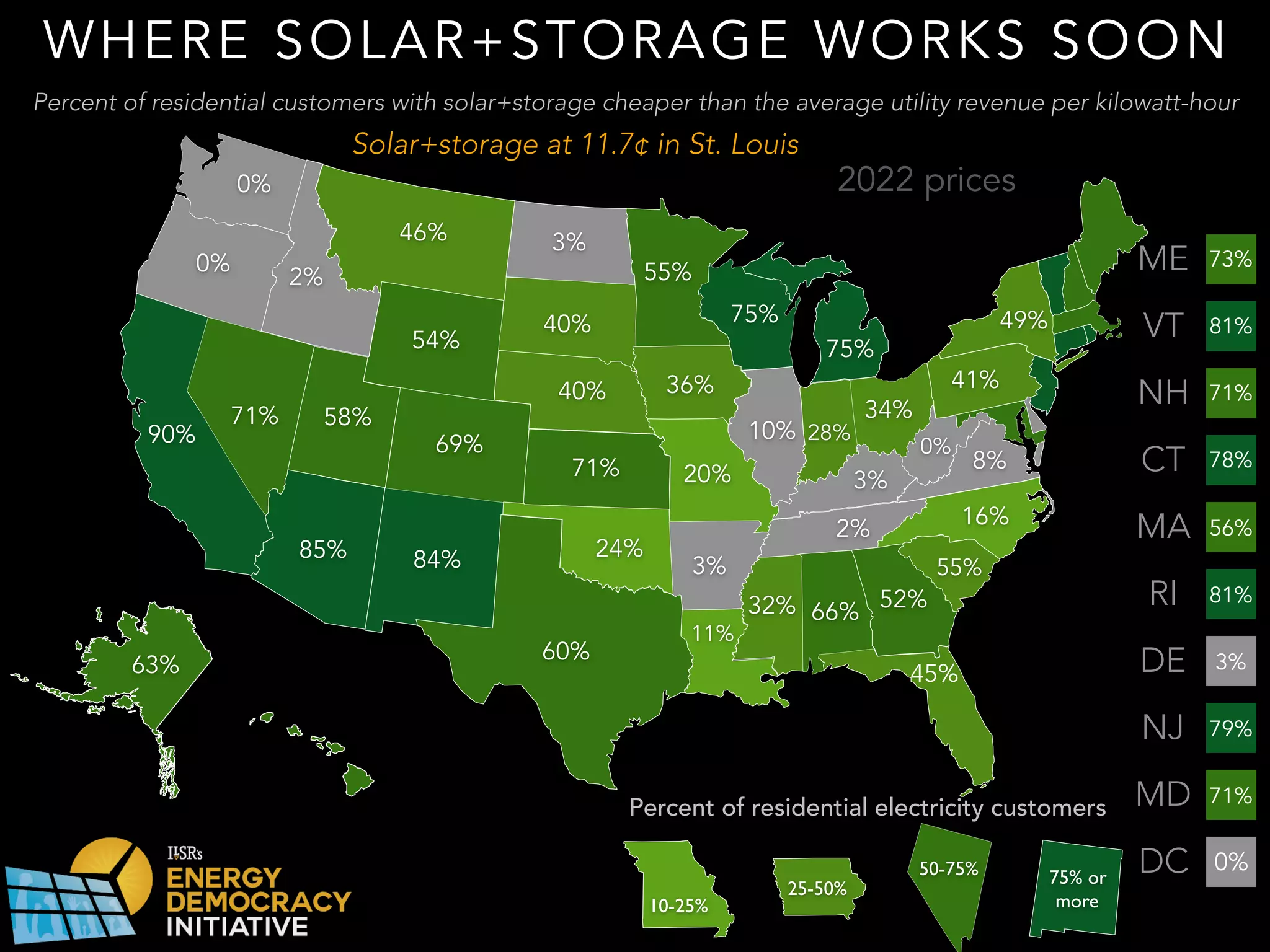

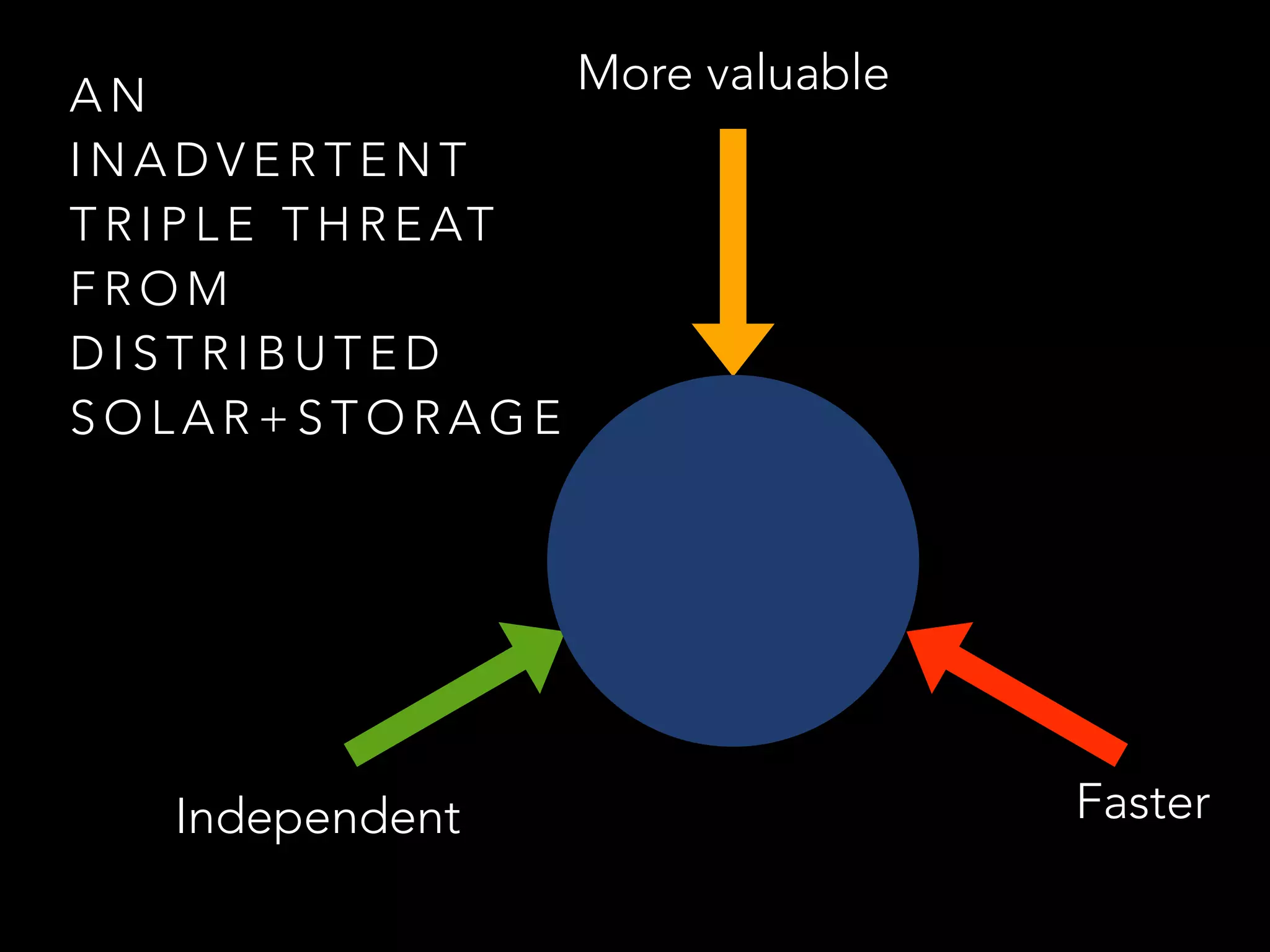

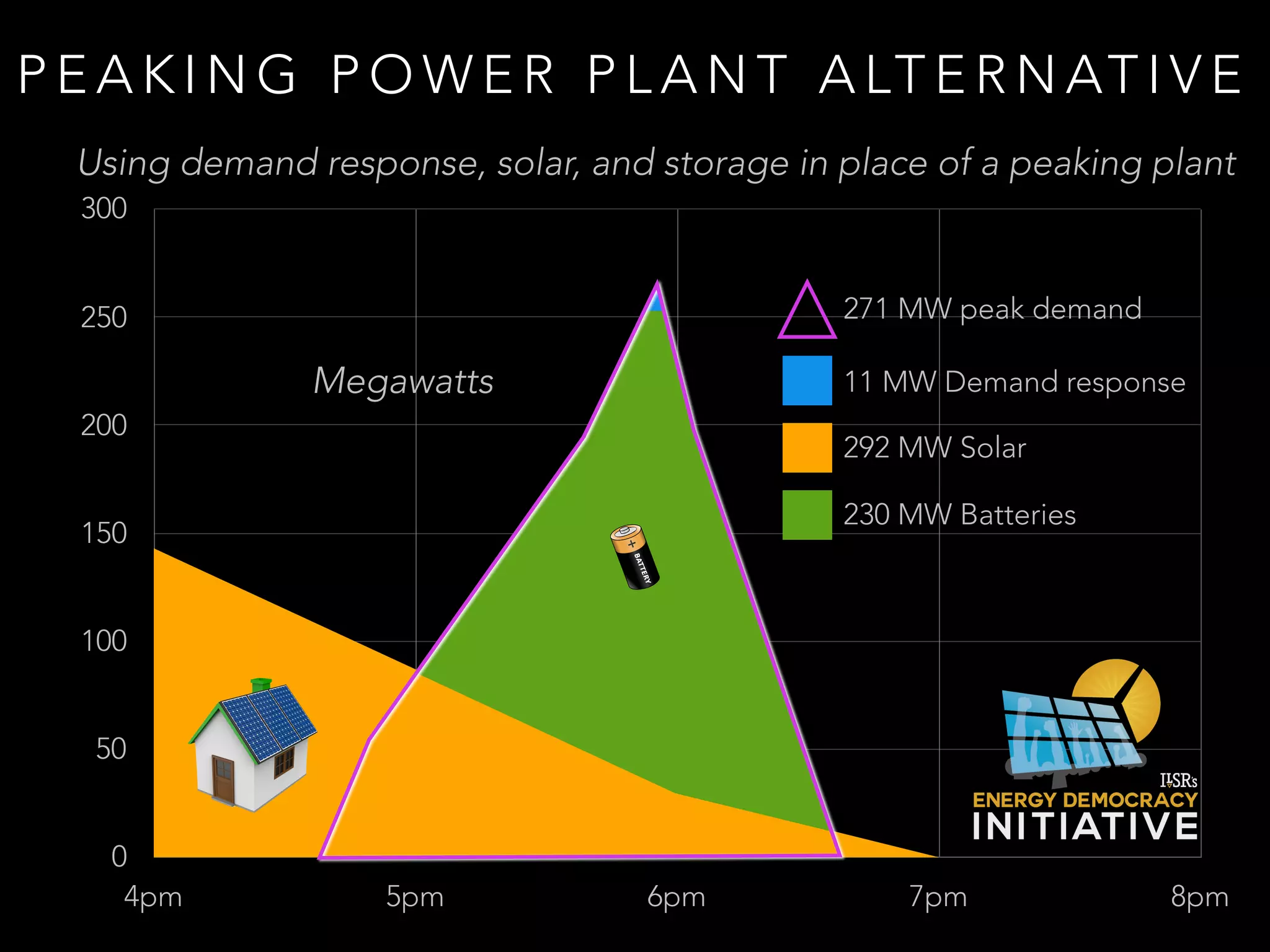

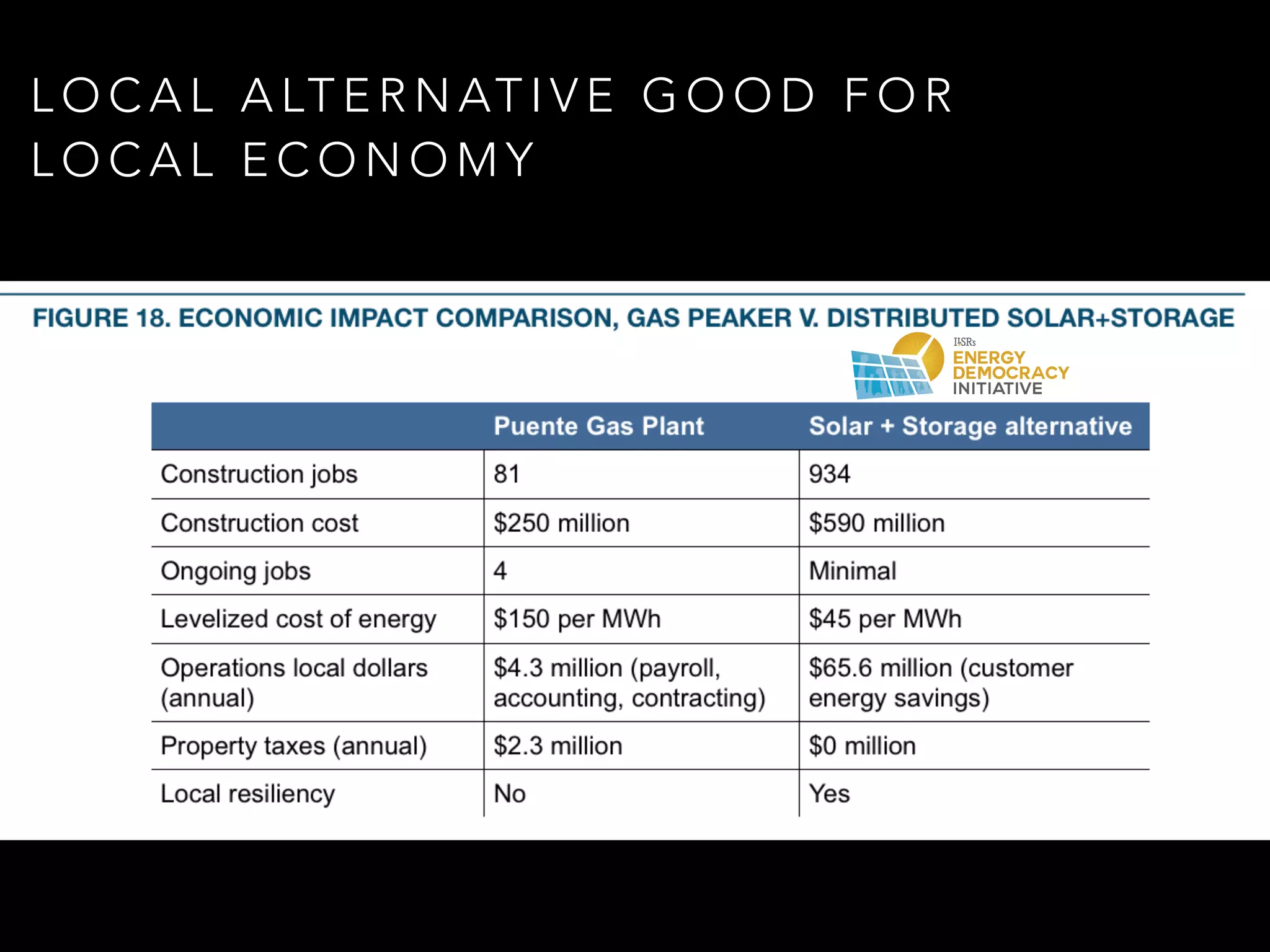

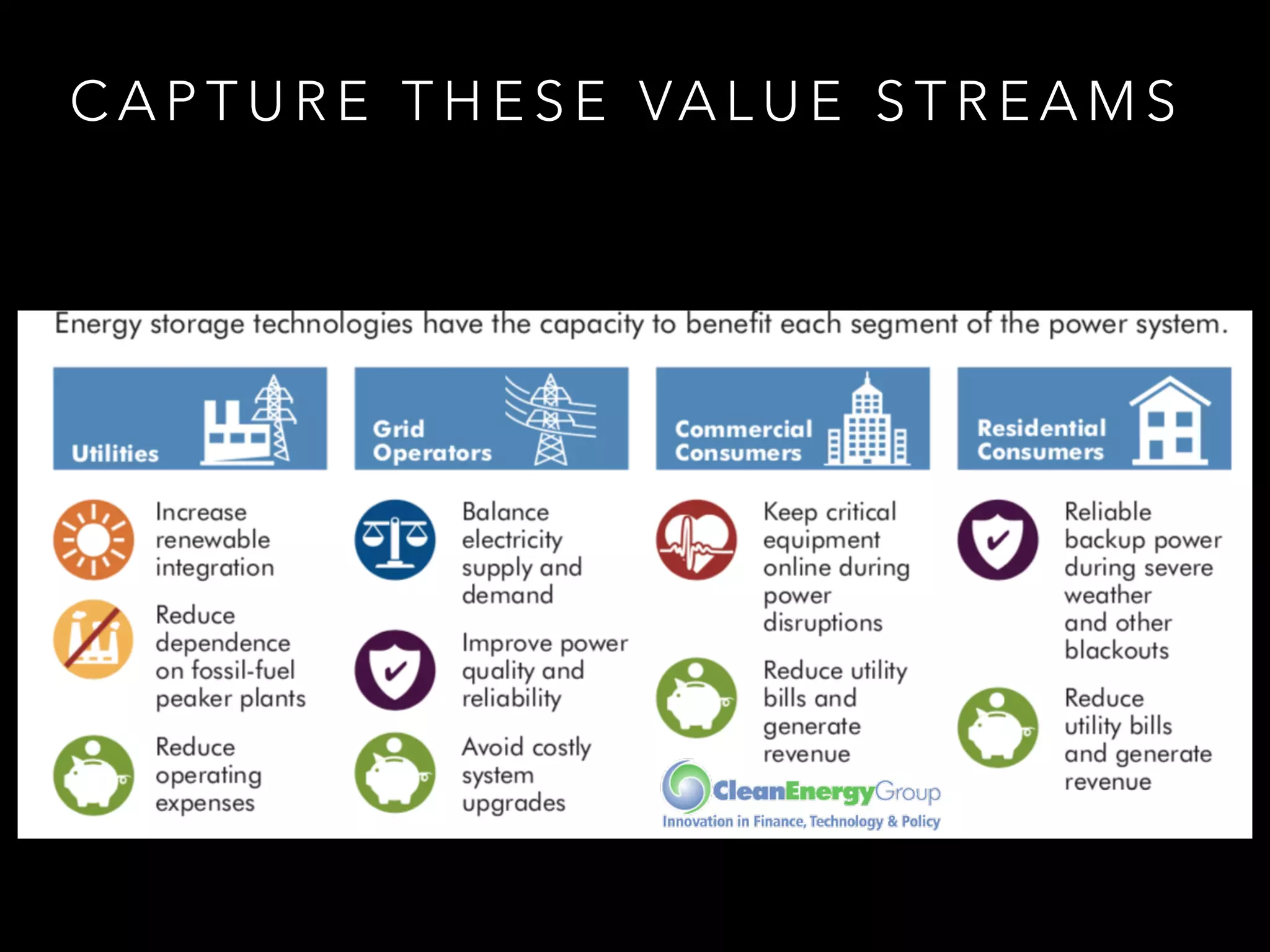

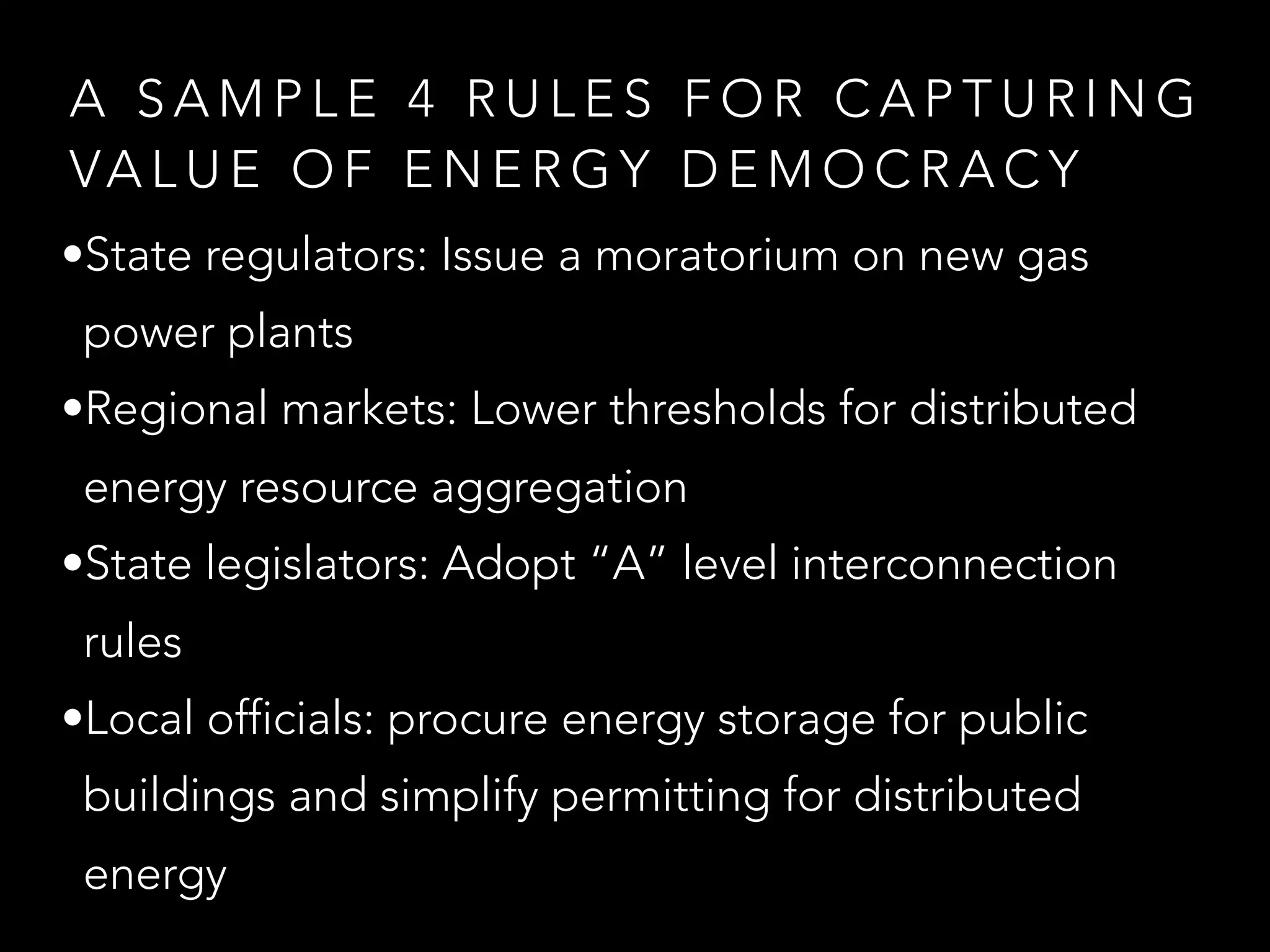

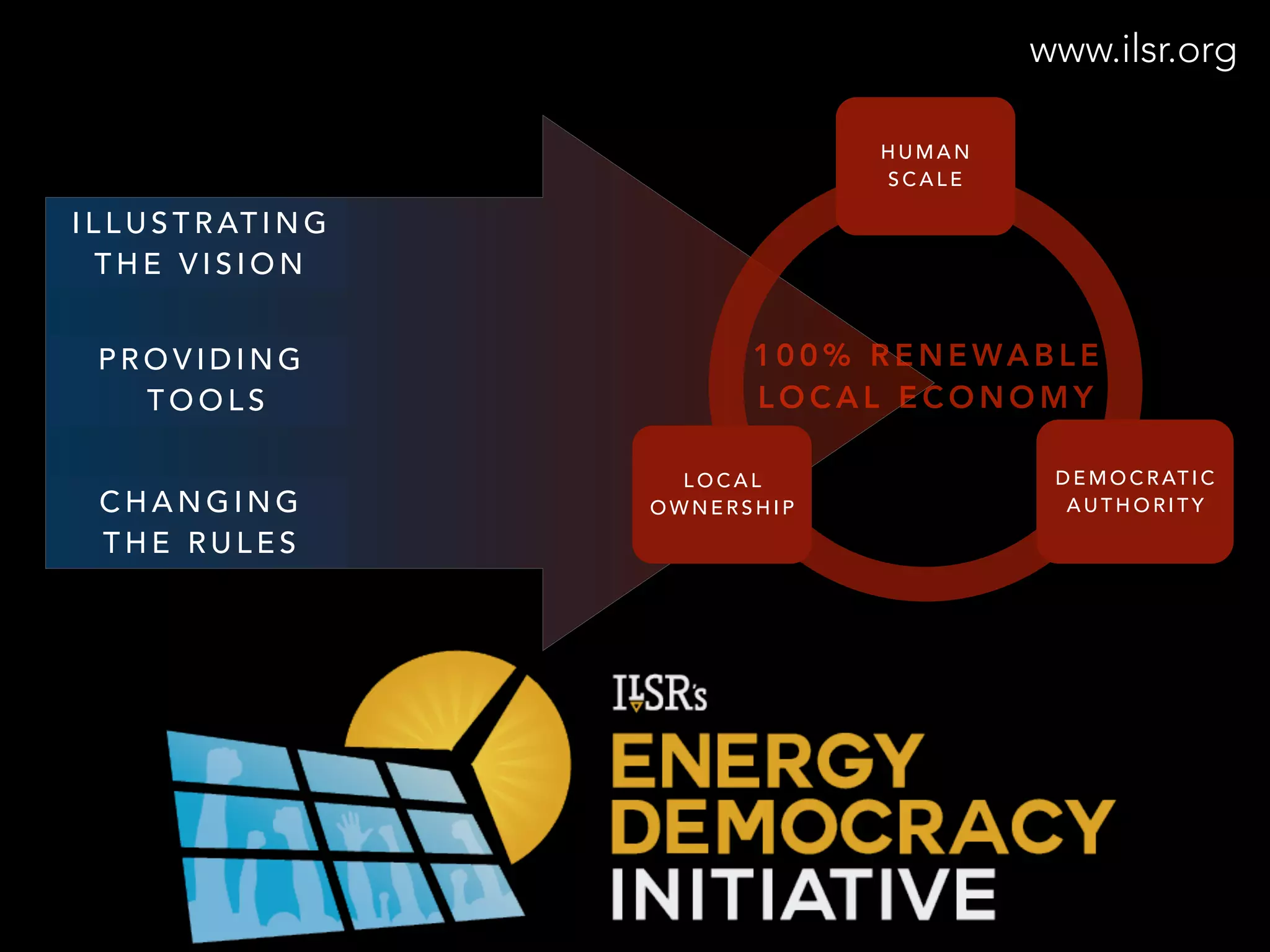

The document discusses the impact of solar and battery storage on electricity grid decision-making, highlighting a shift from utility dominance to consumer choice. It emphasizes the decreasing costs of energy storage and solar technology, showcasing the growing competitiveness of solar+storage solutions against traditional gas peaker plants. Additionally, it calls for regulatory changes to support the growth of distributed generation and promote a renewable energy economy.