Retirement checklist v.2

•Download as PPTX, PDF•

1 like•571 views

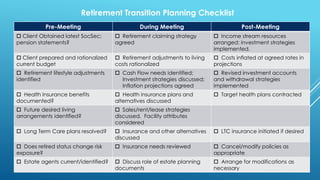

The retirement transition planning checklist outlines steps for clients to take before, during, and after meetings with financial advisors to plan for retirement, including obtaining statements, discussing claiming strategies and budgets, identifying costs and lifestyle adjustments, planning health insurance and long-term care, reviewing estate documents, and implementing investment and withdrawal strategies.

Recommended

More Related Content

What's hot

What's hot (18)

Similar to Retirement checklist v.2

Similar to Retirement checklist v.2 (20)

Retirement checklist v.2

- 1. Retirement Transition Planning Checklist Pre-Meeting During Meeting Post-Meeting Client Obtained latest SocSec; pension statements? Retirement claiming strategy agreed Income stream resources arranged; investment strategies implemented. Client prepared and rationalized current budget Retirement adjustments to living costs rationalized Costs inflated at agreed rates in projections Retirement lifestyle adjustments identified Cash Flow needs identified; Investment strategies discussed; Inflation projections agreed Revised investment accounts and withdrawal strategies implemented Health Insurance benefits documented? Health insurance plans and alternatives discussed Target health plans contracted Future desired living arrangements identified? Sales/rent/lease strategies discussed. Facility attributes considered Long Term Care plans resolved? Insurance and other alternatives discussed LTC insurance initiated if desired Does retired status change risk exposure? Insurance needs reviewed Cancel/modify policies as appropriate Estate agents current/identified? Discuss role of estate planning documents Arrange for modifications as necessary