Download as PDF, PPTX

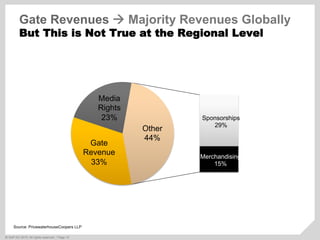

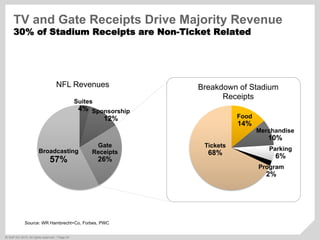

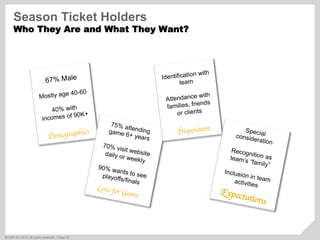

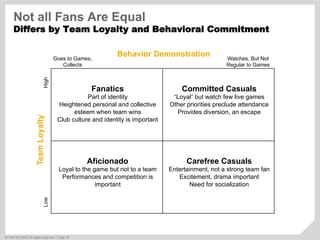

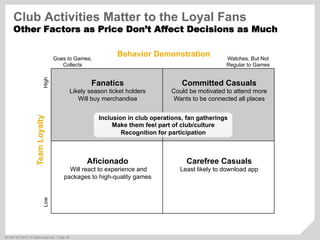

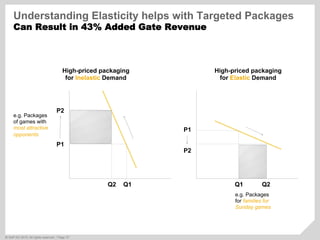

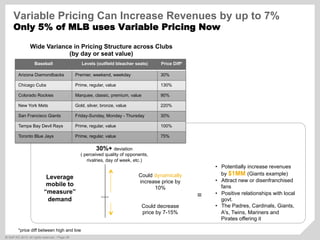

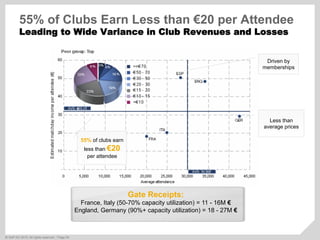

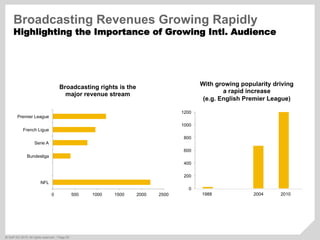

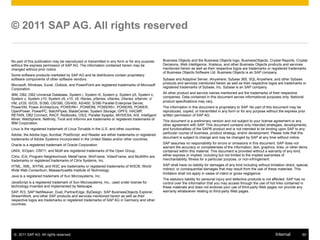

The document analyzes the current landscape of sports apps and fan engagement strategies, highlighting various features across leagues and clubs. It emphasizes the significance of differentiated loyalty programs and the diverse revenue sources in the sports industry, particularly noting that while gate receipts are essential, broadcasting and sponsorship revenues are crucial. Additionally, it discusses fan demographics and behaviors, cautioning that clubs must address no-shows and focus on creating unique value for season ticket holders to enhance profitability.