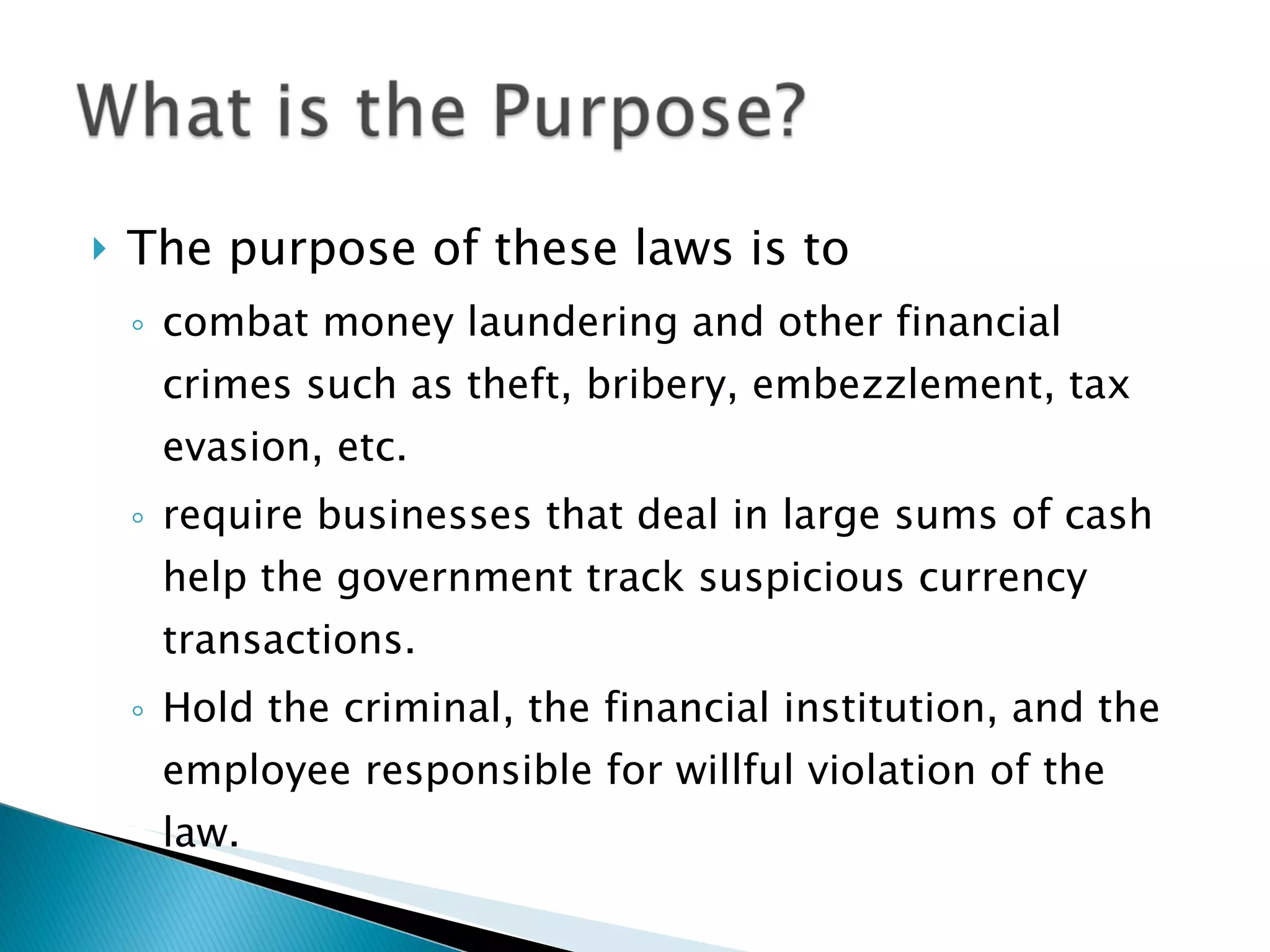

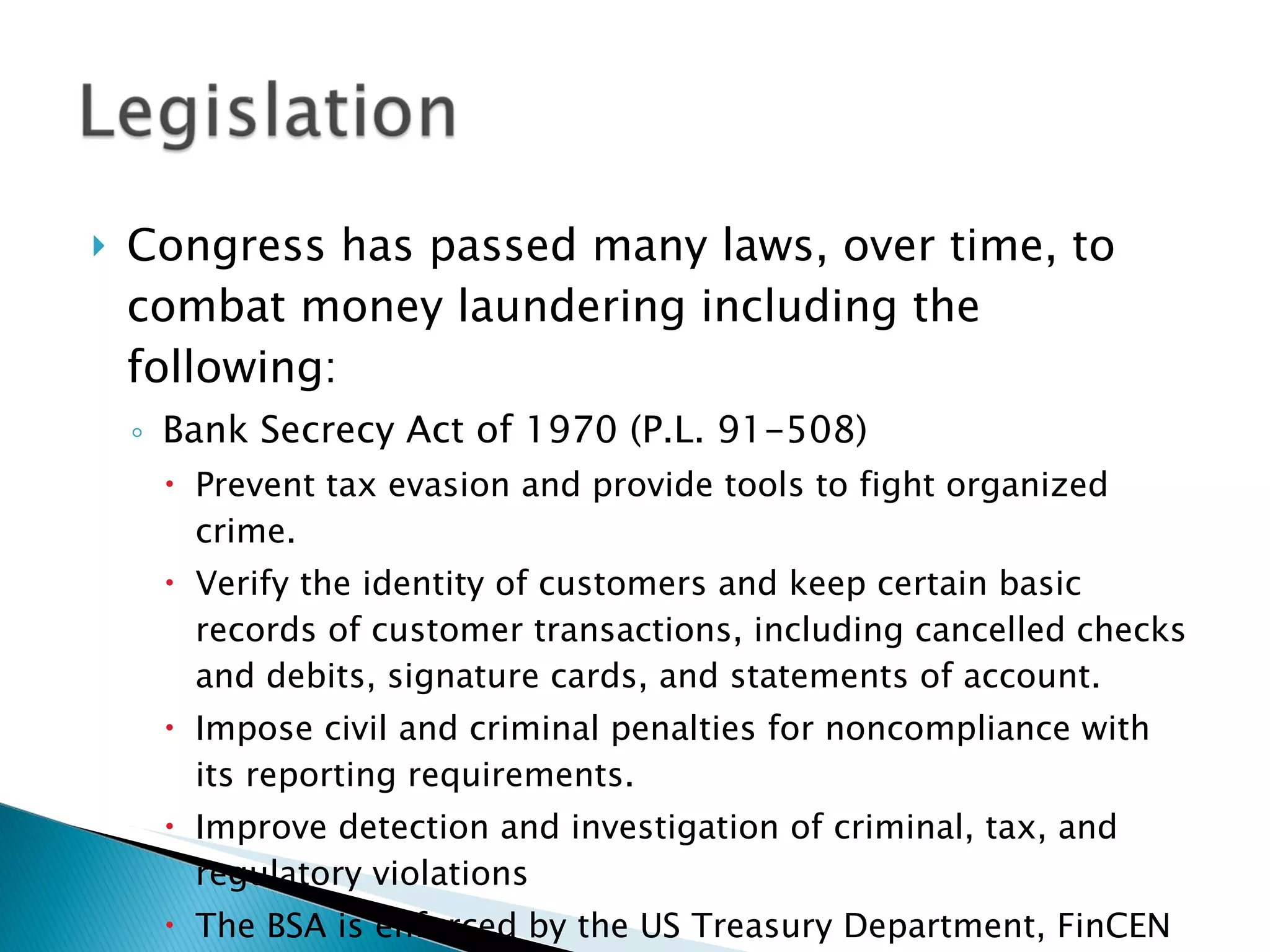

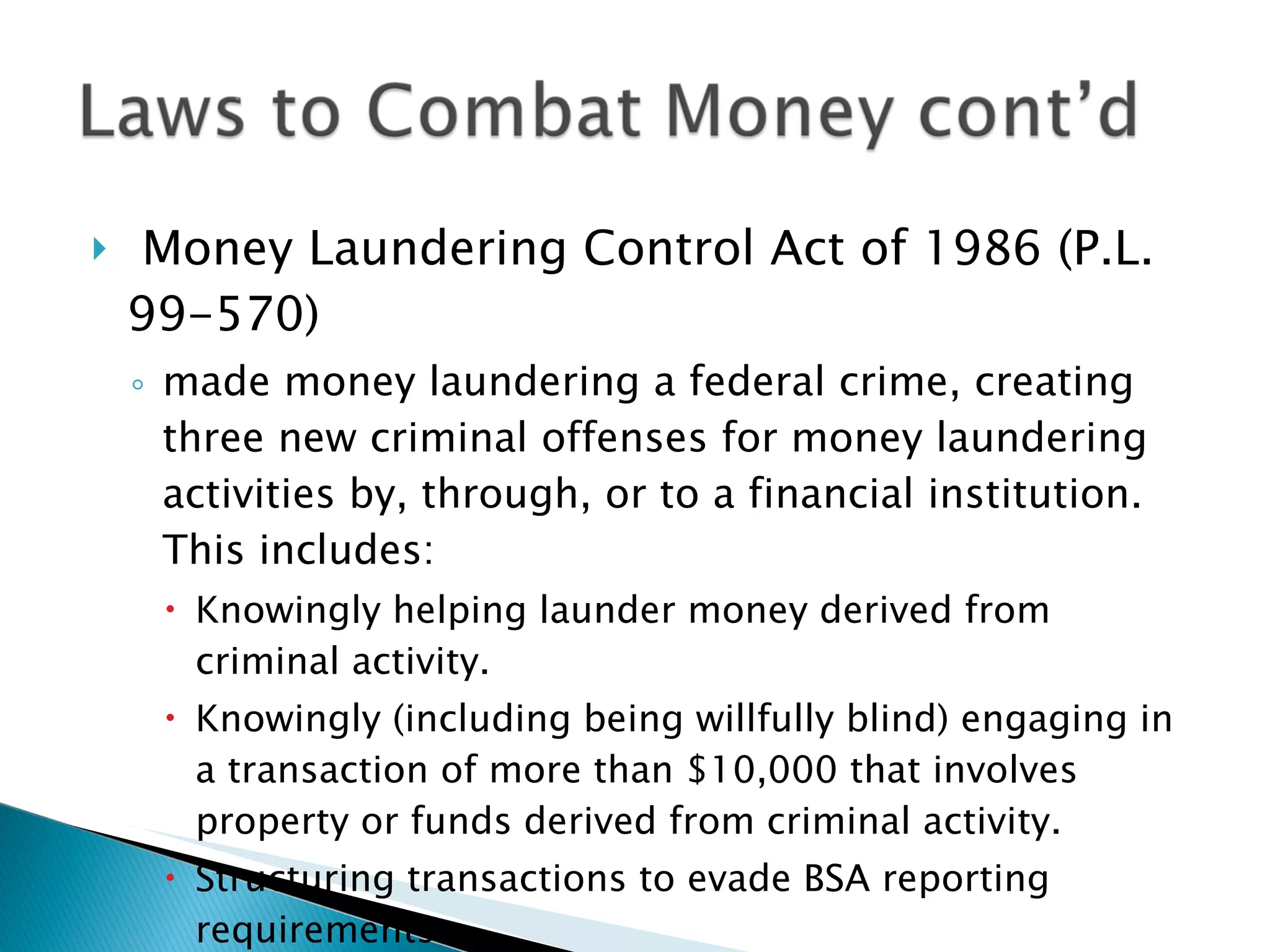

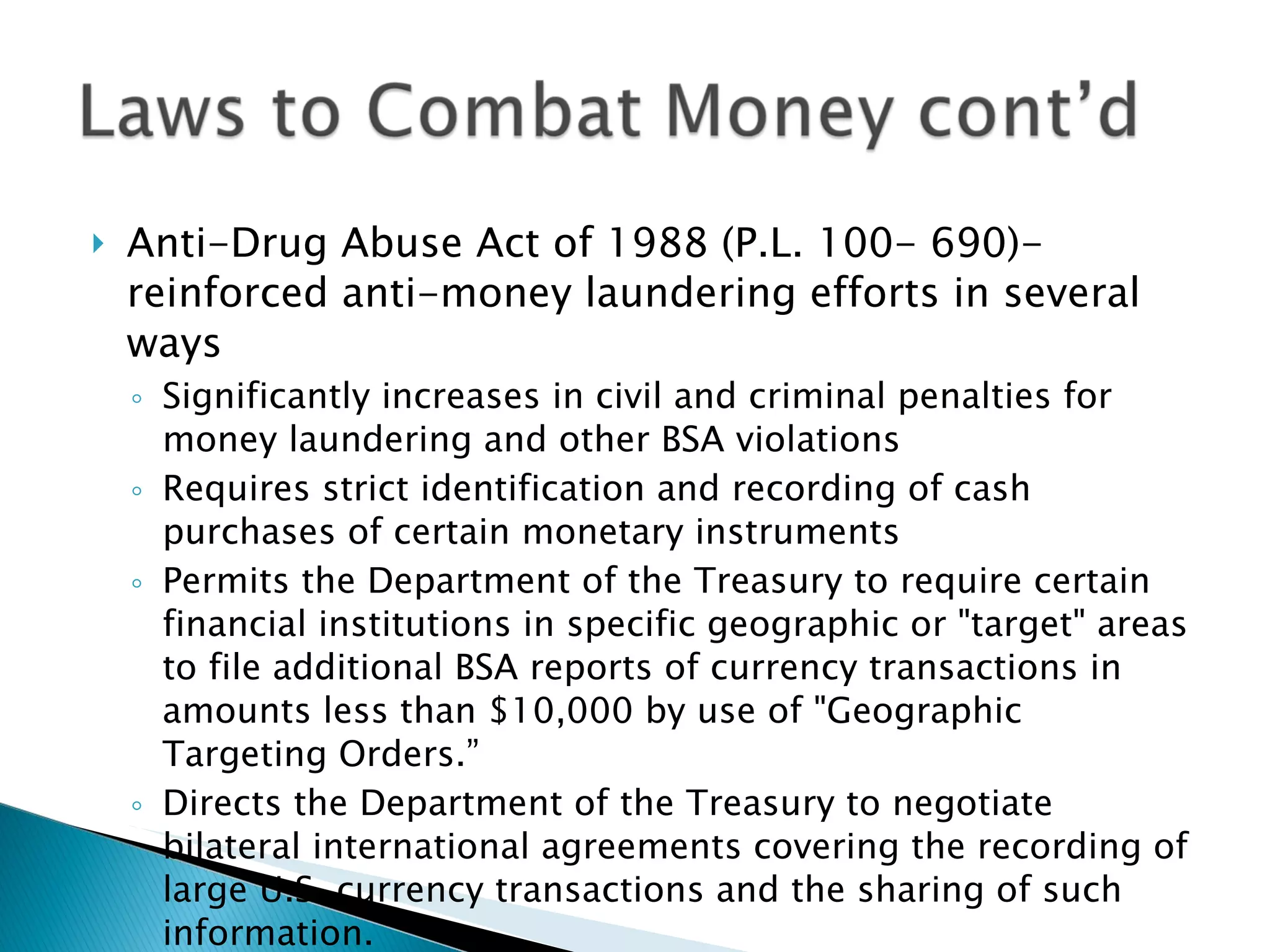

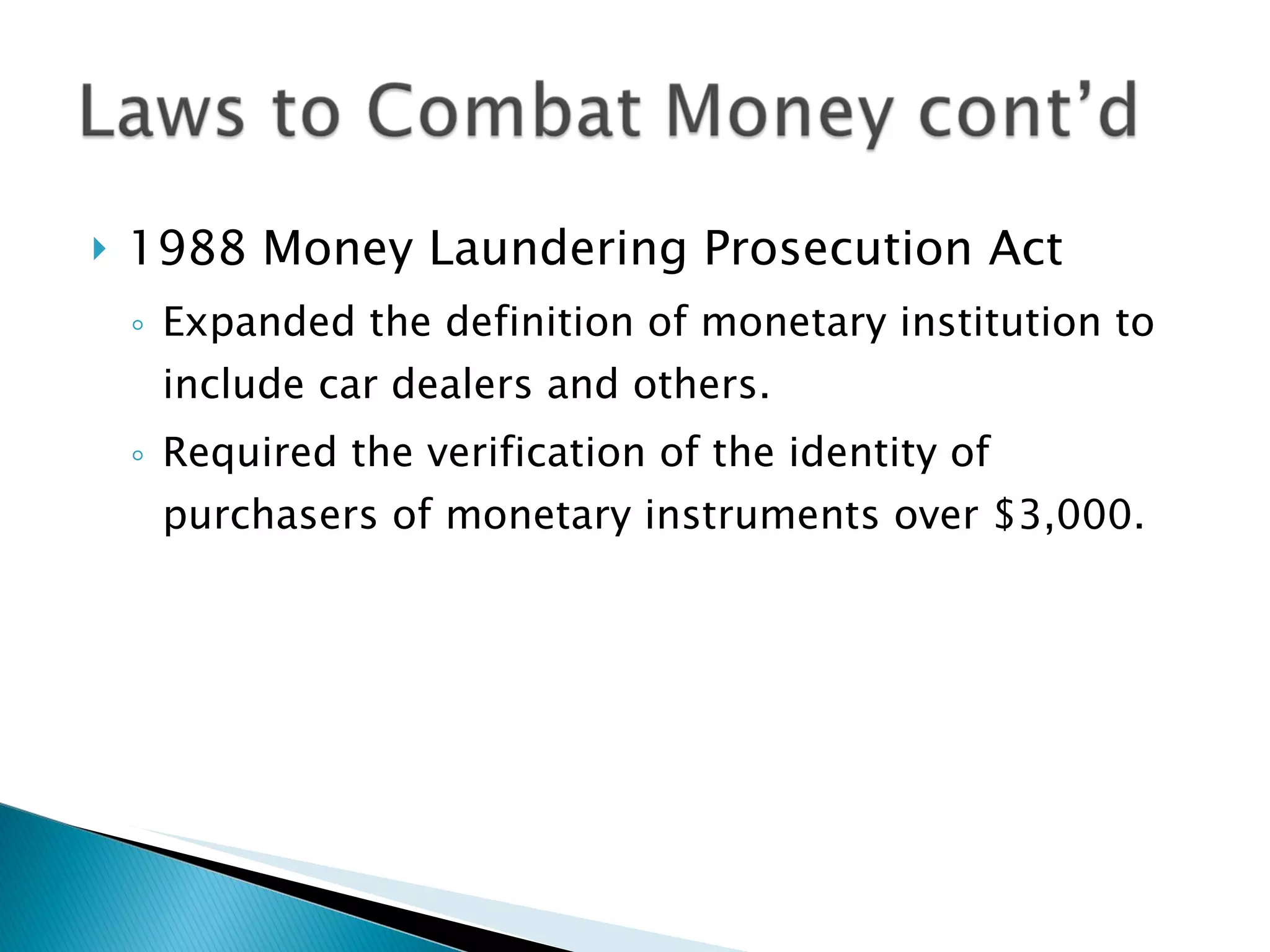

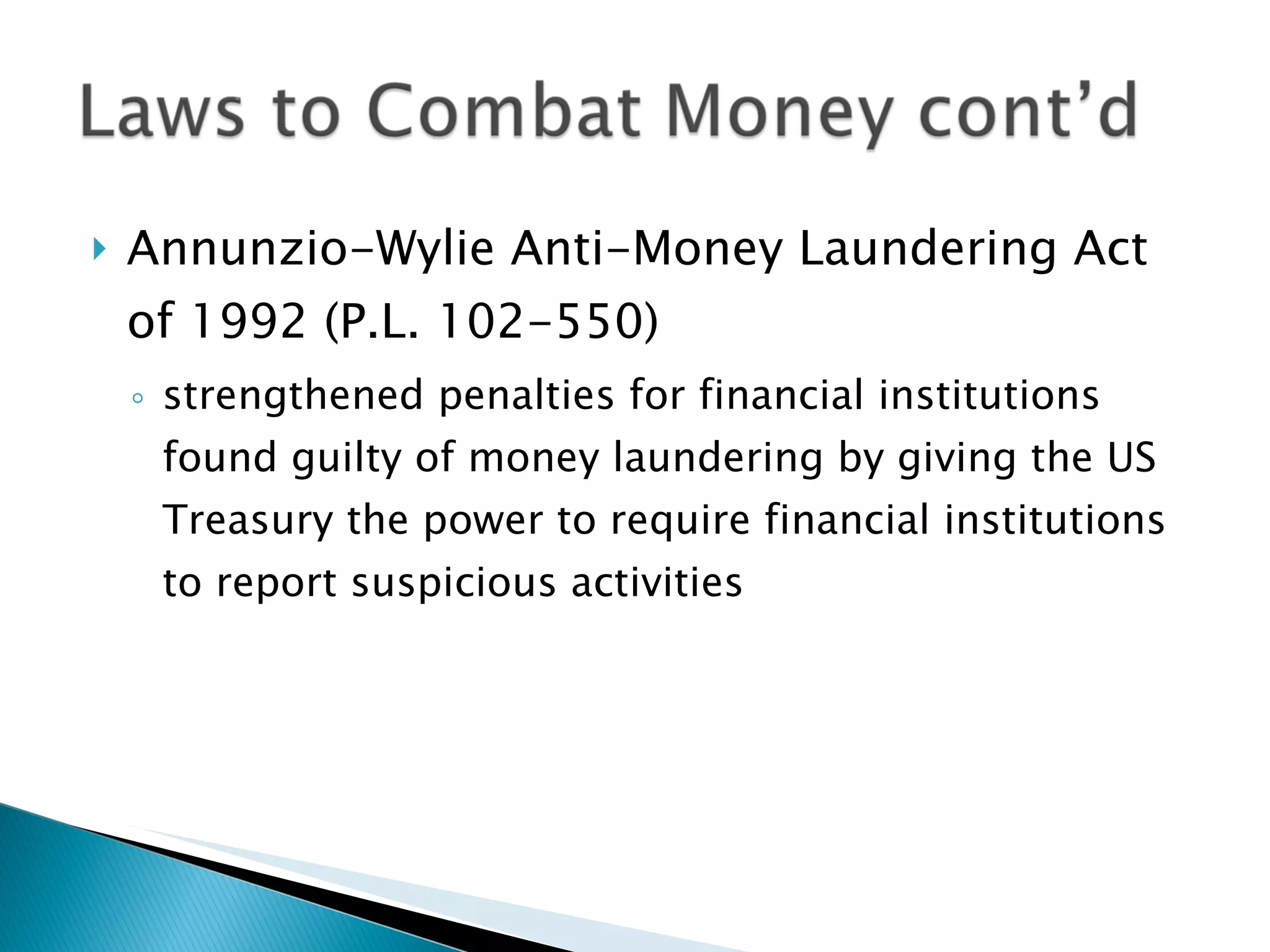

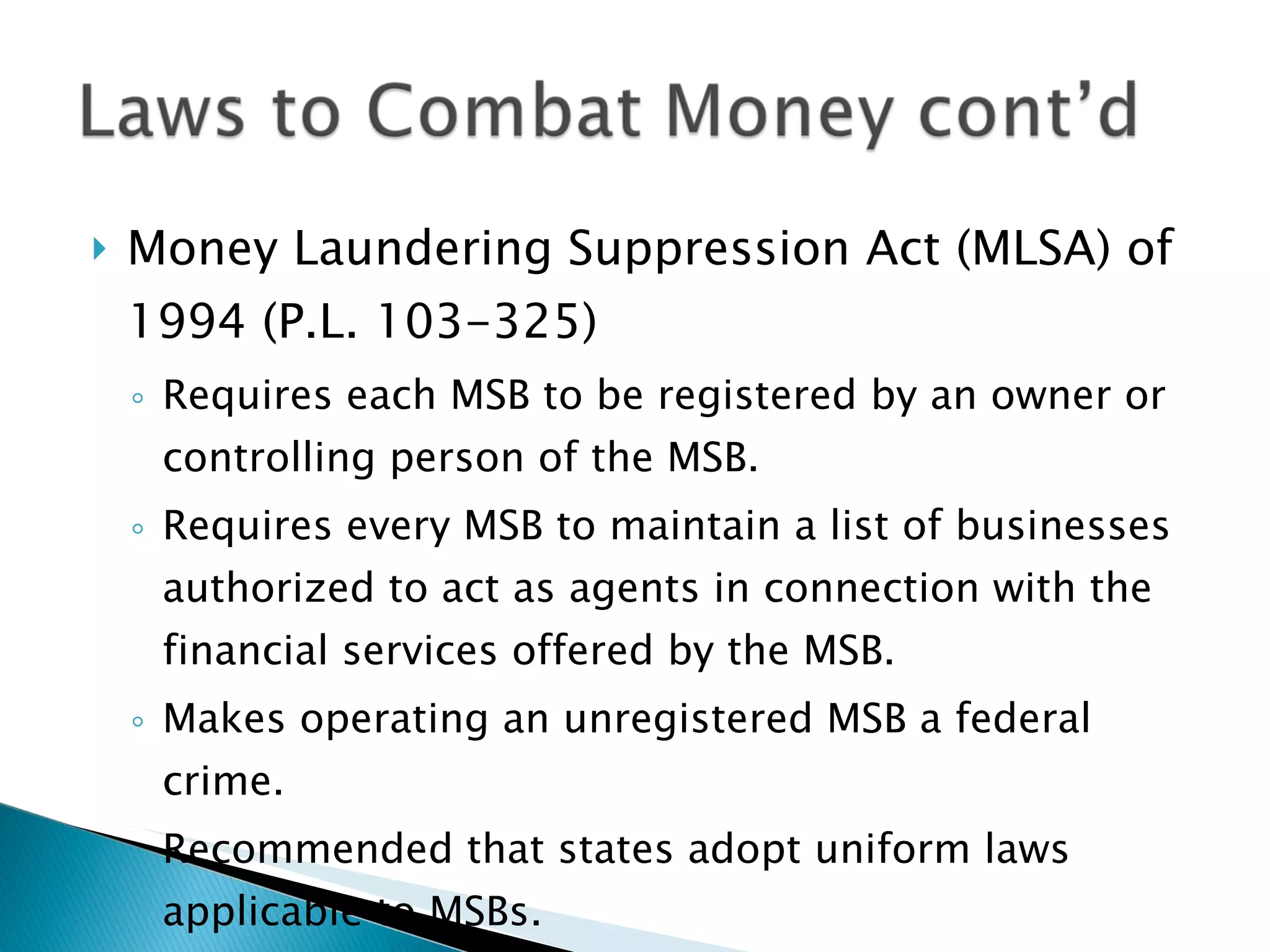

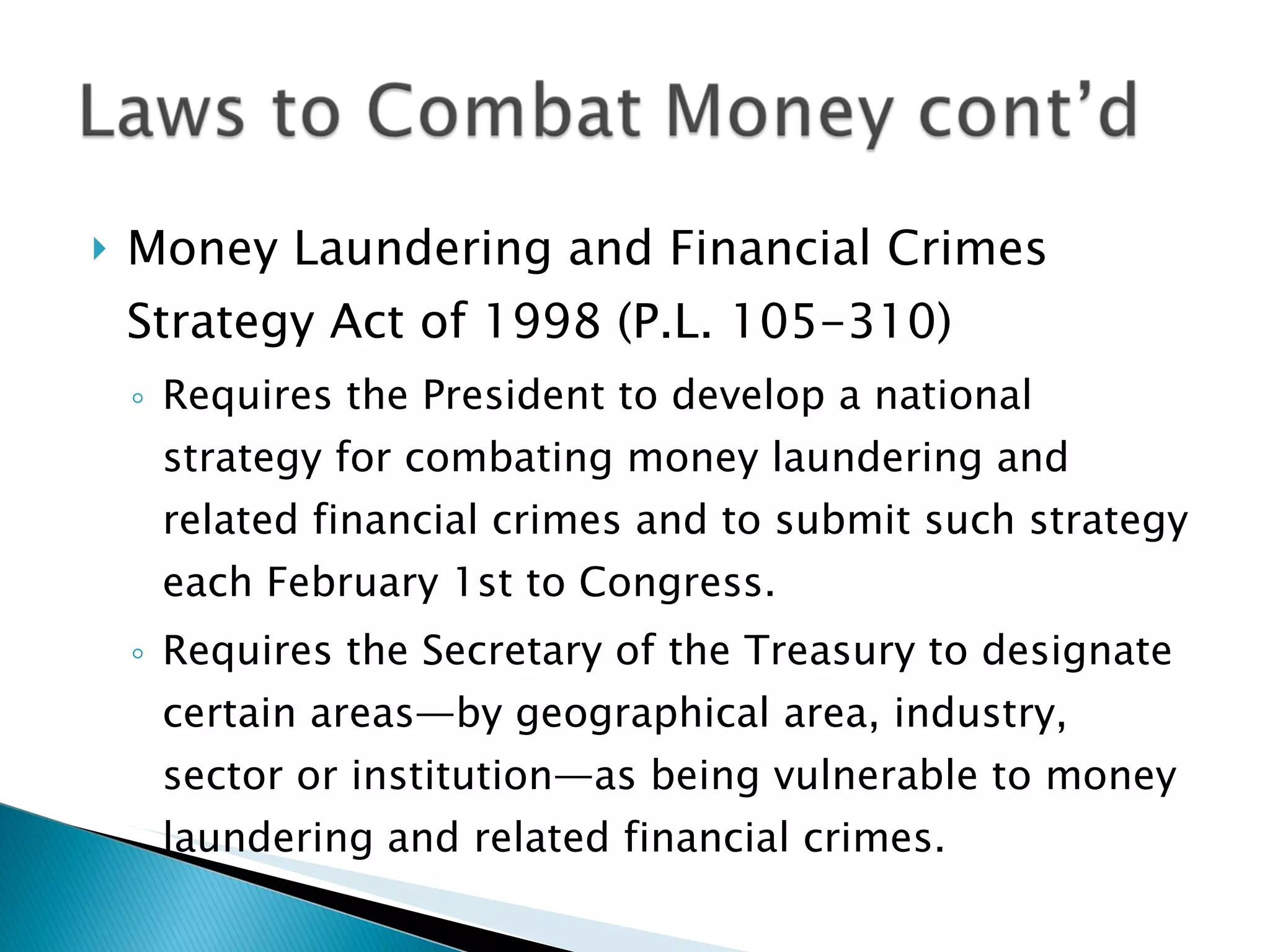

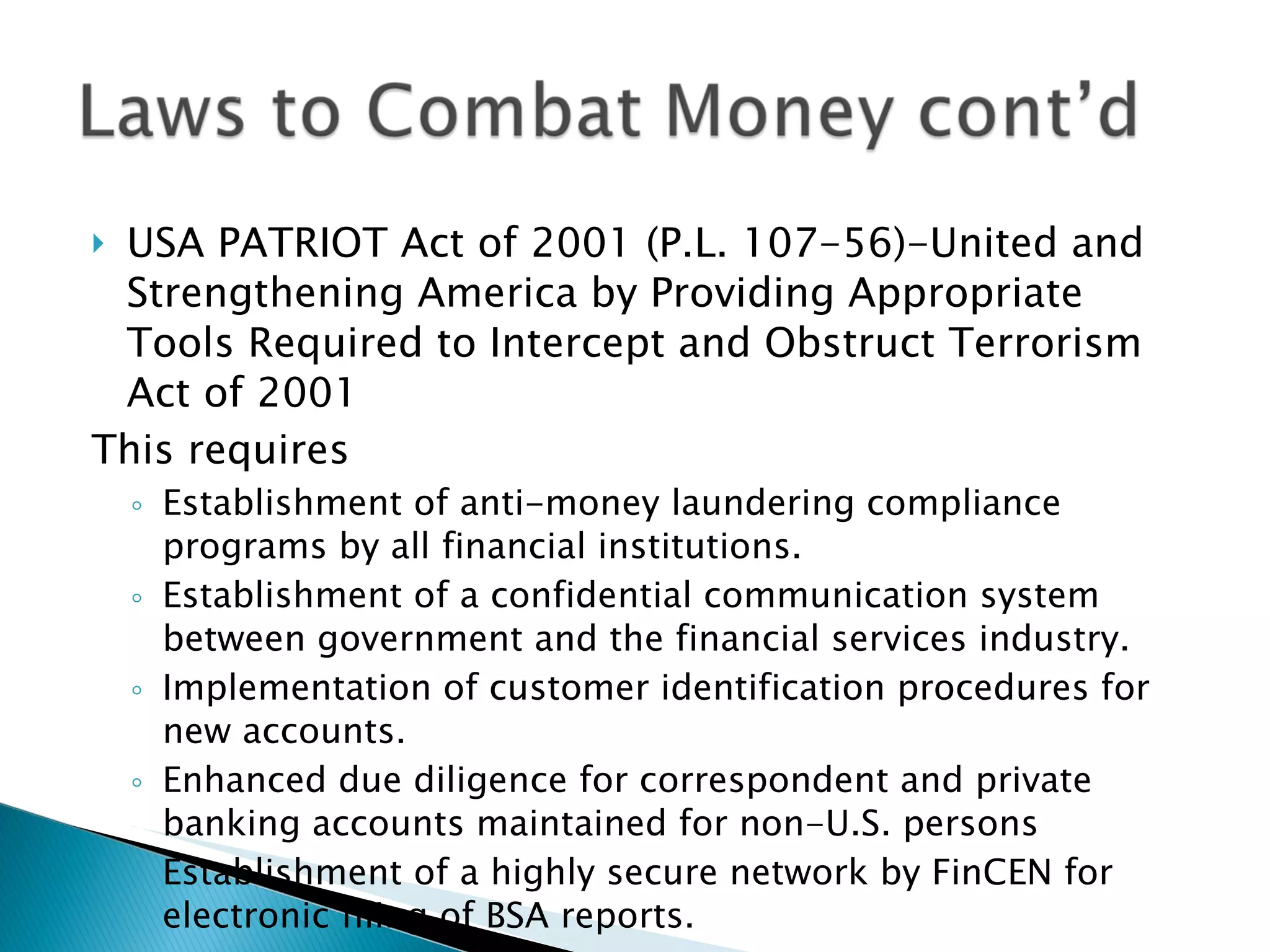

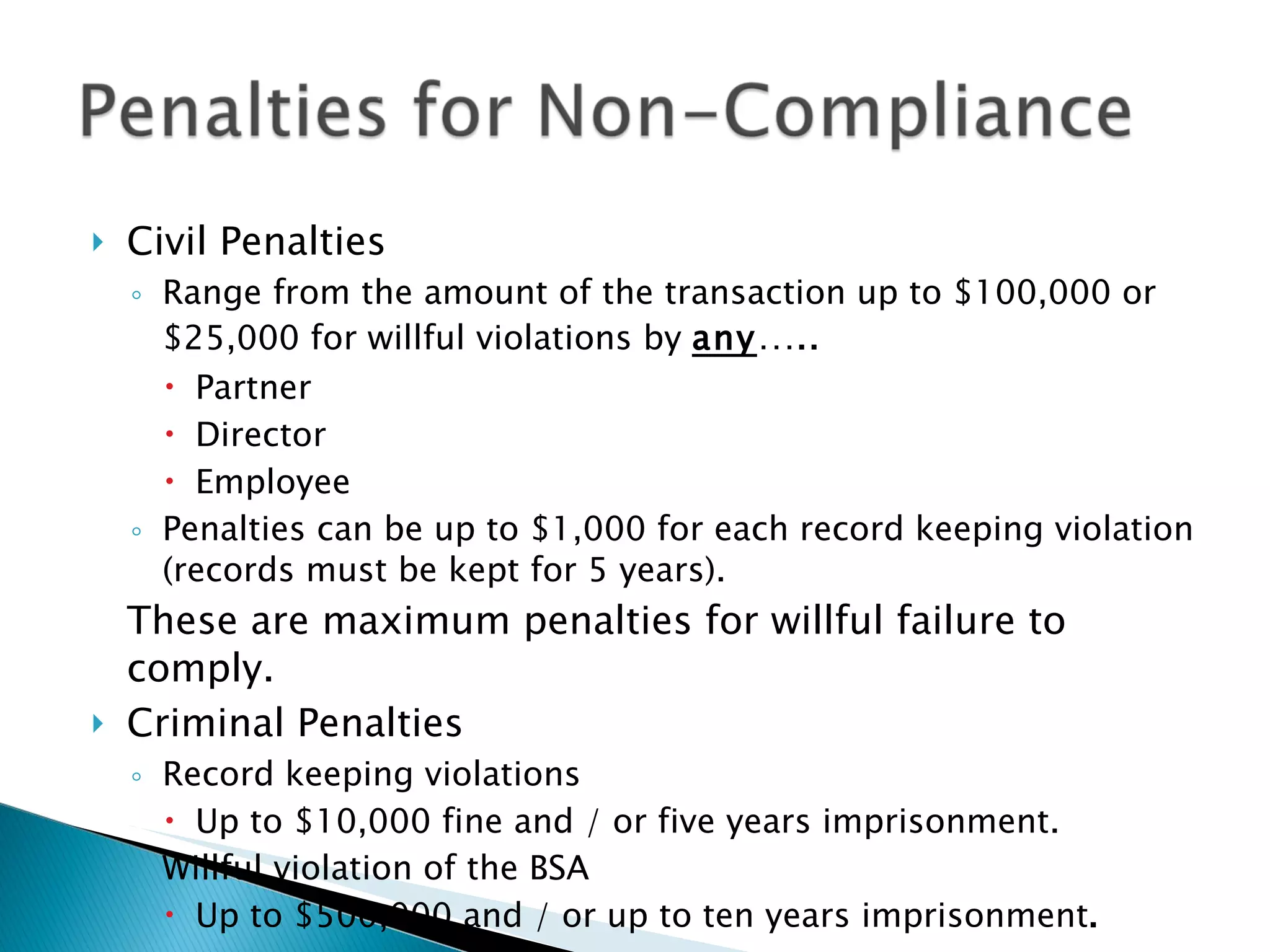

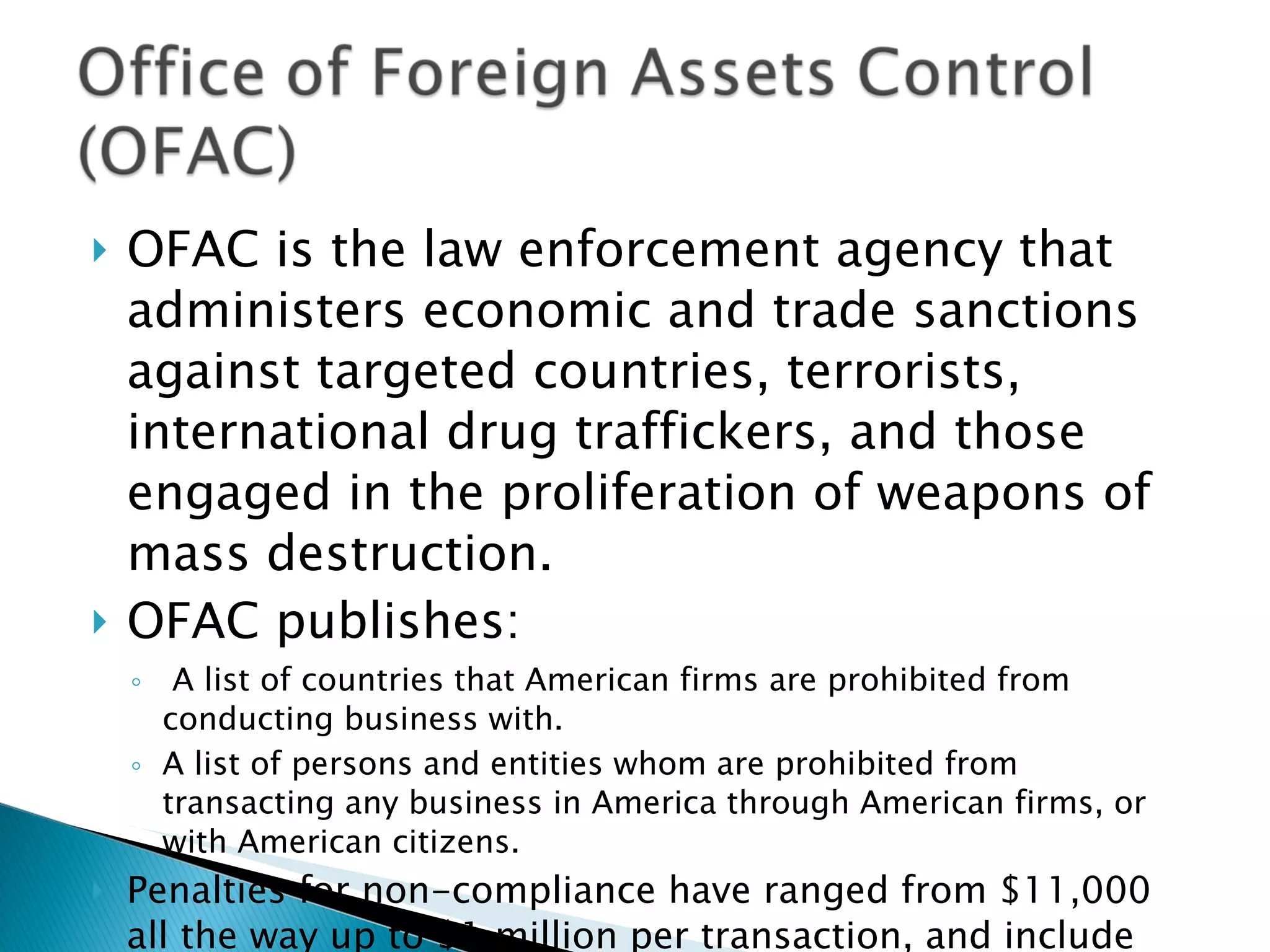

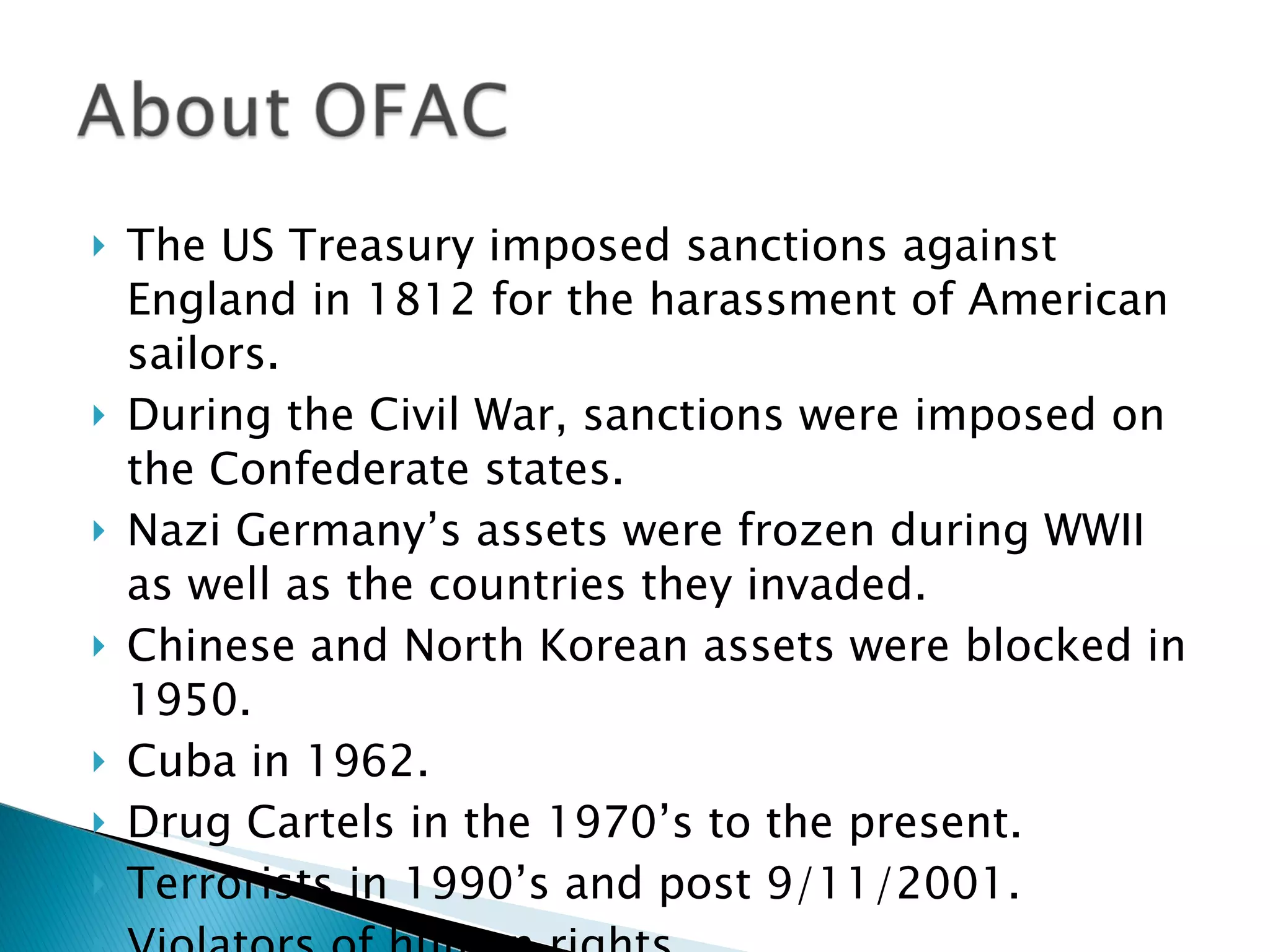

The document discusses several pieces of US legislation aimed at combating money laundering and other financial crimes. It outlines laws such as the Bank Secrecy Act of 1970, Money Laundering Control Act of 1986, Anti-Drug Abuse Act of 1988, and the USA PATRIOT Act of 2001. These laws established reporting requirements for financial institutions, made money laundering a federal crime, increased penalties for noncompliance, and enhanced anti-money laundering efforts. The document also discusses the role of the Office of Foreign Assets Control (OFAC) in administering sanctions and publishing restricted lists.