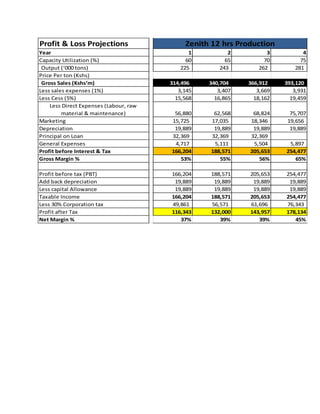

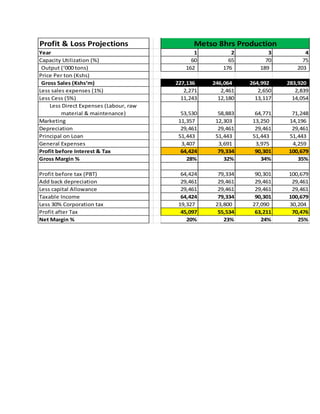

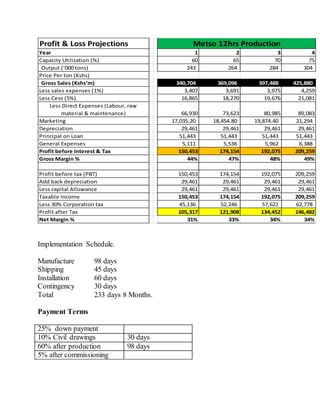

Teyomi International Limited plans to open a quarry to take advantage of high demand for chippings from ongoing infrastructure projects. The quarry will produce chippings through blasting, crushing, and grading raw materials extracted from stone deposits. It will be run by a production, administration, and accounting department, employing up to 15 workers. Financial projections estimate revenues of 209-262 million Kenyan shillings annually over 5 years based on projected output volumes and prices. Capital costs of 180 million shillings will be financed by equity and bank loans.