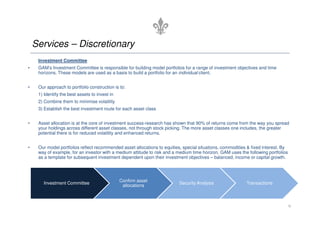

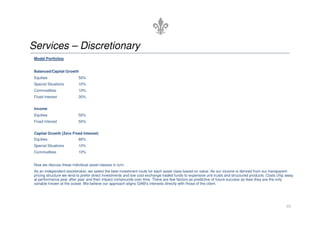

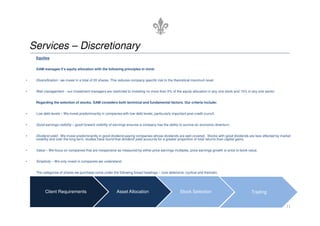

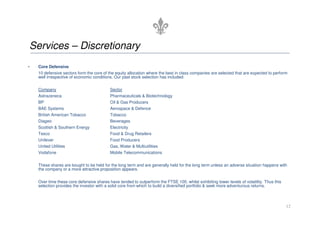

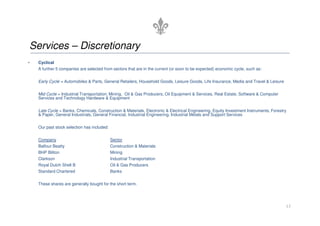

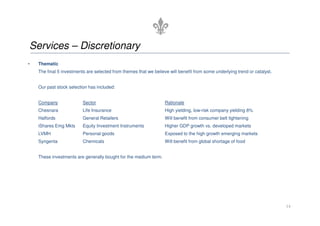

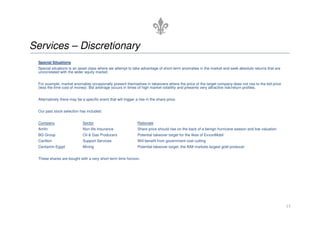

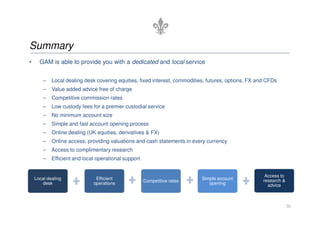

Gibraltar Asset Management provides various investment services including execution-only dealing, advisory services, and discretionary portfolio management. For discretionary clients, GAM constructs model portfolios consisting of equities, fixed income, commodities, and special situations. Equity holdings are selected based on criteria like low debt, earnings visibility, dividends, and value. Fixed income, commodities, and special situations further diversify portfolios. Clients receive regular reporting and their assets are held securely with a third-party custodian.