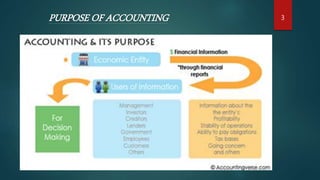

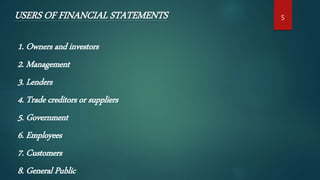

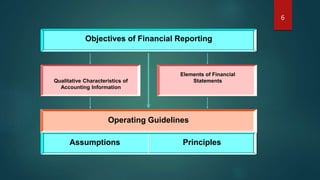

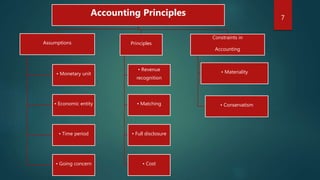

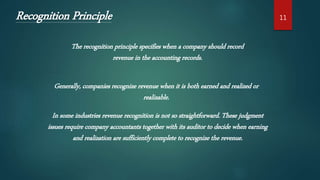

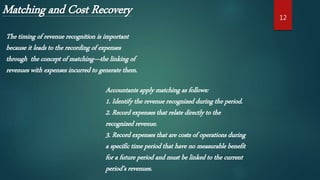

This document provides an overview of accounting principles and financial statements. It discusses that accounting involves recording business transactions in monetary terms and interpreting the results. The main purposes of accounting are to provide quantitative financial information to help with economic decision making. Key users of financial statements are identified such as owners, management, lenders and the government. The document then discusses accounting principles like the revenue recognition principle and matching principle. It defines the objectives of financial reporting and elements of financial statements. Finally, it provides details on the nature of accounting systems and how they communicate financial information to stakeholders through financial reports.

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)