Downloaded 48 times

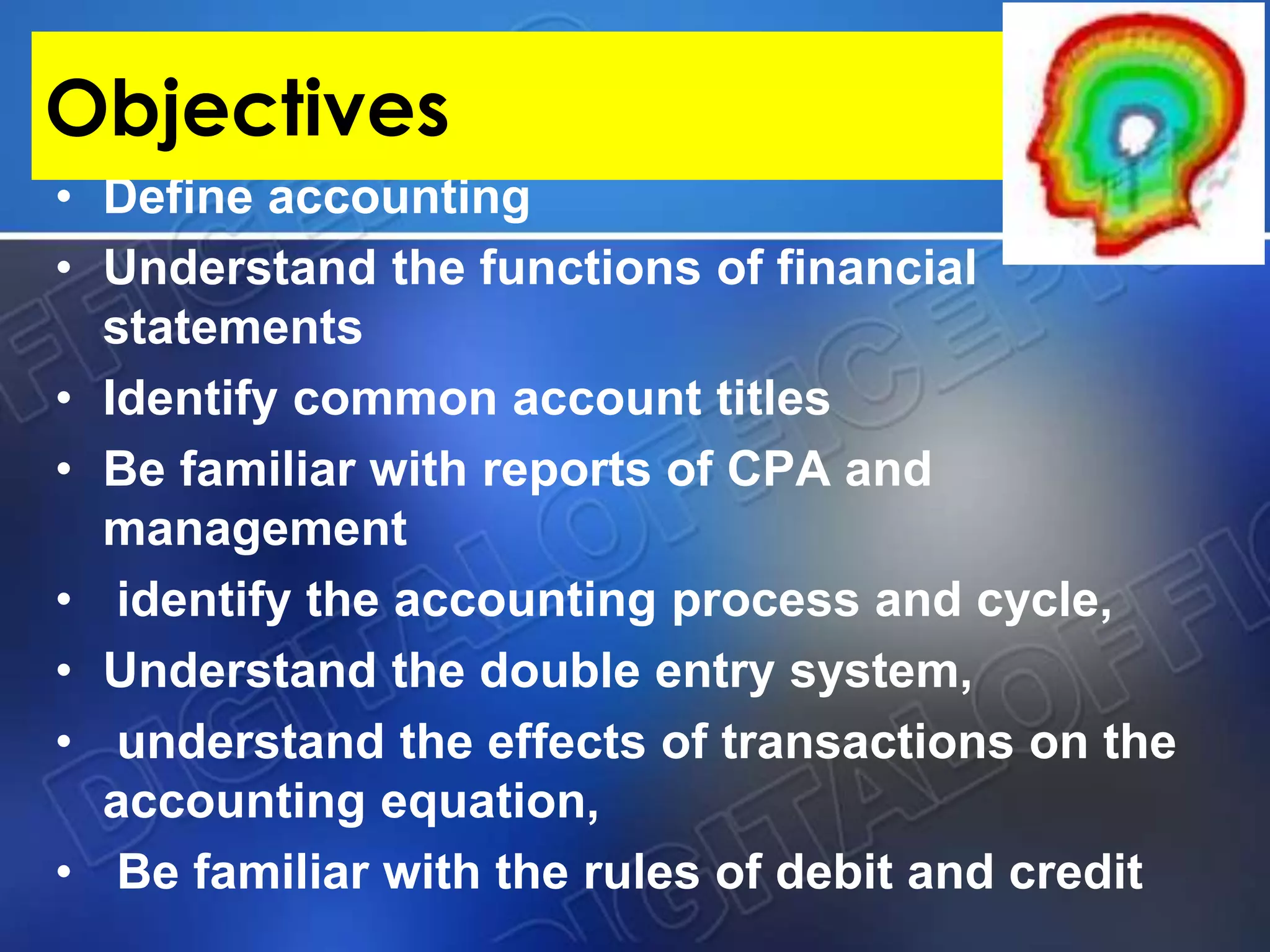

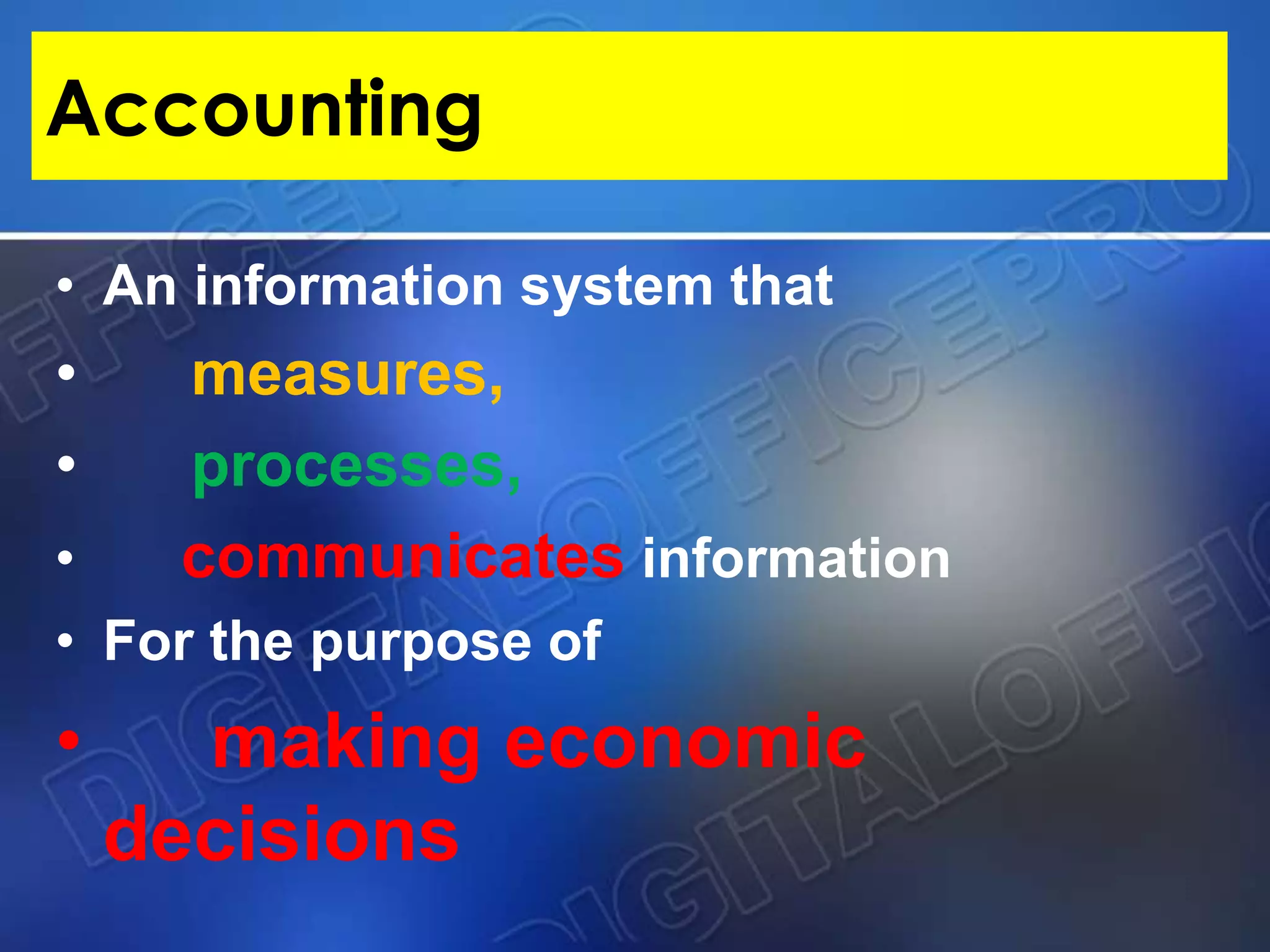

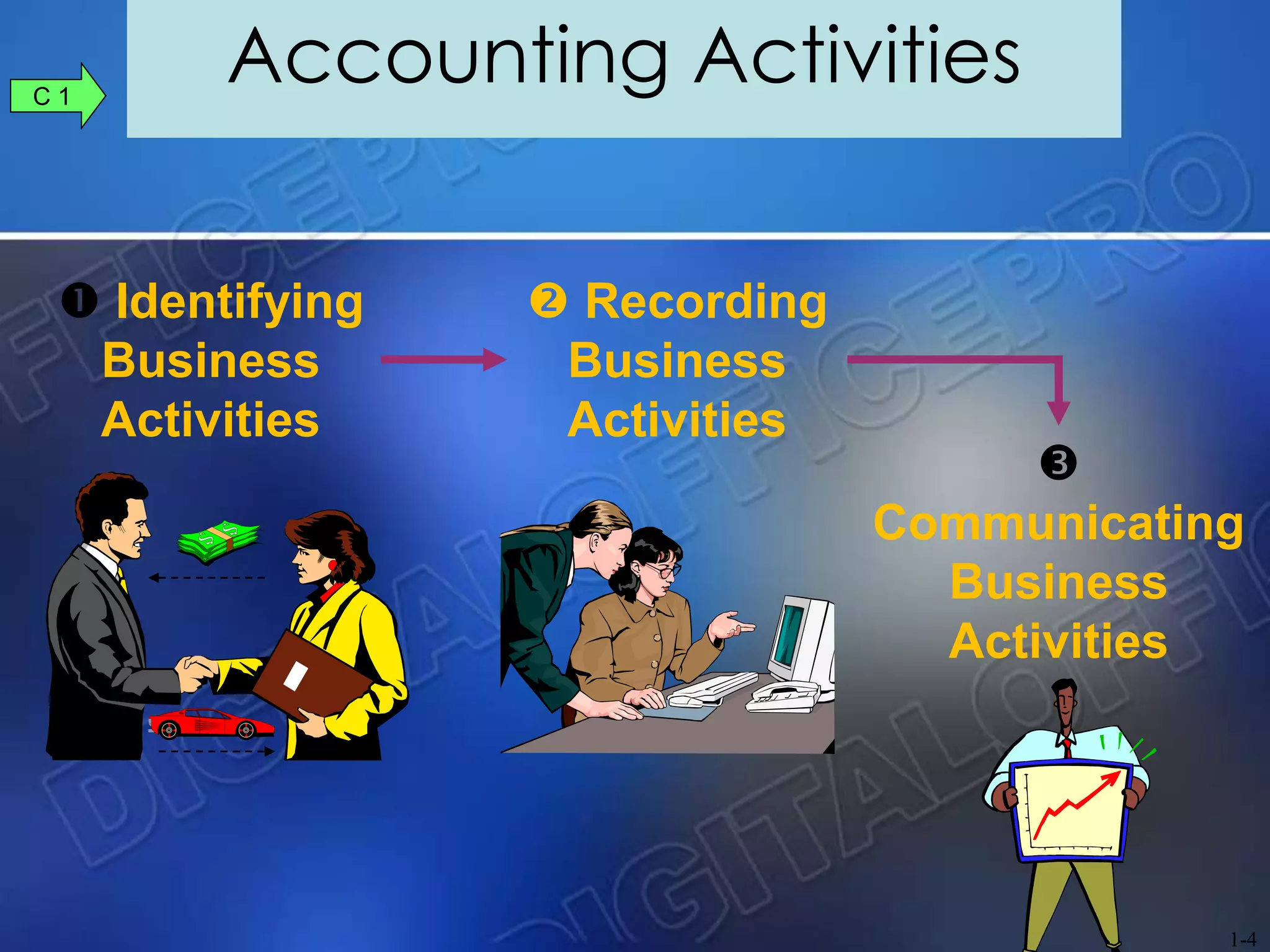

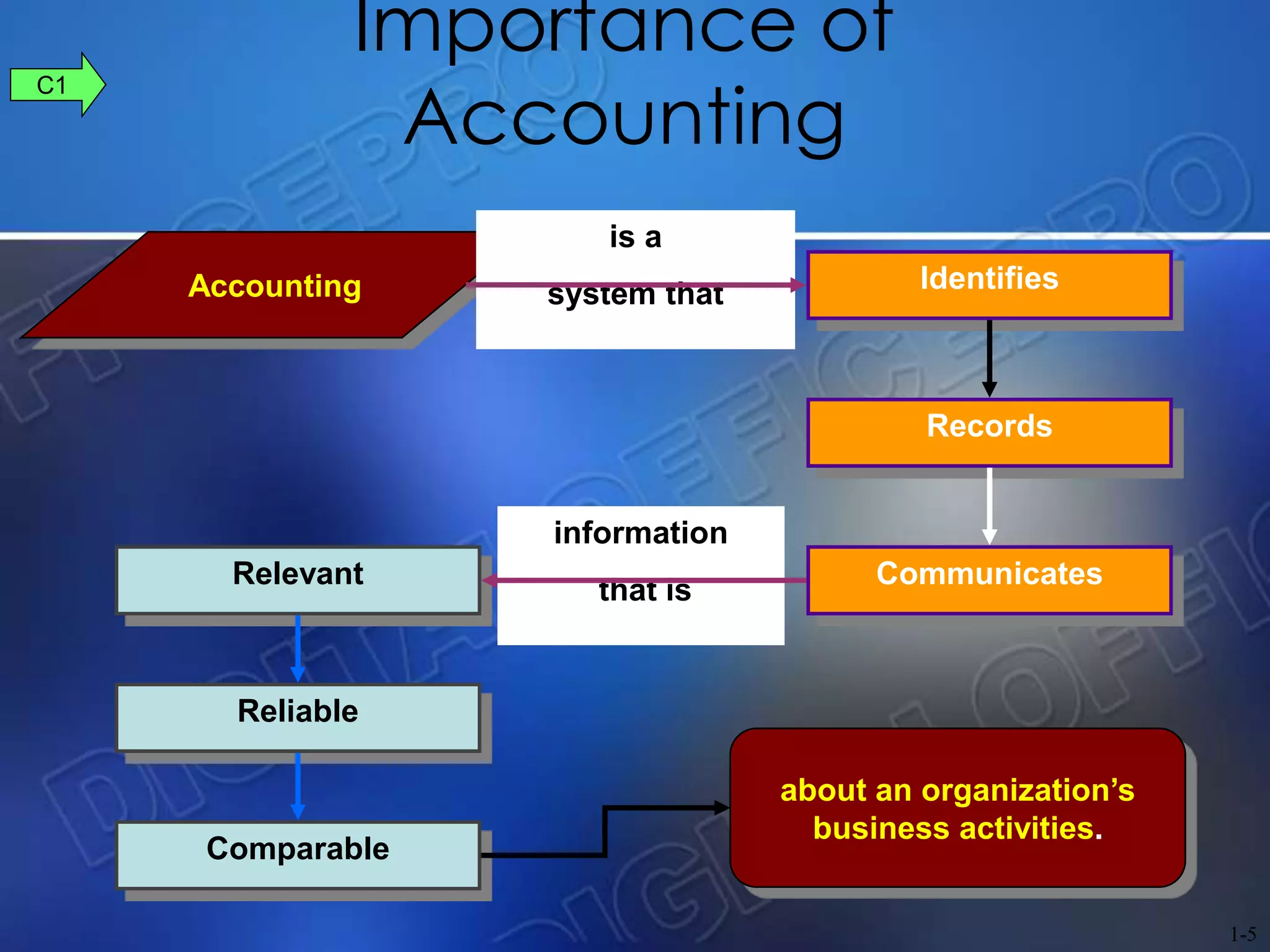

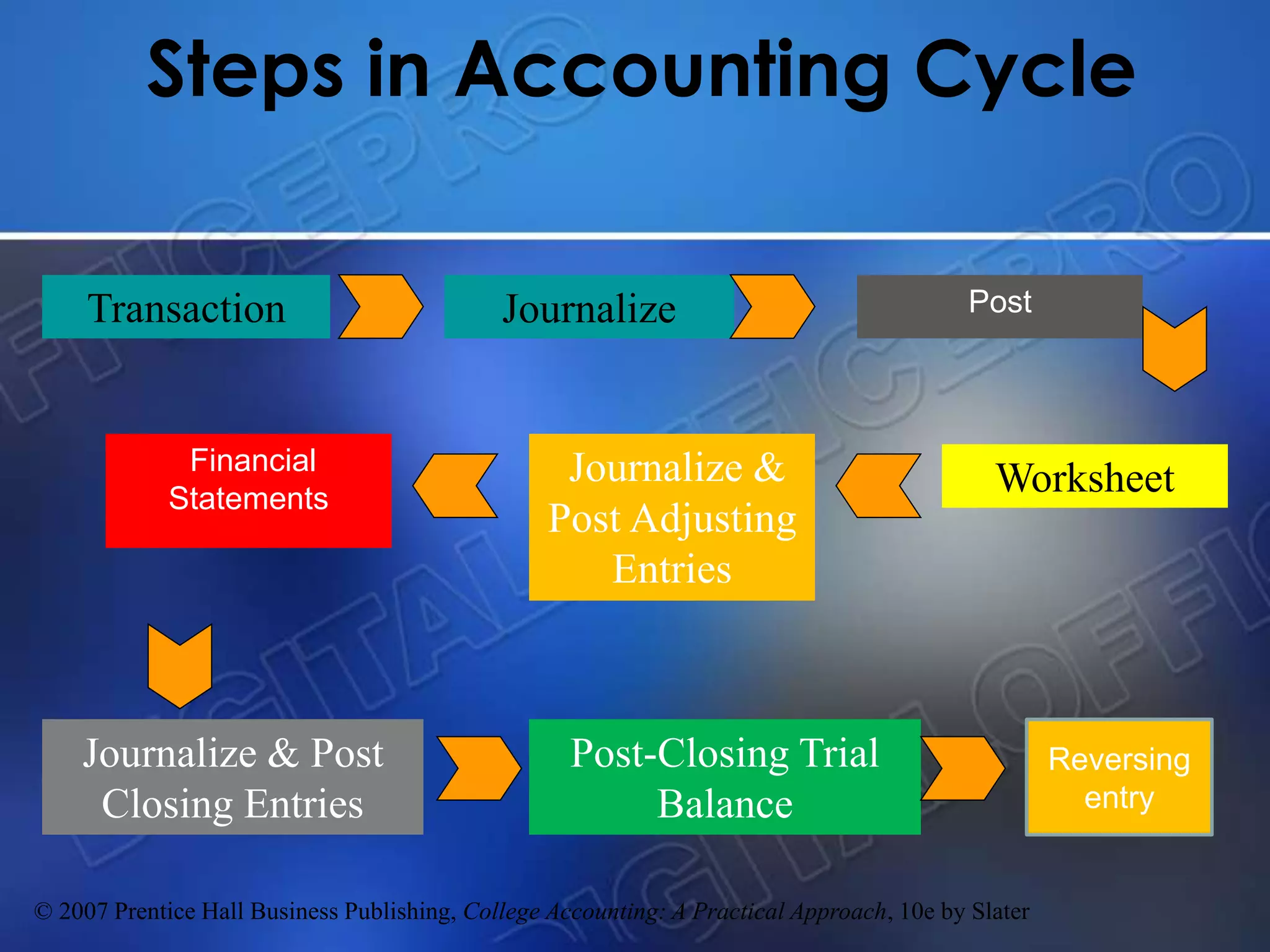

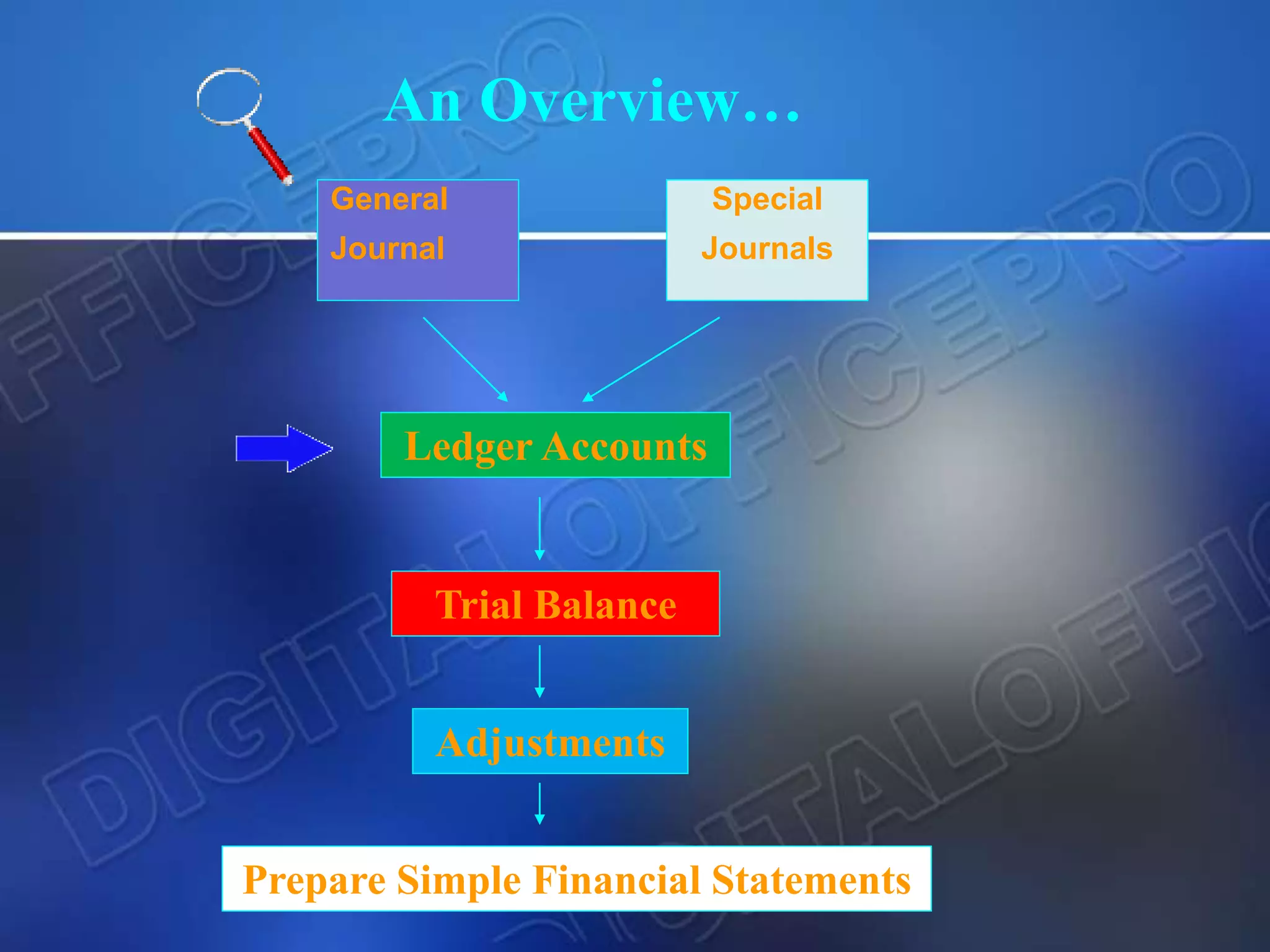

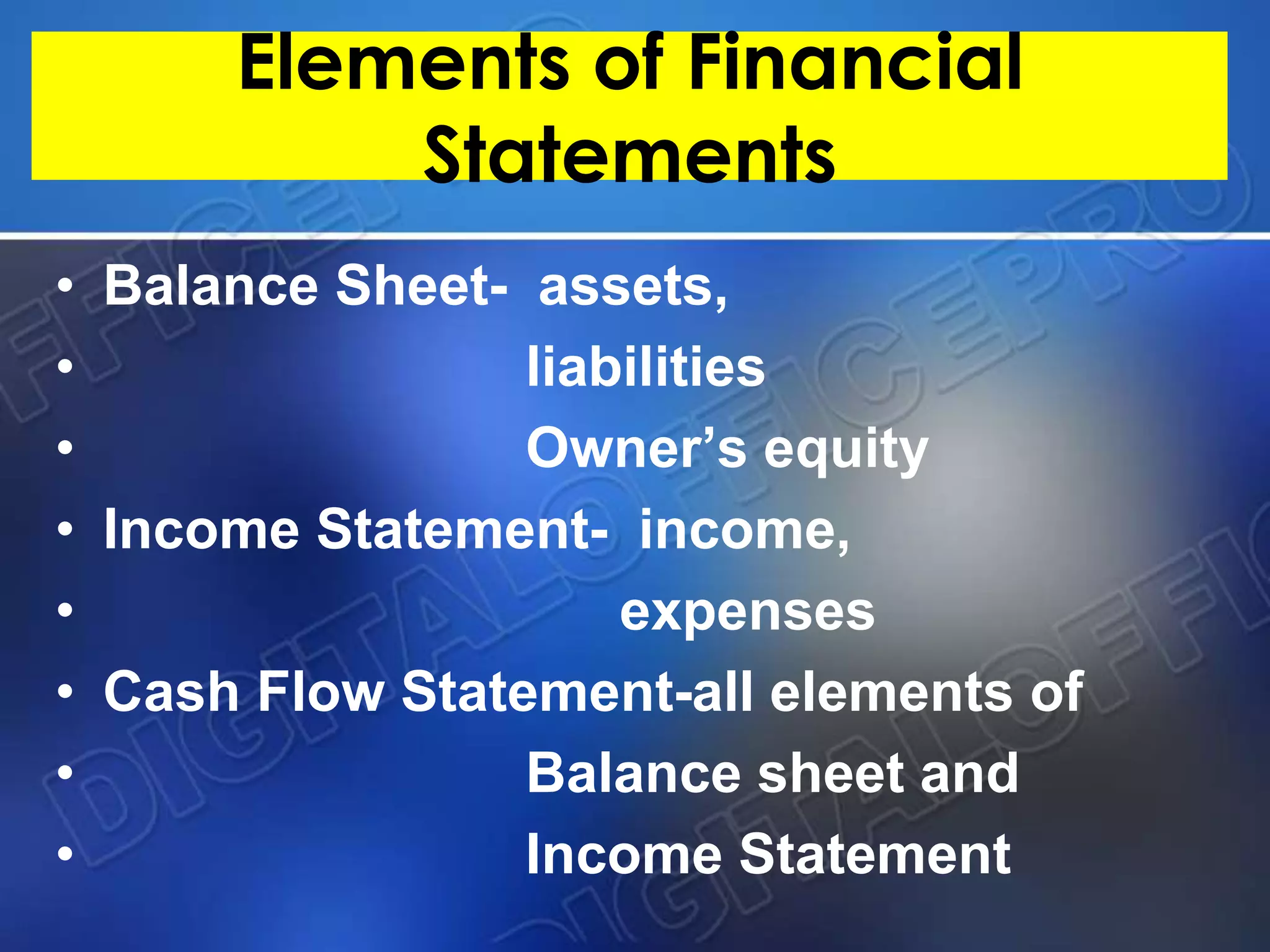

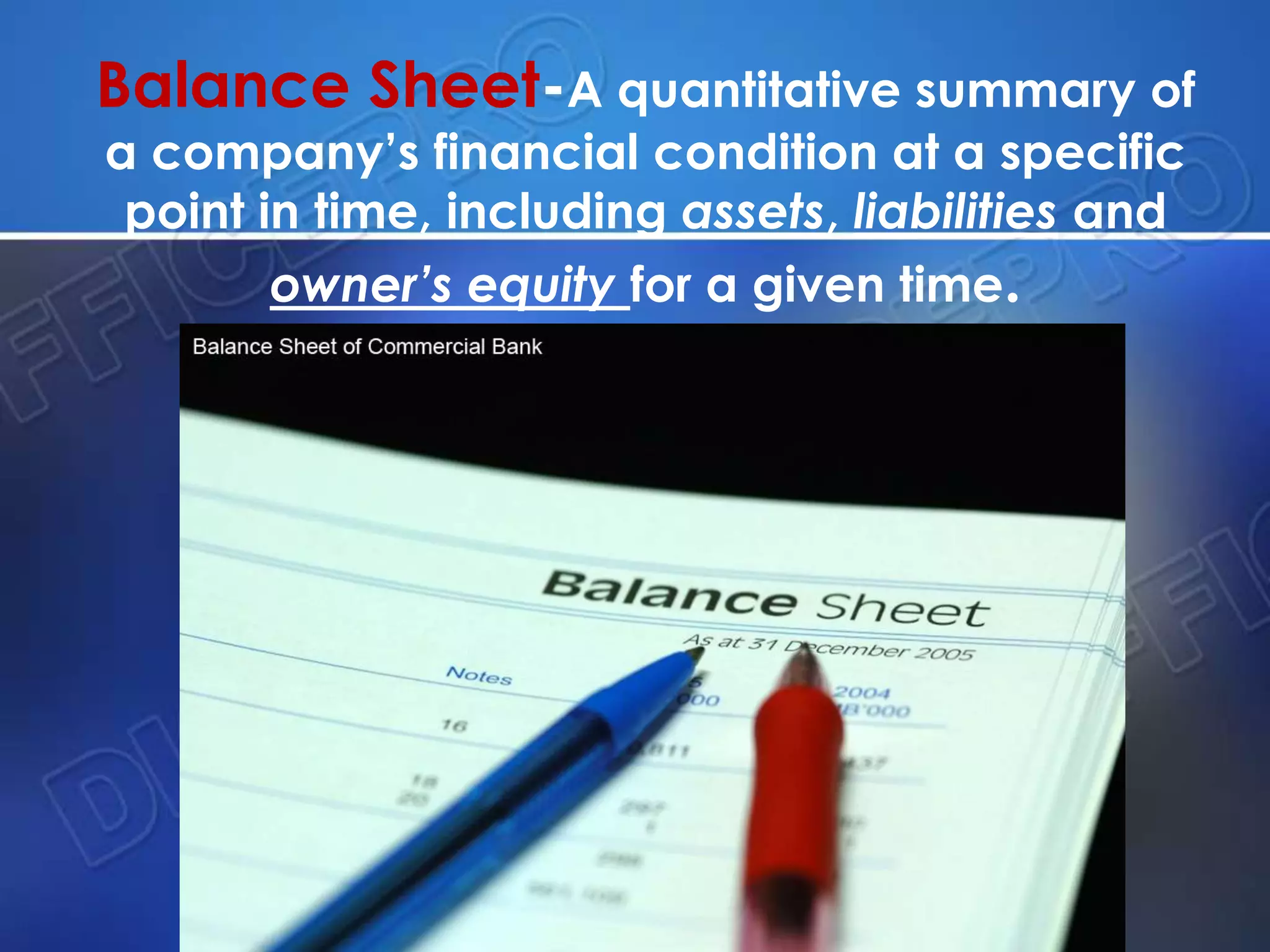

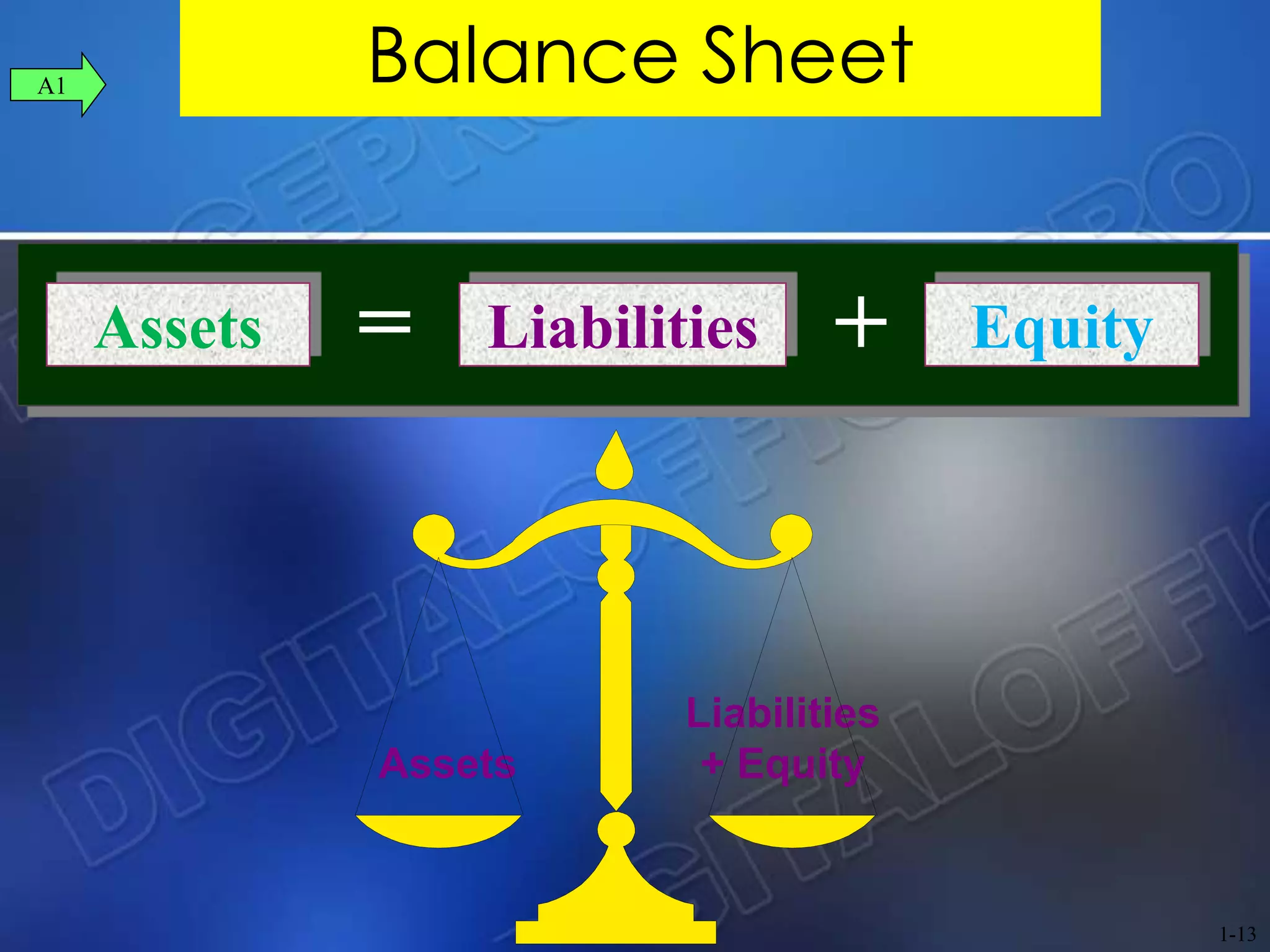

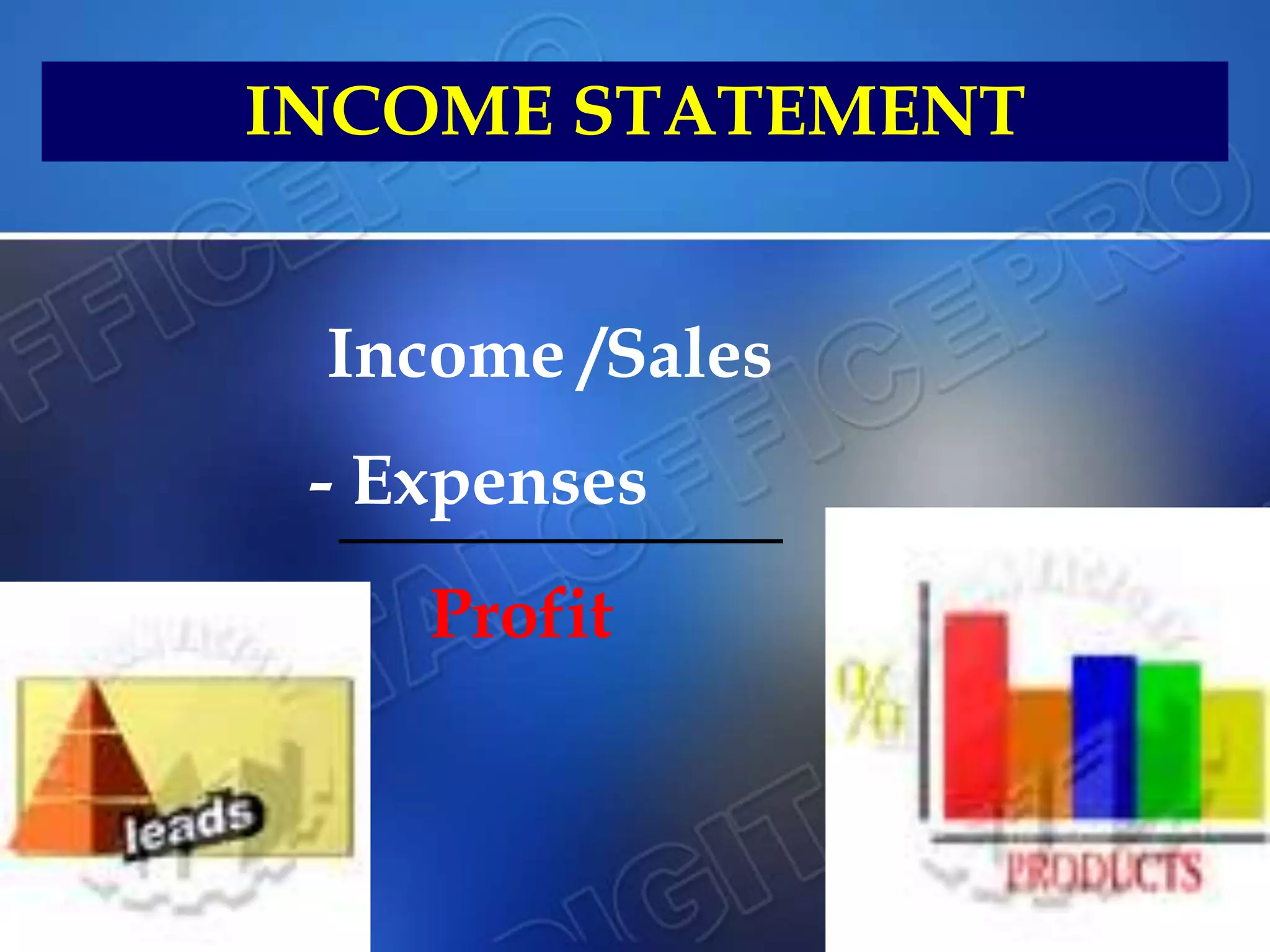

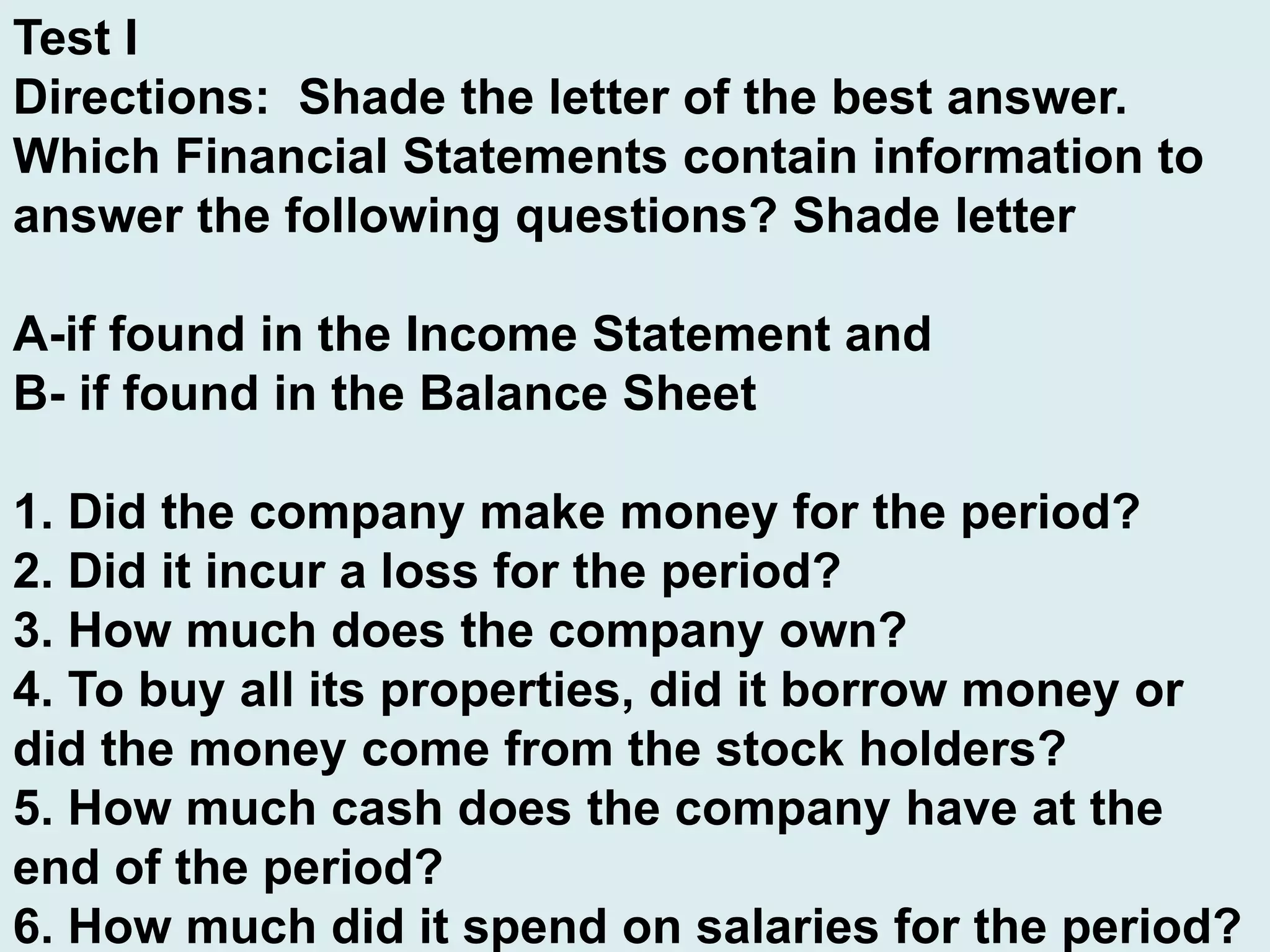

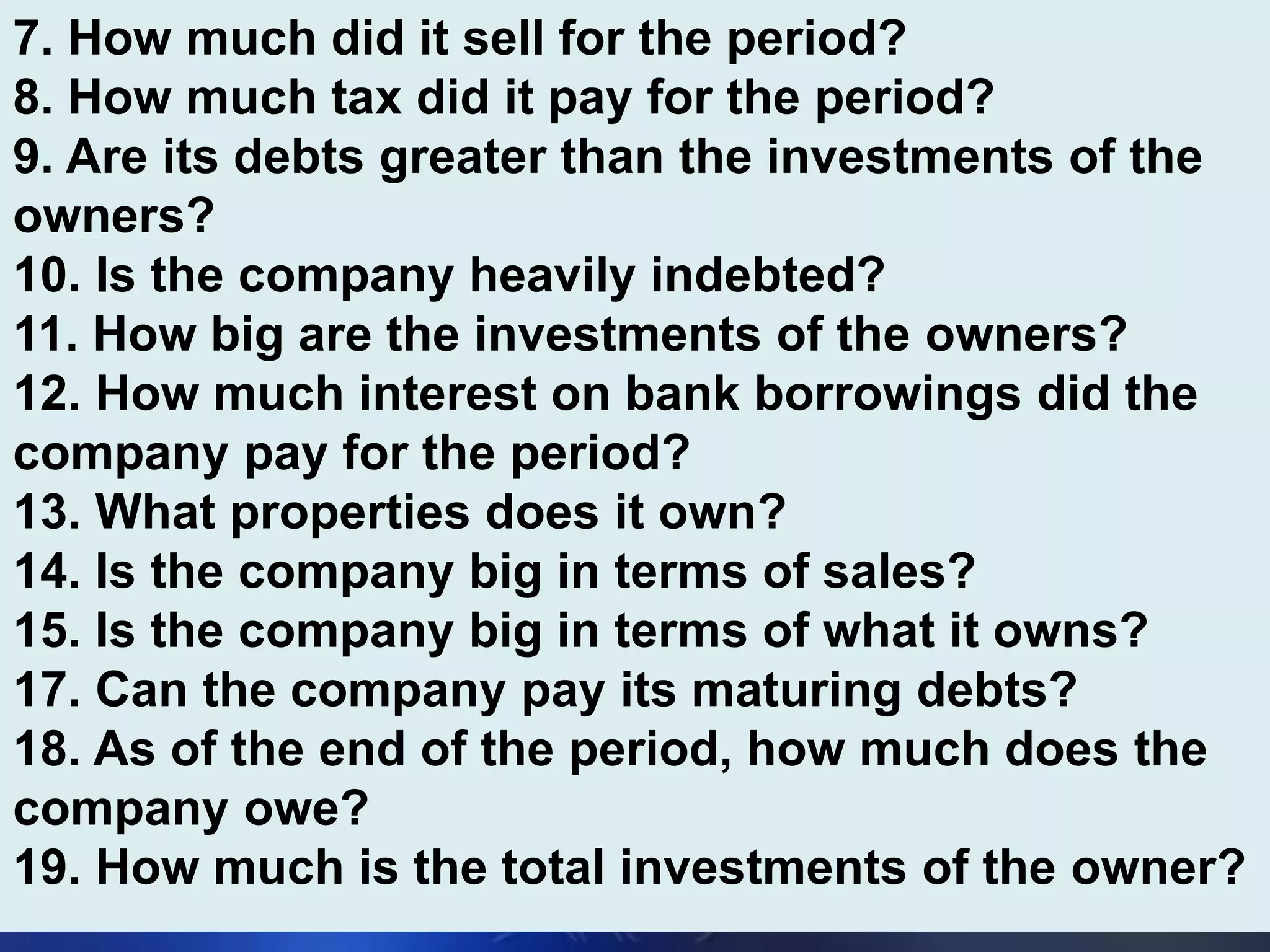

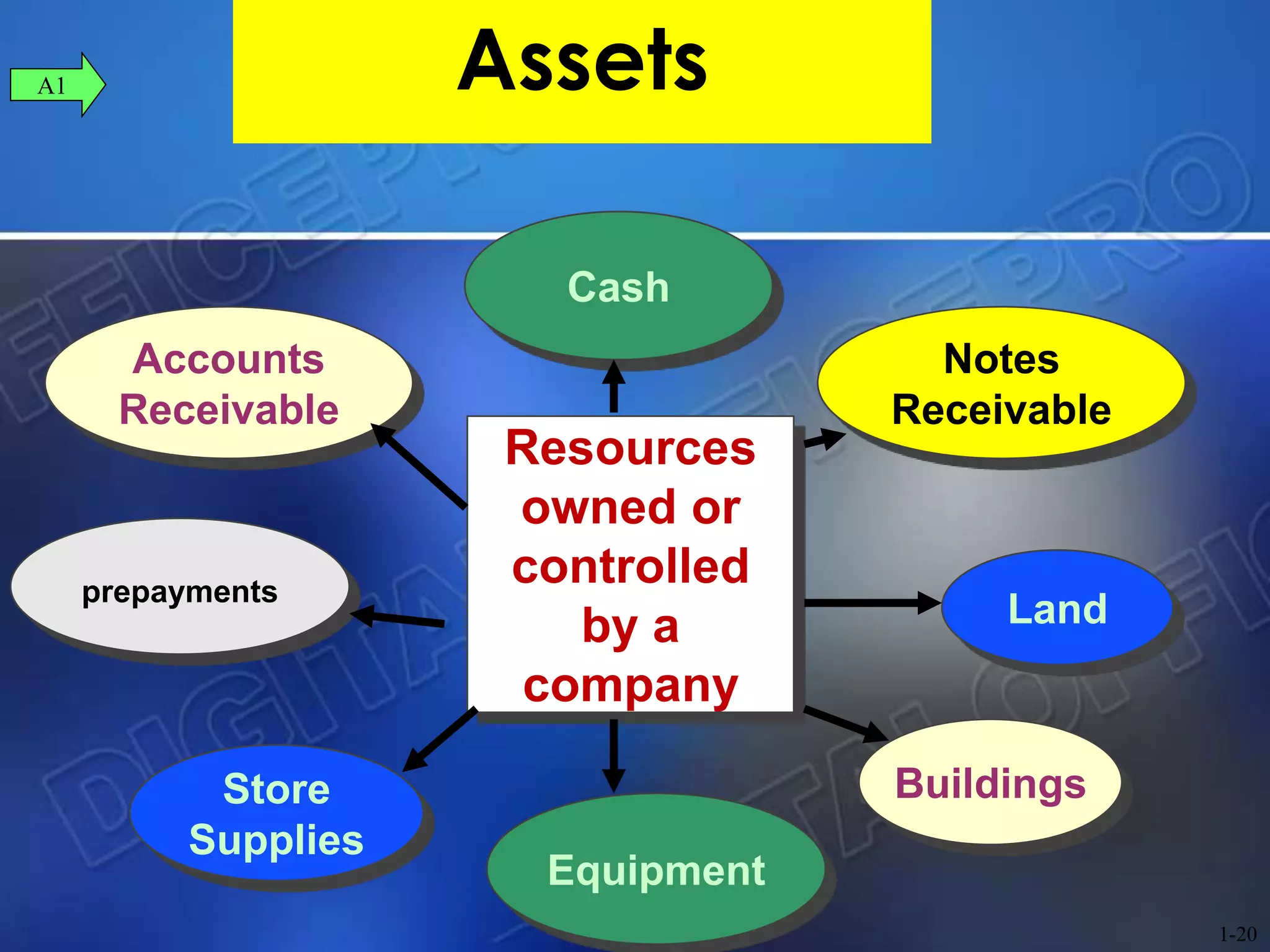

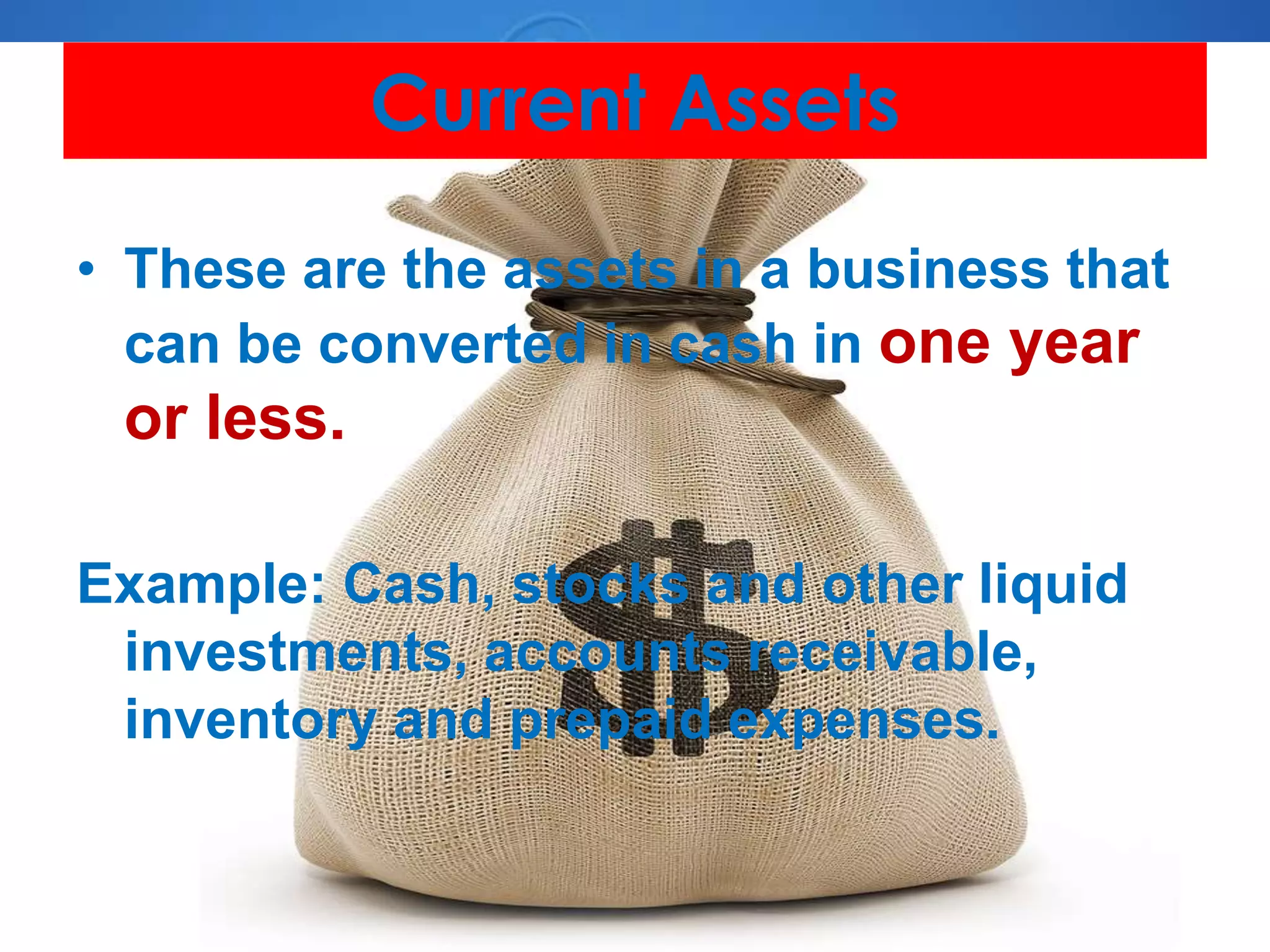

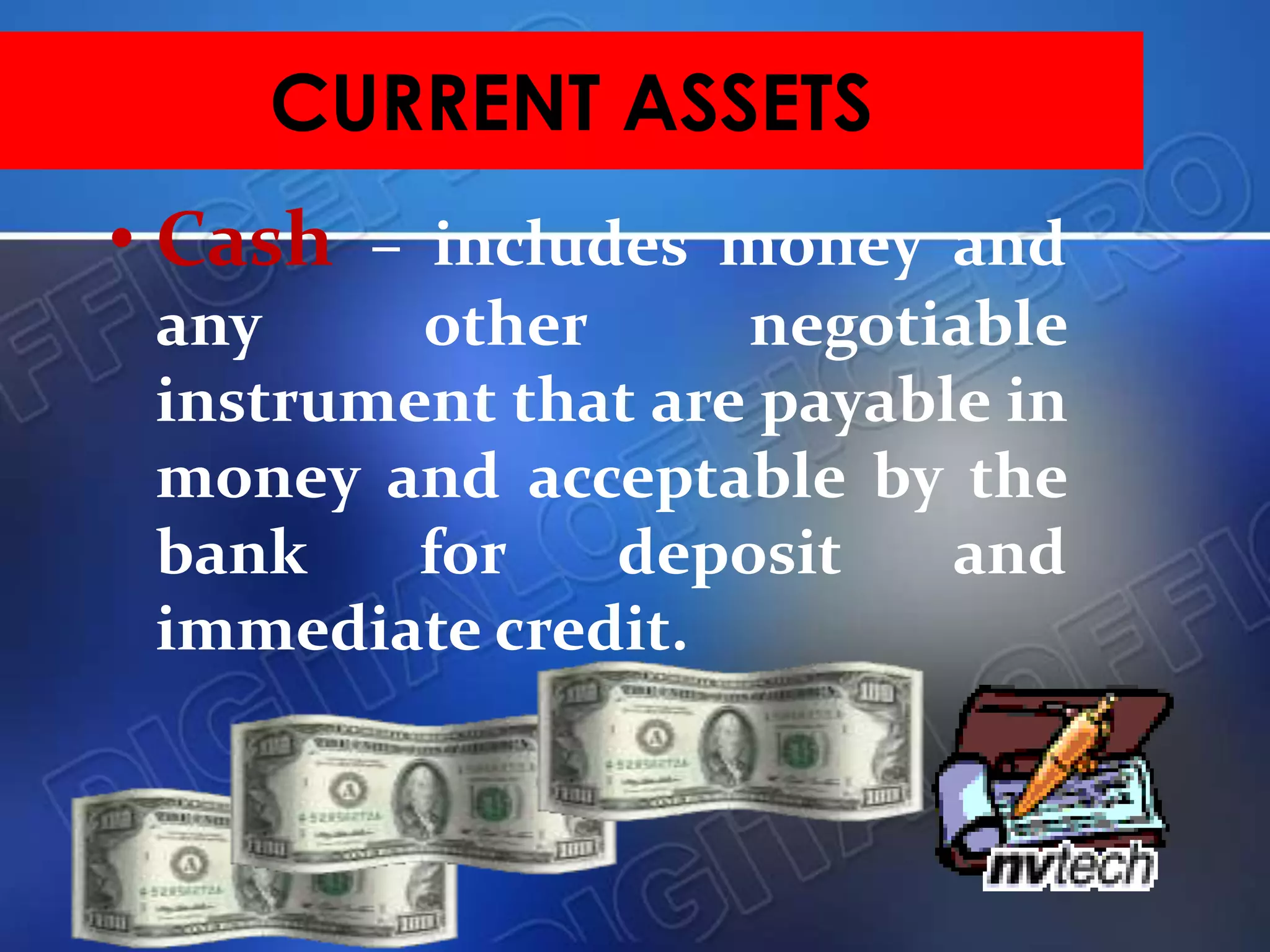

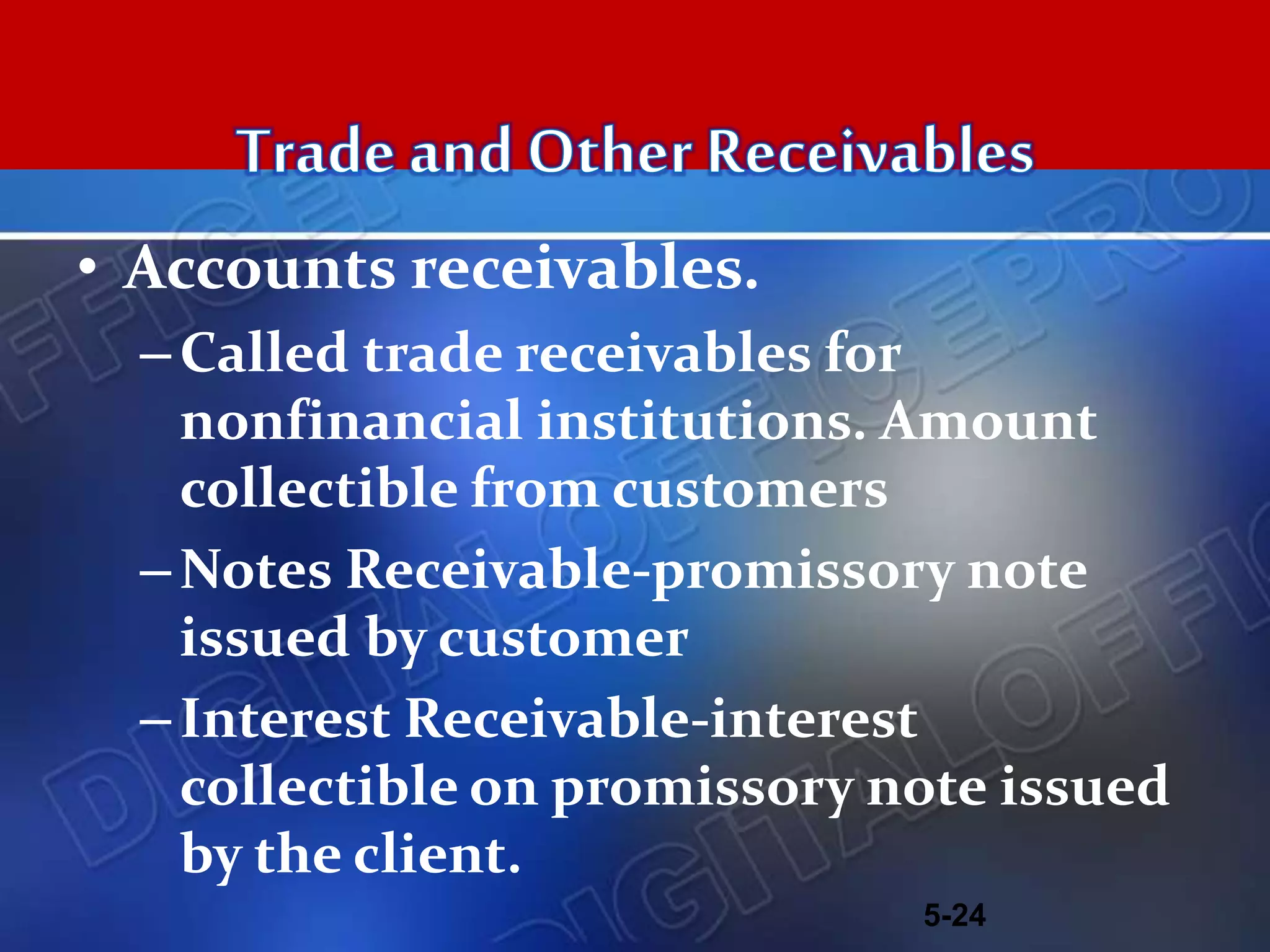

This document provides an overview of introductory accounting concepts including: - The definition and objectives of accounting as an information system that measures, processes, and communicates financial information. - The accounting process and cycle including identifying transactions, recording them, and communicating financial statements. - The key financial statements - balance sheet, income statement, statement of cash flows - and what financial information they provide. - Common accounts and how transactions affect the accounting equation.

![[PREMONEY 2013] Karthik Reddy](https://cdn.slidesharecdn.com/ss_thumbnails/karthikreddy6-20-130625162721-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)