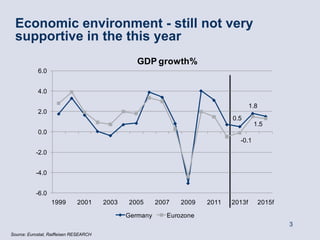

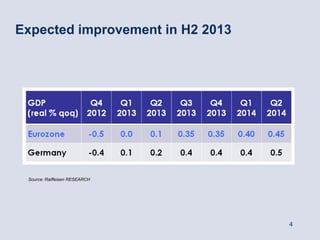

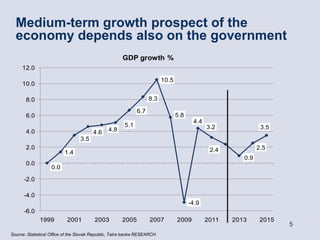

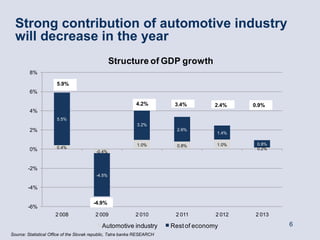

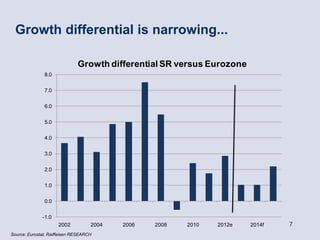

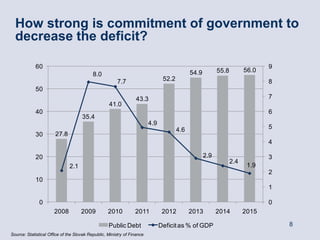

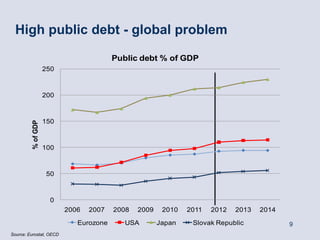

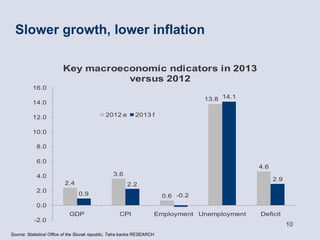

The document discusses the economic outlook for Slovakia in 2013, highlighting a growth projection of 1.5% amid ongoing challenges from the eurozone debt crisis. It emphasizes the importance of government policy and the automotive industry’s declining contribution to GDP growth. The overall economic environment is characterized by high public debt and lower inflation compared to previous years.