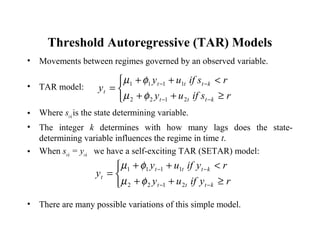

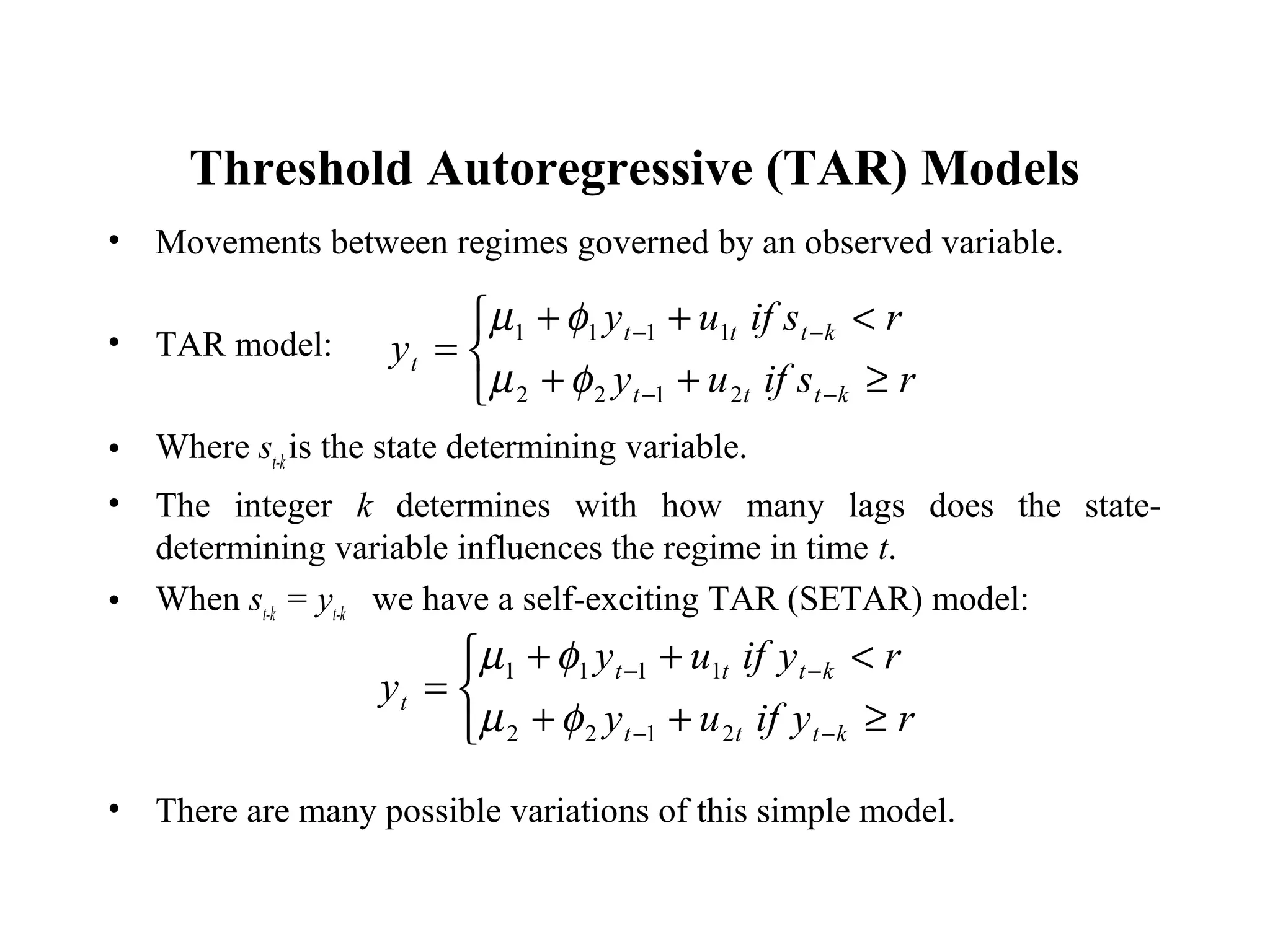

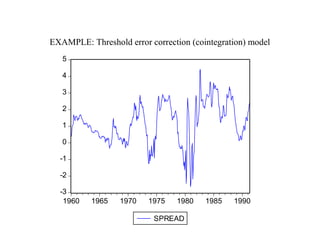

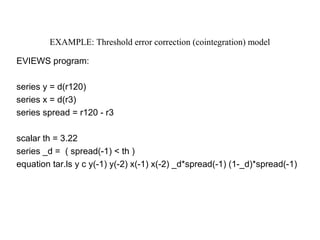

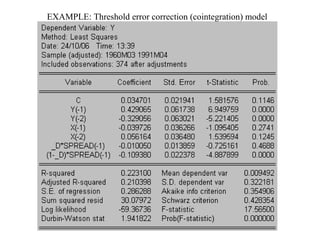

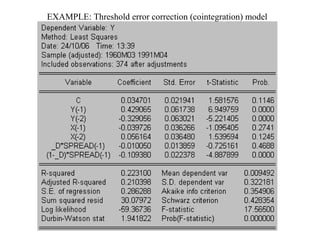

Threshold Autoregressive (TAR) models allow for movements between regimes that are governed by an observed variable. A TAR model contains different parameters depending on whether the state-determining variable is above or below a certain threshold. A self-exciting TAR (SETAR) model occurs when the state-determining variable is a lag of the dependent variable. There are many possible variations of the basic TAR model, including models with switching in some but not all parameters, models with more than two regimes, and models with different threshold variables or dynamic specifications.

![Getting Started with Apache Spark: Big Data Made Simple [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/apachesparkgettingstarted-260203175547-8361bcc3-thumbnail.jpg?width=640&height=640&fit=bounds)