Download to read offline

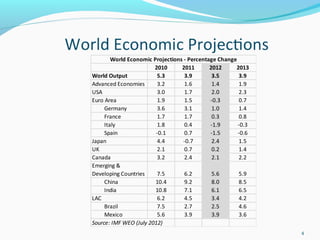

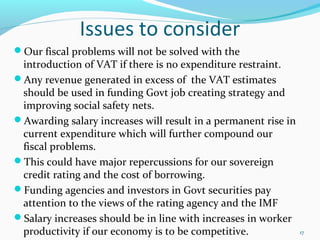

![8

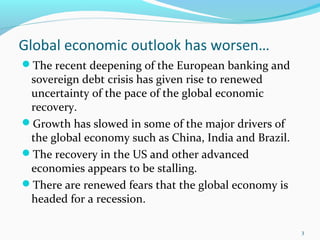

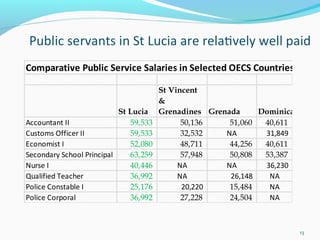

2007/08r 2008/09r 2009/10r 2010/11r 2011/12pre

TOTAL REVENUE AND GRANTS 753.10 829.03 826.79 873.91 921.63

Current Revenue 741.23 804.87 759.62 787.18 828.76

Tax Revenue 687.74 737.74 700.76 736.34 757.39

Non Tax Revenue 53.49 67.13 58.86 50.85 71.37

TOTAL EXPENDITURE 811.34 856.82 925.08 1,041.04 1,183.25

Capital Expenditure 230.70 208.17 241.31 298.57 402.60

Current Expenditure 580.64 648.65 683.77 742.47 780.65

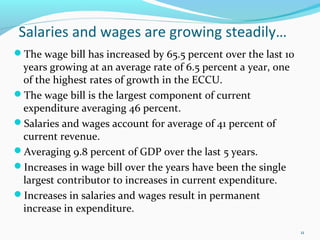

Salaries & Wages 266.97 301.07 316.15 342.30 350.31

Current Balance 160.59 156.22 75.85 44.71 48.11

Primary Balance 26.27 60.68 -11.54 -65.38 -150.45

Overall Balance -58.24 -27.79 -98.29 -167.13 -261.62

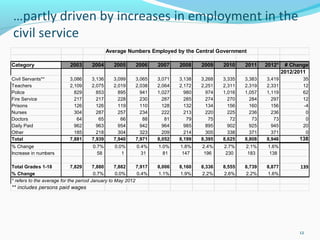

Salaries and Wages Account for Single Largest Share of Increaes in Current Expenditure

Increases in Current Expenditure ($ Mil.) 25.77 68.01 35.12 58.70 38.18

Increases in Salaries and Wages ($ Mil.) 11.32 34.10 15.08 26.15 8.01

S & W as Percentage Share of Increases 43.9% 50.1% 42.9% 44.5% 21.0% 40.5%

CENTRAL GOVERNMENT

SUMMARY OF FISCAL OPERATIONS [Fiscal Year]

ECONOMIC CLASSIFICATION

(EC$ Millions)](https://image.slidesharecdn.com/presentationonupdateofmacroeconomicframeworkfornegotiations21-130812212223-phpapp01/85/Presentation-on-update-of-macroeconomic-framework-for-negotiations-2-1-8-320.jpg)

The document summarizes the current state of the global and Saint Lucian economies. It notes that the global economic outlook has worsened as growth has slowed in major economies like China, India, and Brazil. This slowing is expected to negatively impact Saint Lucia through lower tourism, FDI, exports, and grants. Saint Lucia's growth is projected to be below targets for 2012 due to these mounting risks. The government's fiscal position is also expected to deteriorate as the recurrent deficit exceeds targets and revenues fall short. Salaries and wages comprise the largest share of expenditures and have been steadily increasing, posing challenges. Recommendations include foregoing salary increases this period to address fiscal issues and risks to the economy.