The document provides an overview of transfer pricing regulations in India. It discusses:

1) The legal framework governing transfer pricing, including key sections of the Income Tax Act relating to computation of income from international transactions at arm's length prices.

2) The procedures involved in transfer pricing assessments, including reference to the transfer pricing officer, draft order process, and appeal mechanisms.

3) Methods for determining arm's length prices for international transactions, including comparable uncontrolled price method, resale price method, cost plus method, profit split method, and transactional net margin method.

4) Requirements for transfer pricing documentation and the accountant's role in furnishing transfer pricing reports as required by section 92E of

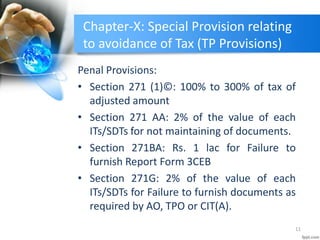

![Chapter-X: Special Provision relating

to avoidance of Tax (TP Provisions)

• The Explanatory Memorandum to the Finance Bill, 2001

explains the need for and the rationale for introduction of

transfer pricing provisions:

• ♦ The profits derived by such enterprises carrying to business

in India can be controlled by the multinational group, by

manipulating the prices charged and paid in such intra-group

transactions, thereby, leading to erosion of tax revenues.

• ♦ With a view to provide a statutory framework which can lead

to computation of reasonable, fair and equitable profits and

tax in India, in the case of such multinational enterprises, new

provisions were to be introduced in the Income-tax Act.

• Constitutional validity of chapter X provisions

• In Coca Cola India Inc. v. Asstt. CIT [2009] 177 Taxman 103

(Punj. & Har.), it was held that Chapter X of the Act was not

violative of Article 14 of the Constitution. Further, there was no

lack of the legislative competence for enacting the provisions

of sections 92 to 92F [as amended by the Finance Act, 2001,

with effect from 1-4-2002] contained in Chapter X of the Act.

5](https://image.slidesharecdn.com/finalpptforgurgaonbranchontp10102015new-160603043027/85/Presentation-on-Transfer-Pricing-5-320.jpg)

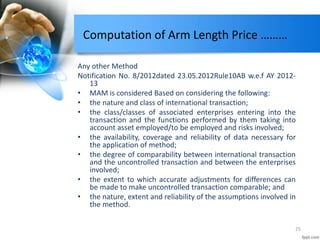

![Computation of Arm Length Price ………

• Obligation to compute income at arm’s length

price of all international transactions

• ALP--“Price between unrelated parties in

uncontrolled conditions” [Section 92F(ii)]

• ALP should be a mirror image of a price

charged for a similar transaction between two

unrelated entities transacting in uncontrolled

conditions;

• Price of a transaction in open market is

reflective of functions performed, assets

employed and risks Assumed i.e.(FAR Analysis);

• FAR Analysis helps to identify the adjustments

required and judging comparability under Rule

10B(2) and Rule 10B(3).

17](https://image.slidesharecdn.com/finalpptforgurgaonbranchontp10102015new-160603043027/85/Presentation-on-Transfer-Pricing-17-320.jpg)