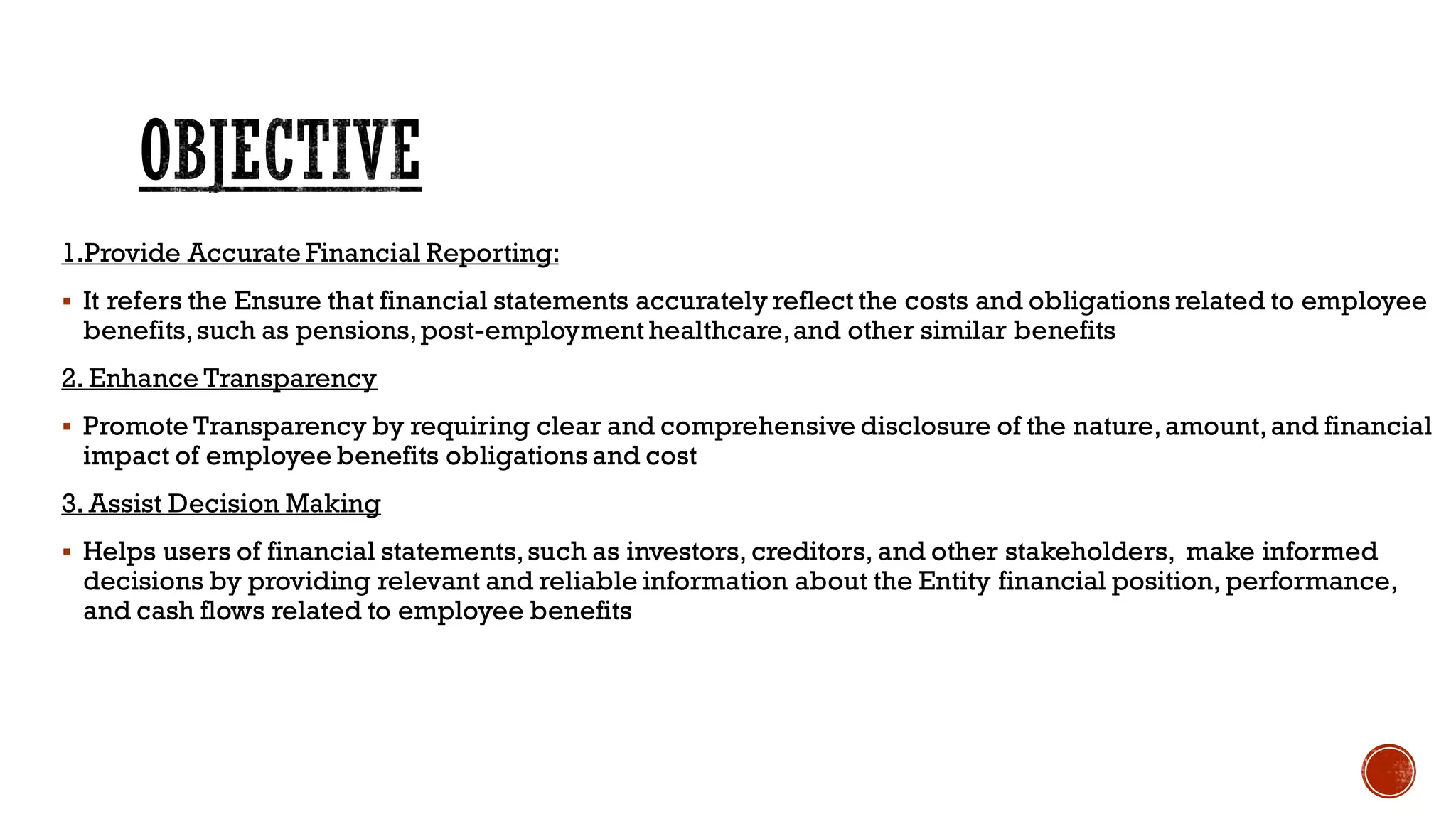

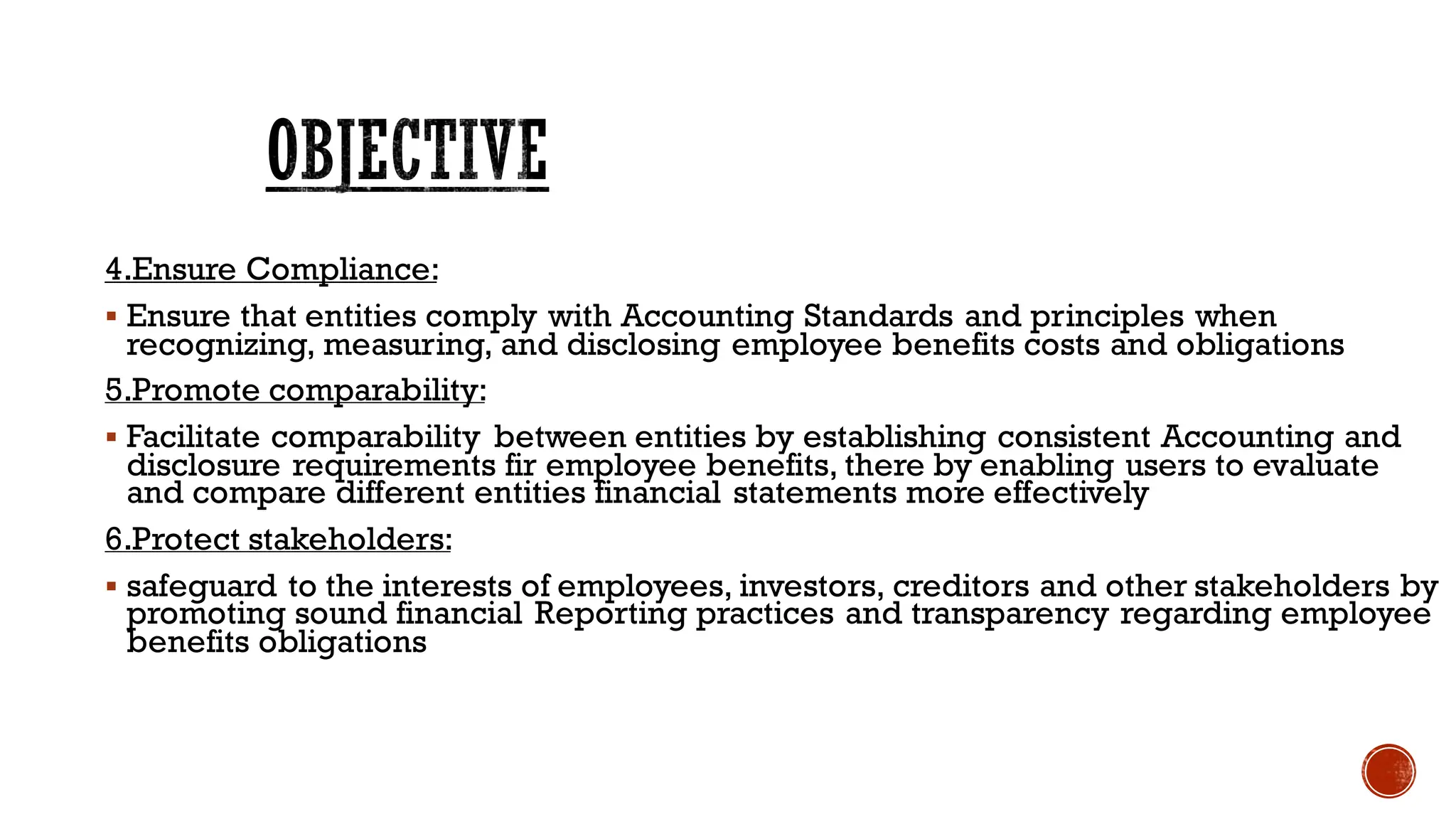

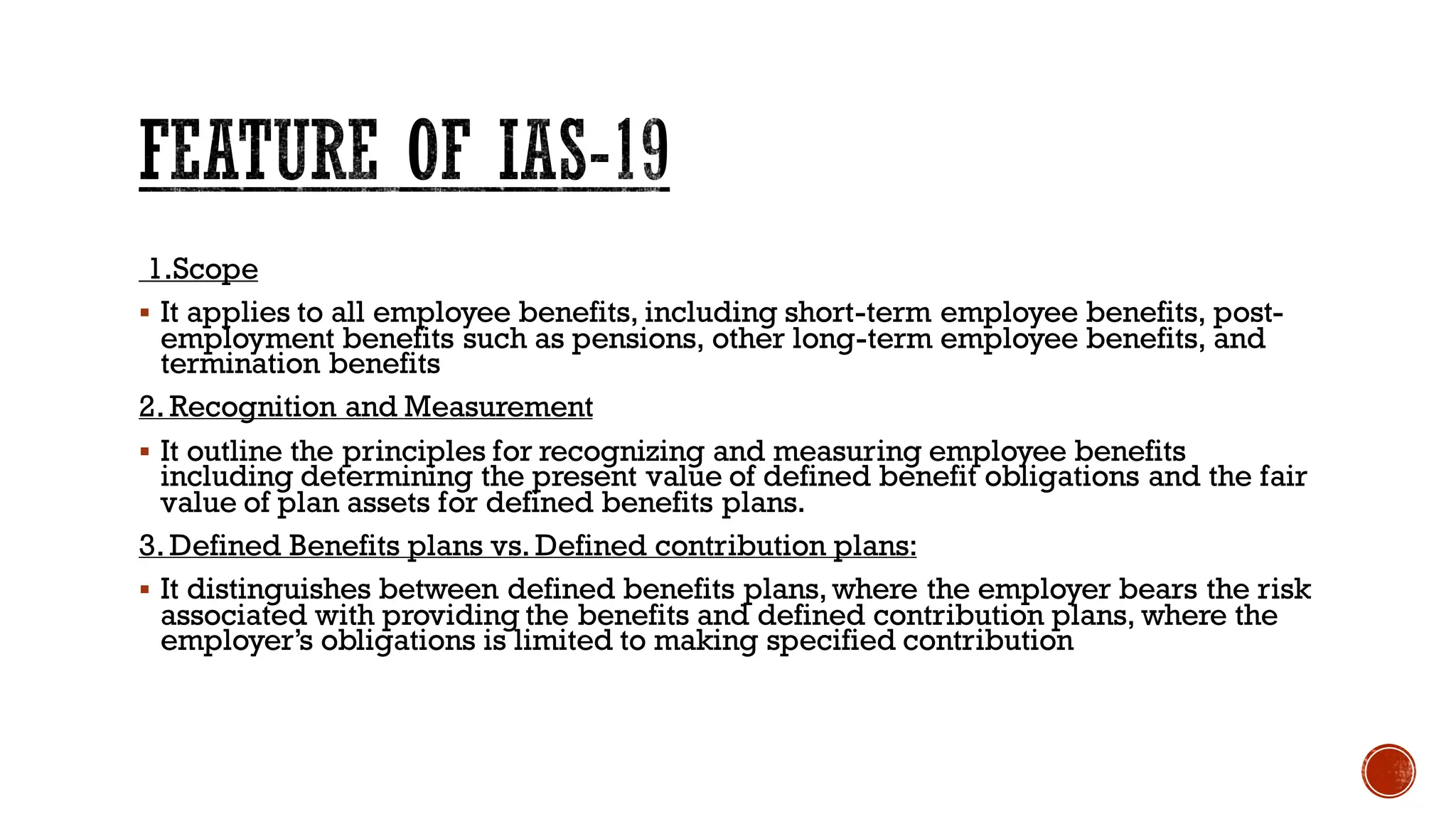

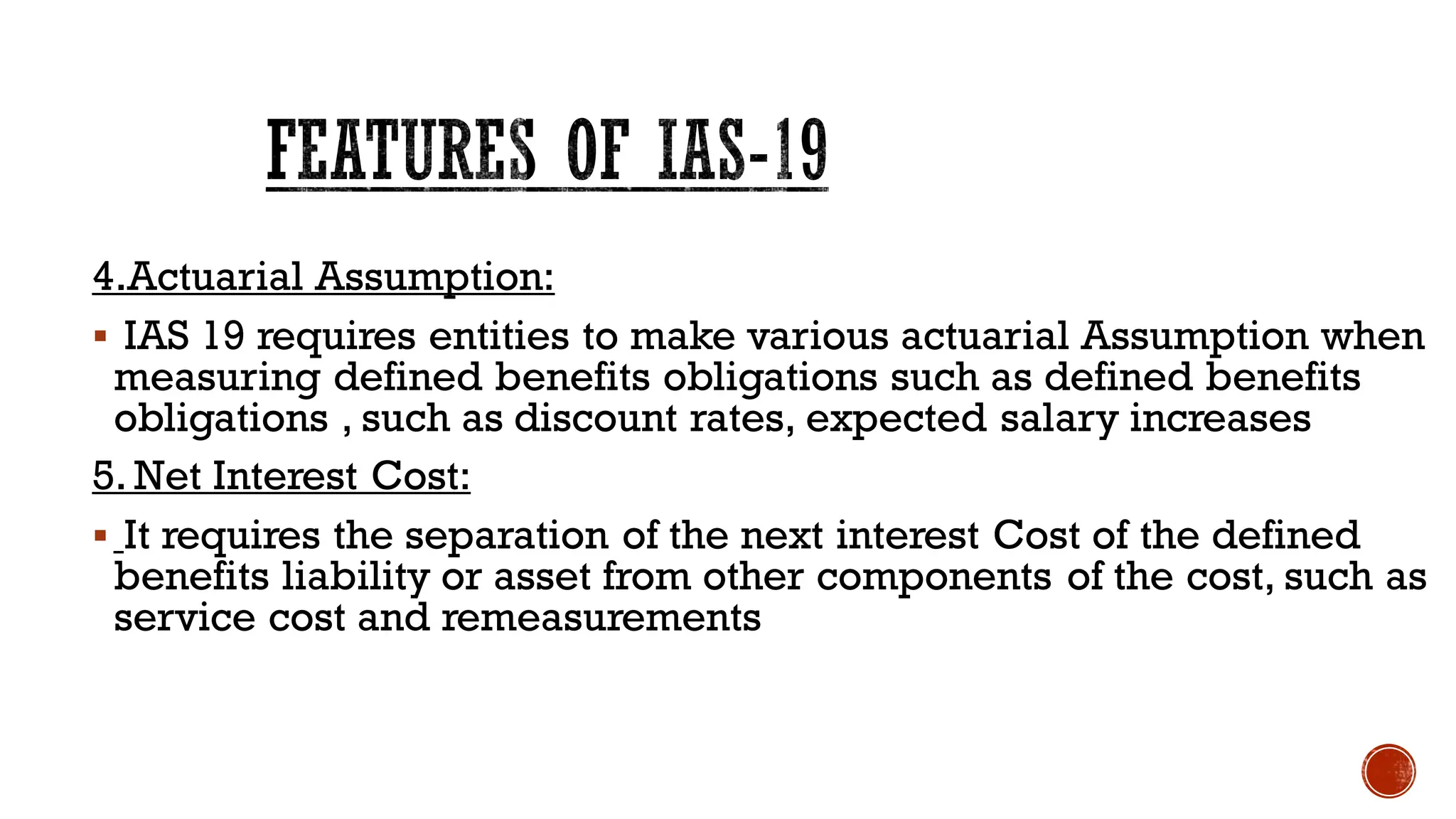

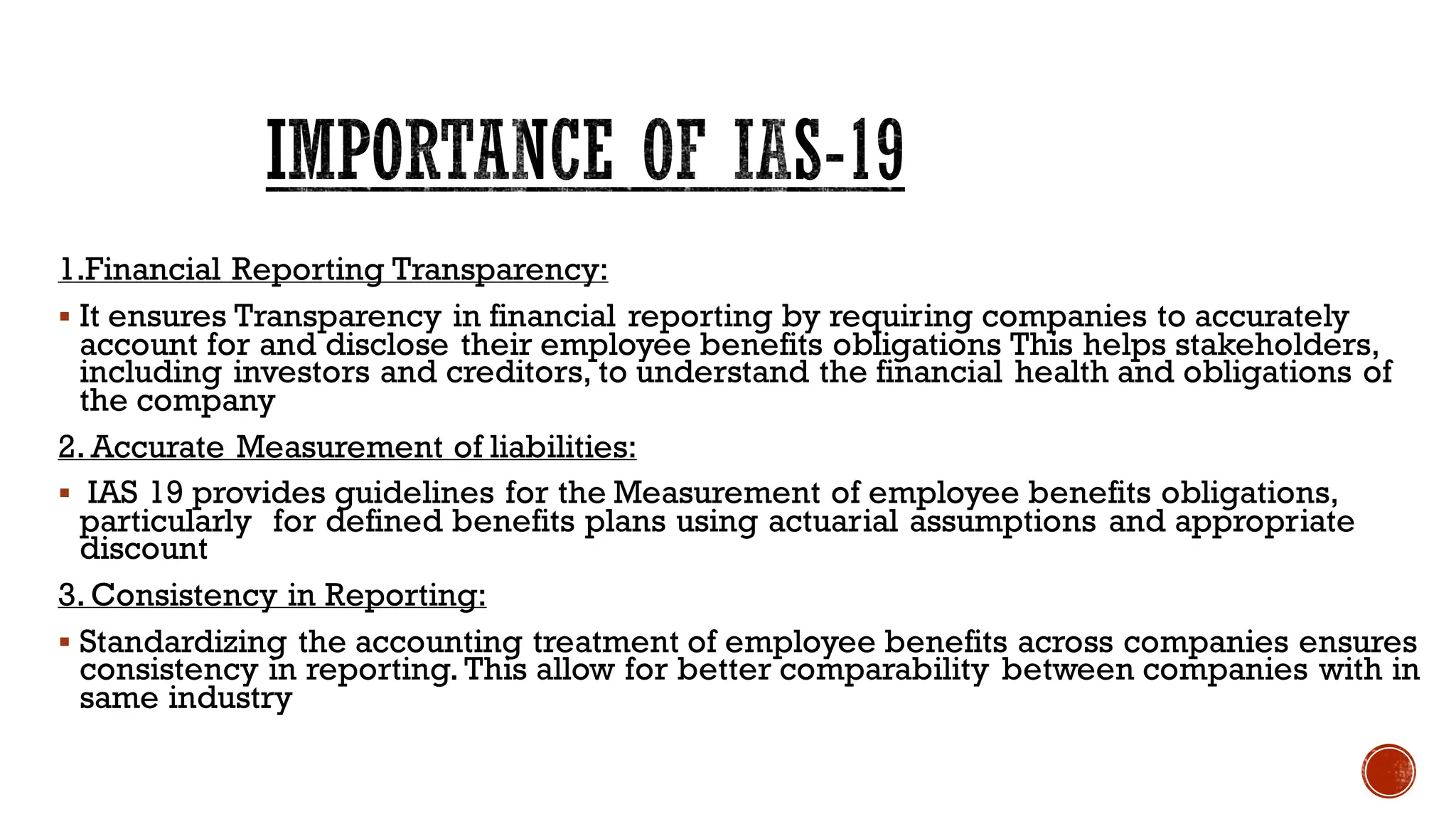

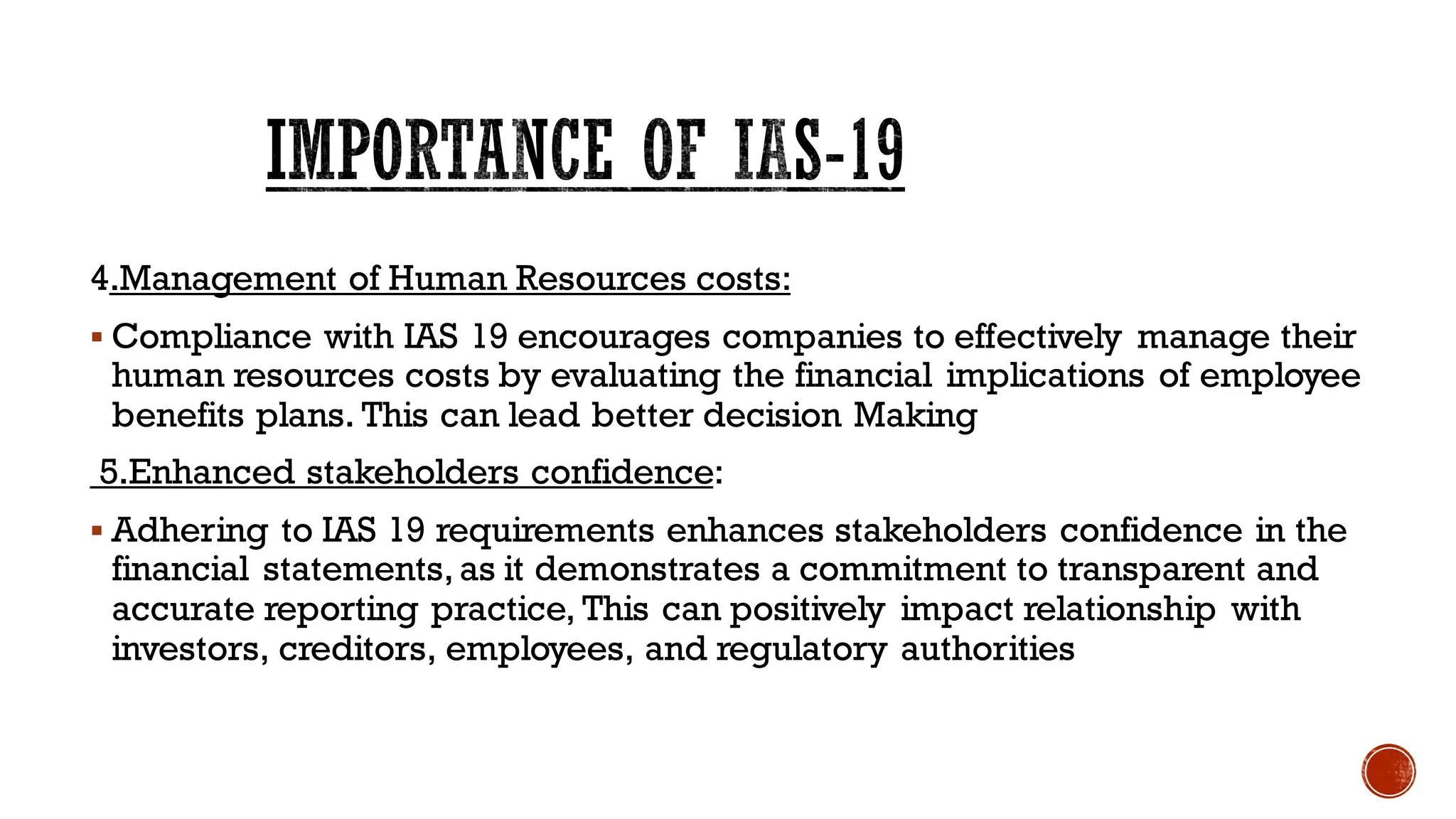

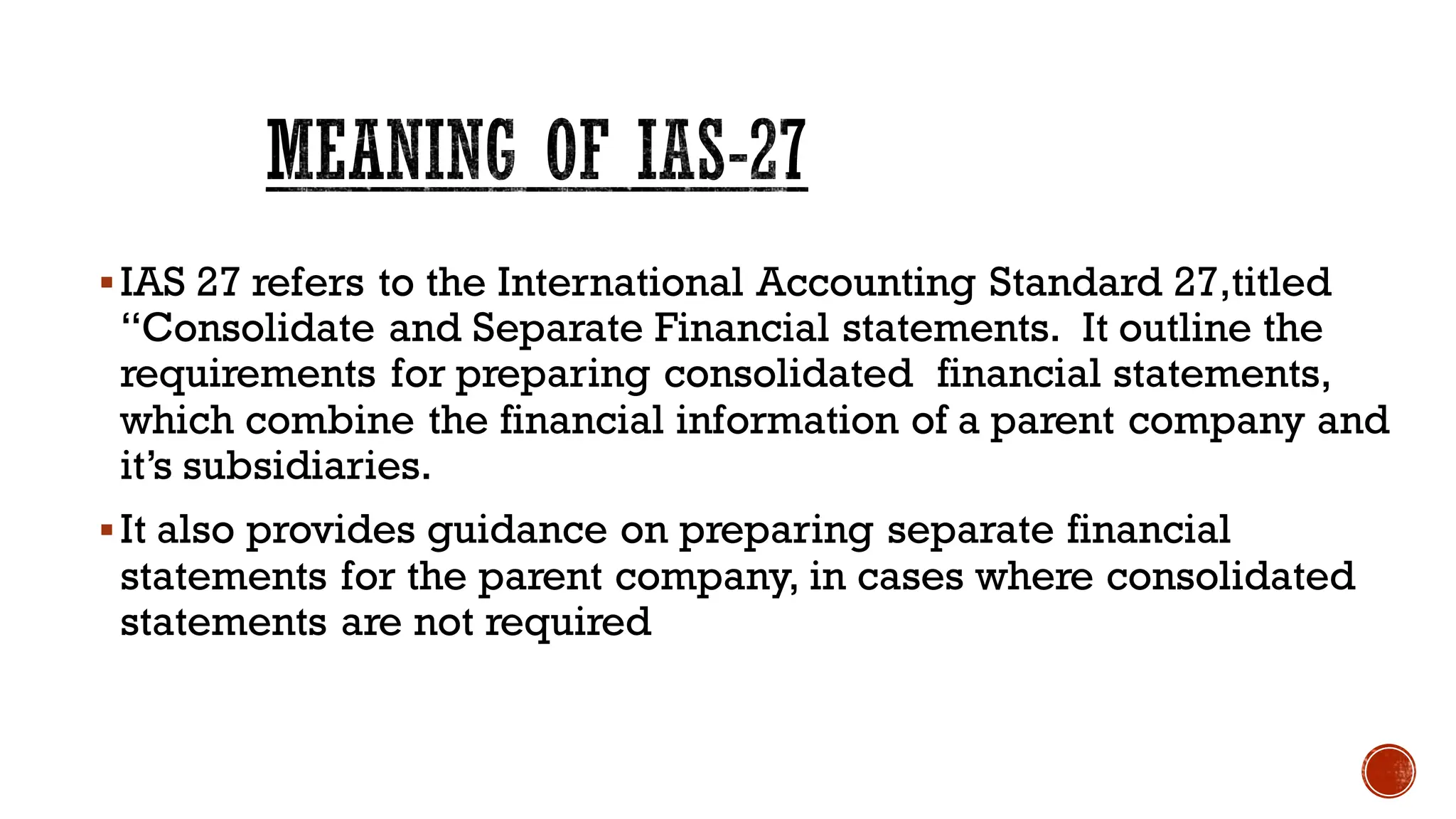

The document discusses several Indian Accounting Standards including IAS 19, IAS 27, and IAS 28. IAS 19 deals with accounting for employee benefits such as pensions and post-employment benefits. It aims to ensure accurate financial reporting and transparency regarding employee benefit obligations. IAS 27 provides requirements for consolidated financial statements that combine a parent and its subsidiaries, and guidance for separate parent financial statements. IAS 27 defines how to account for investments in subsidiaries, joint ventures, and associates. It outlines requirements for consolidated statements when an entity controls one or more others.

![FIMS[1] FINAL PRINT PPT647.docx](https://cdn.slidesharecdn.com/ss_thumbnails/fims1finalprintppt647-240213104513-12bc0623-thumbnail.jpg?width=640&height=640&fit=bounds)