Downloaded 138 times

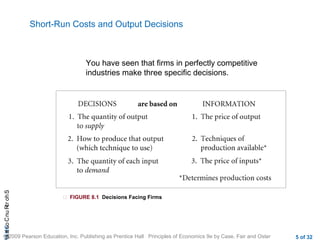

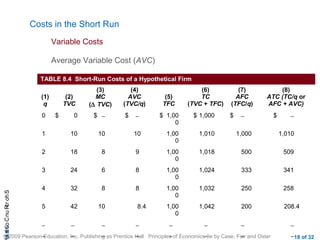

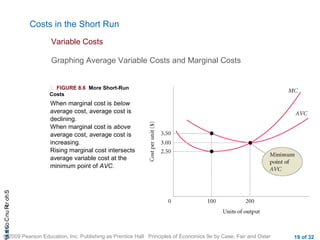

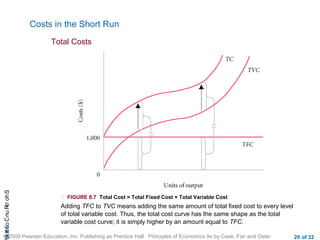

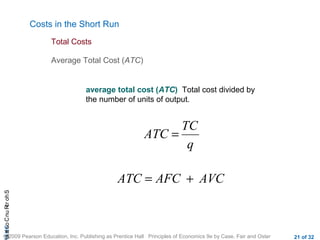

This document discusses short-run costs for firms. It defines key cost concepts like fixed costs, variable costs, total costs, average costs, and marginal costs. Fixed costs do not vary with output, while variable costs do. Total costs are the sum of fixed and variable costs. Marginal cost is the change in total cost from producing one additional unit. In the short-run, marginal costs typically rise as fixed capacities are approached. The document provides graphs and examples to illustrate how these different cost curves relate to each other.