Philippines upcoming rate hike and concerns

•

0 likes•43 views

This document summarizes the economic challenges facing the Philippines, including twin deficits, rising inflation, a weakening currency, and negative real interest rates. It notes the Philippines Central Bank is expected to raise interest rates by 50 basis points to 4% to address high inflation and the weak peso. With continued forecasts of a weakening peso and high inflation, along with higher interest rates, the document argues it is unrealistic to expect significant discounts on current interest rates for project financing in the Philippines.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Philippines upcoming rate hike and concerns

Similar to Philippines upcoming rate hike and concerns (20)

Recently uploaded

Recently uploaded (20)

Philippines upcoming rate hike and concerns

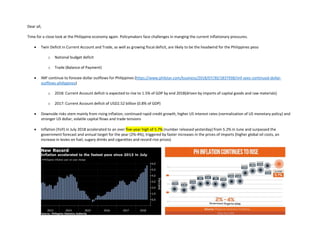

- 1. Dear all, Time for a close look at the Philippine economy again. Policymakers face challenges in manging the current inflationary pressures. Twin Deficit in Current Account and Trade, as well as growing fiscal deficit, are likely to be the headwind for the Philippines peso o National budget deficit o Trade (Balance of Payment) IMF continue to foresee dollar outflows for Philippines (https://www.philstar.com/business/2018/07/30/1837938/imf-sees-continued-dollar- outflows-philippines) o 2018: Current Account deficit is expected to rise to 1.5% of GDP by end 2018(driven by imports of capital goods and raw materials) o 2017: Current Account deficit of USD2.52 billion (0.8% of GDP) Downside risks stem mainly from rising inflation, continued rapid credit growth, higher US interest rates (normalization of US monetary policy) and stronger US dollar, volatile capital flows and trade tensions Inflation (YoY) in July 2018 accelerated to an over five-year high of 5.7% (number released yesterday) from 5.2% in June and surpassed the government forecast and annual target for the year (2%-4%), triggered by faster increases in the prices of imports (higher global oil costs, an increase in levies on fuel, sugary drinks and cigarettes and record rice prices)

- 2. Peso has slumped to its weakest level in 12 years this year, +Php53.6 / USD but recover to just below <Php53 in recent days before the upcoming interest rate decision (9th August), generally, Philippines central bank is expected to adopt the biggest rate hike in a Decade (50 bps hike to 4%) since 2008, supported by strong economic growth forecast at more than 6% in 2Q2018, high inflation rate and weakening currency. Below chart is the current number (3.5%) This rate hike approach is similar to other central banks in emerging markets as countries take more aggressive steps to curb the fallout from rising US rate and stronger dollar. Please pay this particular attention on the headline here “Philippines is the only Southeast Asian economy to have negative real interests at - 2.2%” calculated using the Benchmark interest rate minus inflation. The key challenge here is the decreasing purchase power of the currency. The purpose of this article is to keep you update with the latest economic development and challenges ahead on the “Interest Rate” assumptions at the project level. With the continued forecast of “Weakening Philippine Peso and high inflation”, and Central bank policy to adopt counter measures to address the challenges with higher interest rate. It will be unrealistic to expect any significant discount of the present interest rate at the project level.

- 3. Here is the snapshot of the present government 10Y treasury bond yield. At the present rate of 6.5%, it may goes up further following the 50bps rate hike expected by tomorrow by the Philippines Central Banks, settle in the region of 7%. It will be unrealise to assume that we can secure any “cheaper” interest rate to support the project financing, unless the financing party has no concern on the “weakening Peso” and “High inflation rate” The challenge is really huge for Philippines project financing market. Best Regards, Jonathan Sim