Downloaded 96 times

![Introduction To develop an automated framework for trading strategy design, by employing evolutionary computation in conjunction with other machine learning paradigms The present framework utilize genetic programming Much of the existing financial forecasting using GP has focused on high-frequency FX [Jonsson, 1997][Dempster and Jones, 2001][Bhattacharyya et al, 2002] and the general consencus is that there is predictability, and excess return is achievable in the pressence of transaction costs For stocks, the results are mixed [Allen and Karjalainen, 1999] do not significantly out-perform the buy-and-hold on S&P500 daily data, but [Becker and Sheshadri, 2003] do on monthly.](https://image.slidesharecdn.com/philip-genetic-programming-in-statistical-arbitrage-119921488571598-4/85/Philip-Genetic-Programming-In-Statistical-Arbitrage-3-320.jpg)

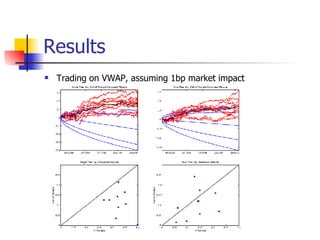

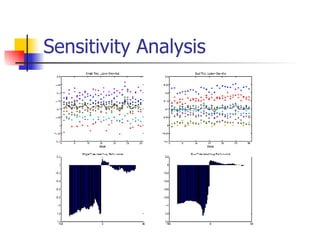

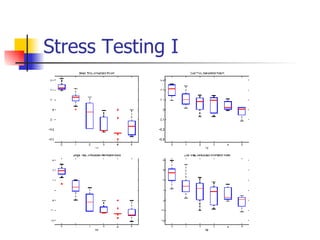

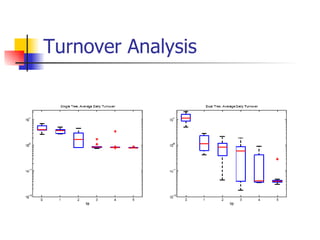

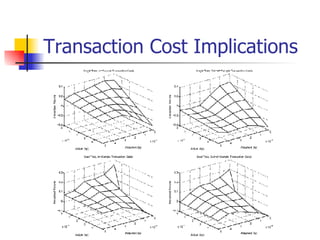

This document discusses using genetic programming to develop automated trading strategies by evolving buy and sell rules for stocks. It introduces genetic programming and how it has been applied to financial forecasting problems. The framework uses genetic programming to evolve trading rules based on hourly price and volume data for banking stocks. The results show it is possible to discover profitable arbitrage trading strategies in this domain, and that co-evolving separate buy and sell rules outperforms evolving a single ruleset. Transaction costs are also an important factor to consider for optimal performance.

![Getting Started with Apache Spark: Big Data Made Simple [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/apachesparkgettingstarted-260203175547-8361bcc3-thumbnail.jpg?width=640&height=640&fit=bounds)