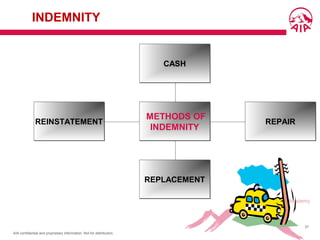

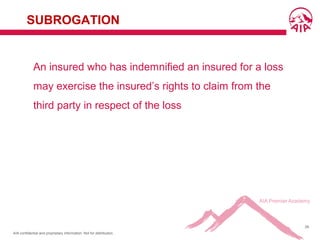

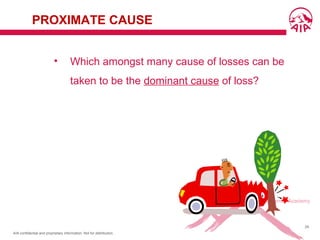

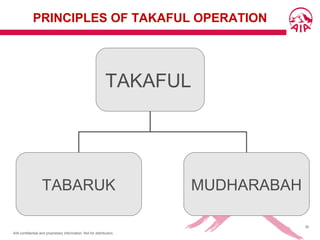

Downloaded 81 times

![AIA confidential and proprietary information. Not for distribution.

61

THE INSURANCE ACT, 1996 [SECTION 151]

“A person who is authorized by an insurer to be its

insurance agent and who solicits or negotiates a

contract of insurance in that capacity shall be deemed,

for the purpose of the formation of the contract, to be

the agent of the insurer and the knowledge of that

insurance agent shall be deemed to be the knowledge

of the insurer”

Law of Agency p.p 7/6](https://image.slidesharecdn.com/n8m94paqlof458iixtix-signature-4af5e7572403e3b1d242a0cf329bb8642956ce20252e5368a4f212b1be9de295-poli-151102112108-lva1-app6891/85/Pce-part-a-chapter-1-8-61-320.jpg)

![AIA confidential and proprietary information. Not for distribution.

62

THE INSURANCE ACT, 1996 [SECTION 151]

shall not apply…..

Where there is collusion or connivance between

the insurance agent and the proposer in the

formation of the contract of insurance](https://image.slidesharecdn.com/n8m94paqlof458iixtix-signature-4af5e7572403e3b1d242a0cf329bb8642956ce20252e5368a4f212b1be9de295-poli-151102112108-lva1-app6891/85/Pce-part-a-chapter-1-8-62-320.jpg)

![AIA confidential and proprietary information. Not for distribution.

63

THE INSURANCE ACT, 1996 [SECTION 151]

shall not apply…..cont’

Where a person has ceased to be an insurance

agent of a insurer and it has taken reasonable steps

to inform, or bring to the knowledge of, potential

policy owners and the public in general of the fact of

such cessation](https://image.slidesharecdn.com/n8m94paqlof458iixtix-signature-4af5e7572403e3b1d242a0cf329bb8642956ce20252e5368a4f212b1be9de295-poli-151102112108-lva1-app6891/85/Pce-part-a-chapter-1-8-63-320.jpg)

![AIA confidential and proprietary information. Not for distribution.

64

THE INSURANCE ACT, 1996 [ SECTION 150 (4) ]

No licensed insurer or insurance agent, in order to

induce a person to enter into or offer to enter into a

contract of insurance with it or through him…

shall make a statement, which is misleading, false

or deceptive, whether fraudulently or otherwise](https://image.slidesharecdn.com/n8m94paqlof458iixtix-signature-4af5e7572403e3b1d242a0cf329bb8642956ce20252e5368a4f212b1be9de295-poli-151102112108-lva1-app6891/85/Pce-part-a-chapter-1-8-64-320.jpg)

![AIA confidential and proprietary information. Not for distribution.

65

THE INSURANCE ACT, 1996 [ SECTION 150 (4) ]

shall fraudulently conceal a material fact; or

in the case of an insurance agent,, use sales

brochures or sales illustration not authorized by the

licensed insurer

PENALTY: ONE MILLION RINGGIT](https://image.slidesharecdn.com/n8m94paqlof458iixtix-signature-4af5e7572403e3b1d242a0cf329bb8642956ce20252e5368a4f212b1be9de295-poli-151102112108-lva1-app6891/85/Pce-part-a-chapter-1-8-65-320.jpg)

The document provides an introduction to insurance concepts, including the basic principles of insurance, risk management, the insurance market and regulatory framework. It discusses key insurance concepts such as insurable interest, utmost good faith, indemnity, subrogation and proximate cause. It also introduces the role of agents and intermediaries and the importance of marketing and after-sales services in the insurance industry.