1. Developers

Tools Outsource Agencies

Independent Development Studios

• Monkey Bar Games

• Digital Chocolate

• Team 17

• Foundation 9

• Valve

• CCP

• Bungie

• Rebellion

• Cat Daddy

• Jagex

• A2M

• Eurocom

• Relentless UK

• Kuju

• Media Molecule

• University of Hull

• City of London

• University of Surrey

• Southampton Solent

University

• Bedfordshire University

• University of Northampton

• University of Dundee

• Train2Game

Localisation Sound Art

• Binari Sonari

• Lionbridge Technology

• Blondé

• Welocalize

• Comsense

• Freedman International

• Texel Localization

• Palex

Game Engines

• Unreal Engine 3

• Game bryo lightspeed

• Cry engine 3

• Unity 3D

• Blitz Tech

• Infernal Engine

• Vision Engine 7.5

• Bigworld

Development Tools

• Rad Game Tools

• Gametools Project

• Autodesk 3ds Max

• OpenGL

• Direct 3D

• NVIDIA Tools

• Direct X

• Flash CS4

• Basiscape

• Tonehammer

• Four Bars Intertainment

• 615 Music

• Advent Media Production

• Greatwaves Digital Media

• Omni Interactive Audio

• Ware Generation

• Shadows in Darkness

• Altmore Springs

• Pixel Revolution

• Aerohills

• Red Fly Studio

• Virtuos

• Blackbow

• Aaron Studios

Trade Bodies

& Regulations

Industry News

& Analysis

University

& TrainingDepartment of Culture,

Media and Sports

Pan European Games

Information

The Independent

Games Developers

Association

• MCV

• 3D World

• casualgaming.biz

• mobile-ent.biz

• Gamesblog

• gamesindustry.biz

• Game Hub

• Mediabox

• Develop Magazine

• Indie Magazine

IAGR

International

Association of

Gaming Regulators

Mobile Specialist Developers

• Firemint

• Gameloft

• Digital Chocolate

• ChaYoWo Games

• Cryteck UK

• Data Design Interactive

• Xaitment GMBH

• Polyphony Digital

• Legend Mobile

• Oasys Mobile Inc

• Gamelion

• Mr. Goodliving

• Fishlabs

• Dynamic Pixels

The map includes information compiled from various reputable sources and other

methods like structured interviews and surveys, conference material and

information available in the public domain. As data and information sources are

outside our control, New Media Maze and make no representation as to its

accuracy or completeness.All responsibility for any interpretation or actions based

on this map lies solely with the reader. Copyright 2009

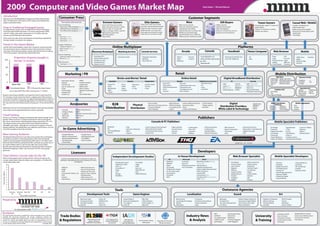

Introduction

Drop in Traditional Packaged Games

Welcome to the NewMediaMaze Computer and Video Games Market

Map. The Map shows the structure of the industry and identifies key

players and market trends.

As expected year-on-year sales of traditional new boxed retail games

for the first half of 2009 were down 5.7% on the same period in 2008

with 29.7 million units sold in comparison to 31.5 million units the

previous year (ELSPA) due to the recession.

At the same time sales of pre-owned games are growing as reported by

all major retailers investing in the category.

Disclaimer

Entertainment and

Leisure Software

Publishers Association

In House Development

• Lionhead

• Rare Ltd

• Wingnut Interactive

• Turn 10 Studios

• Rebellion

• BioWare

• Maxis

• EA Canada

• EA Black Box Canada

• EA The Sims Studio

• EA Pandemic

• EA Mythic

• DICE

• Black Rock Studios (Disney

Interactive)

• Bandai Namco

• Ubisoft Entertainment

• Kojima Digital Entertainment

• Eidos Interactive

• Square ENIX

• GamesFreak (IGN)

• Travellers Tale (Warner Bros.)

• Relic (THQ)

EA Microsoft Other

•

Trends in the Games Market

Source MCV UK 22/4/09

0

1

2

3

4

5

6

7

8

9

10

Nintendo

DS

Nintendo

Wii

Xbox 360 PSP PS3 PS2

Total Lifetime Console Sales for the UK

ConsoleSales,Millions

Platforms

Extreme Gamers

Customer Segments

MassElite Gamers Gift Buyers Casual Web / Mobile

Accessories

Publishers

Online Multiplayer

Console

• Sony Playstation 3/2

• Microsoft Xbox 360-Arcade,

pro, elite

• Nintendo Wii

Handheld

• Nintendo DS (DSi/DS Lite)

• Sony PSP (3000/Go!)

Home Computer

• PC

• Mac

• Owns more than one console

• Plays more than 10 hours a week

• Skew to male 12-35 year olds

• Buys on average 4 titles a quarter

• Will purchase preowned

• Will pirate games

• Plays online

• Owns more than one console

• Consoles may be family purchase

• Plays less than 10 hours a week

• Balanced split 12-45 year olds

• New games purchased through

high street or received as a gift

• Plays on one console

• Play is for education, fitness,

socialising or time filling

• High female skew 5-65 years old

• Wholly purchased through

general retailer, Tesco, ASDA etc.

• Influenced by mainstream media

• Highly seasonal

• Uninformed purchase

• Older demographic

• Shops for convenience, price or

recipient recommendations

• Usually a handheld unit

• High female skew

• Balanced age demographic

• Attracted to simple games with

simple rules

• Time filling

Arcade

• Namco

• SEGA

• Midaway

• Konami

• Capcom

Tween Gamers

• Primarily girls, aged 9-13 years old

• Make friends

• Play for 55 minutes at a sitting

• Explore new places

Consumer Press

Future Publishing

• PlayStation Official Magazine (print)

• Official Nintendo Magazine (print)

• The Official Xbox Magazine (print)

IGN

• IGN.com (online)

• GameSpy (online)

• Gamasutra (online)

Imagine Publishing

• Pokemon World (print)

• Retro Gamer (print)

• Play (print)

Dennis Publishing

• Ultimate Guide to PC Gaming (print)

• Bit-Tech (print)

CBS Interactive

• Gamespot (online)

• Pebble Entertainment

• Belkin

• Pinpoint Consumer Electronics

• Plantronics

• Logic 3

Web Browser

• Pogo

• Sega

• PopCap Games

• Habbo

• Club Penguin

• Jolt

• Funcom

• Jagex

• 888.com

• Gamesys

Matching Services

• GameSpy Arcade

Console Services

• Playstation Networks

• Wii Ware

• Xbox 360 Live

Massively Multiplayer

• EverQuest (PC)

• World of Warcraft (PC)

• Warhammer (PC)

• Guildwards (PC)

• Quake Live (PC)

Press split by online and print

B2B

Distribution

• Gem creative

• Meroncourt Europe Services

• Pinnacle Software

• Discs Tribution

• Ideal Software

• DVD Technology

• Curveball Leisure

• Logic 3

• Gamers Without Frontiers

• Interactive Ideas

• Play V

• Creative Distribution

Digital

Distribution Providers,

White Label & Technology

• Digital River

• Metaboli

• Steam

• Exent

• Scratch Busters

• Trilogy Logistics

• EtnaTech

Specialist D2C

Operator PortalsApp Store

Mobile

• J2ME (Java)

• Apple

• Nokia N-Gage

• Android

• Symbian

• Jamba

• Mobile Fun

• Neomobile

• Hungama

• PlayPhone

• Flycell

• TIM w.c.

Publisher D2C

• EA Mobile

• Glu

• Capcom Mobile

• Vodafone

• T-Mobile

• Orange

• Apple App store

• Blackberry App World

• Android Market

• Windows Apps

• Handango

• Palm Apps

• Mobango

• Get Jar

Physical

Distribution

Mobile Specialist PublishersMobile Specialist Publishers

• EA Mobile

• Gameloft

• Digital Chocolate

• Glu Mobile

• Greystripe

• Oasys Mobile Inc.

• Hands-On Mobile

• HandyGames

• I-Play

• IG Fun

• THQ Wireless

• Player X

• Twistbox Games

• Vivendi Games Mobile

• Connect 2 Media

• Ngmoco

• Namco

• Mobile Deluxe

Retail

‘Bricks-and-Mortar’Retail Online Retail

Specialist General Independent

Digital Broadband Distribution

• Game PLC

• DSGi

• Blockbuster

• HMV

• Comet

• Tesco

• ASDA

• Argos

• ToysRus

• Grainer Games

• The Hut

• Chips

• Game PLC

• Tesco Direct

• ASDA Entertainment

• Zavvi

• Amazon

Publishers to Consumer PC Console

• Microsoft Shop

• EA

• Sony

• Activision

• Ubisoft

• Steam (PC)

• Metaboli

• Onlive

• HMV (XBox 360)

• Play.com (all formats)

• Xbox Live

• Nintendo Wii Ware

• PlayStation Networks

Retailer

Mobile Distribution

Mobile Aggregators

• Zed

• Arvato

• Seletra

Mobile Distribution

Platforms

• Movaya

• Motricity

• Amdocs

• Materna

• Metaflow

• Accumulate• Pyramat

• Antigrav Media

• Logitech

• Microsoft

• Ideazon

In-Game Advertising

• Google AdSense

• Massive Incorporated

• Nielsen Media Research

• IGA Worldwide

• JOGO Media

• 3

• O2

• Double Fusion

• NeoEdge Networks

• EnterMedia

• Game Creative

• Play.com

• Gameconnection.co.uk

• Gameseek.co.uk

• Simplygames.com

• Gem creative

• Morrisons

• Next

• Co-Op

• HMV

• Game (PC)

• EA (Mac/PC)

• Online Playcast

Marketing / PR

• Barrington Harvey

• Bastion

• Ark VFX Ltd

• Eye-D Creative Ltd

• Fluid

• Fink Creative

• Realtime UK

• Studio Co2

• FEREF

• Freeform.london

• Indigo Pearl

• Media Safari

• More Creative

• Rainbow Productions

• 3Di

• New Media Maze

EA Microsoft Other

Web Browser Specialist

• Gameforge

• Travian Games

• Sierra Online

• Bigpoint

• Weewar

• Imperia Online

• Mediatainment

• Burda:ic

• Sodigital

• BigFish

• Xybris Interactive

• Travian Games

• Pixeltamer

• Twisted Empire

• XS Software

• Upjers

• Crafty Studios

• Xhodon

• Xfer

• Popcap

Licensors

• WWE Inc

• MGM

• EON

• Formula One Admin. Ltd.

• FIFA

• Hasbro

• Warner Bros.

• MGA Entertainment

• Viacom international

• Paramount Pics Corp

• Disney / Pixar / Marvel

Entertainment

• 20th Century Fox

• IGN Entertainment Inc.

Licensors grant permission to licensees to copy and

distribute copyrighted works and characters for use in

videogames.

Console & PC Publishers

• Nintendo

• EA

• Activision|Blizzard

• Ubisoft

• THQ

• Take-Two interactive

• SEGA

• Capcom

• Namco Bandai

• Vivendi Games

• Konami

• NCsoft

• Sony Computer Entertainment

• Microsoft Games Studio

• SCi Entertainment Group

• Square Enix

• Disney Interactive

• Codemasters

• ZeniMax Media

• Kojima Production

• Codemasters

• Altus USA

• LucasArts

• Midway

• NBC Universal

• Nexon Corporation

• 505 Games

• Atari

• Paramount Pictures

• Warner Bros. Entertainment

• Digital Chocolate

• IGN

Growth of the downloadable content (DLC) for games consoles has been

slow but there has been a marked increase in last two months amongst

consumers of the latest generation consoles. Blu-Ray PS3 owners make up

17% of the numbers, 16% with Xbox 360 and Wii at 6%.

Xbox 360 PS3 Wii

% Physical Disc Based Games% Downloaded Games

Proportion of games bought in

the last 12 months

Source Ipsos MORI (Base 468 console gamers 12-18 May)

0

40

80

120

Research done by Ipsos MediaCT concludes that there is high interest for

DLC amongst console owners but there is a tipping point where pricing is

concerned. Perception of the value of a digital downloaded game is that it is

not worth as much as a retailed packaged game. The interest in purchasing

DLC was only 3% at the £36 price point, increasing to 11% at £24 and 39% at

£12.

Additional revenues are increasingly generated by online gaming with both

“pay to play”and ad supported business models in operation.

OnLive is a US startup is hoping to revolutionise the market through“cloud

gaming”where consumers can play mainstream PC and console games

that run on central servers with the graphics being streamed to a PC or TV.

This will give instant access without the need to download, all for an

affordable subscription. Although the concept has the support of several

leading publishers, New Media Maze sees significant performance, cost and

consumer acceptance risks to be overcome.

The Nintendo Wii and DS and music titles such as Guitar Hero and Singstar

are leading a revolution in opening gaming to older and more female

audiences and participative family gaming. With sales of 1.65 million units

Nintendo’s Wii Fit, Wii Play and Mario Kart Wii combined accounted 72% of

the top five OEbest sellers’in the UK chart (GfK chart track for 2008 ).

Records were also broken by Nintendo’s Dr Kawashima’s Brain Training on

Ninetndo DS topping 3 million units to become the UK’s most popular

game ever.

With its broad appeal and innovative interface Wii has emerged as the

console market leader selling 50 million units worldwide vs 21million PS3

and 30 million Xbox sales.

Mass Gaming Audience

Cloud Gaming

• Ovi

2009 Computer and Video Games Market Map

Prepared by

+44 (0)207 097 3600

www.newmediamaze.com

In association with FirstPartner

Kate Hakes I Richard Warren