Download to read offline

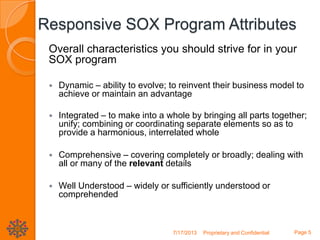

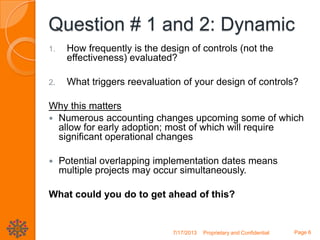

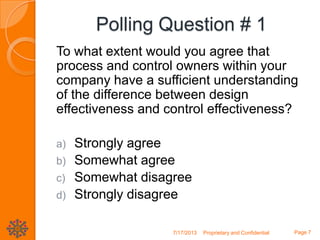

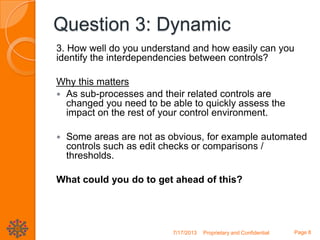

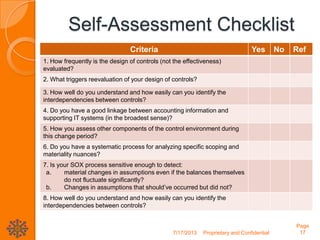

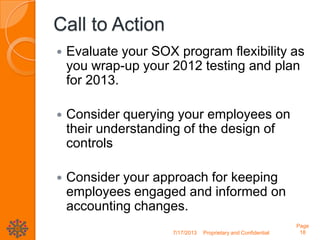

The document discusses the attributes of a responsive SOX (Sarbanes-Oxley) program, highlighting the need for a dynamic, integrated, comprehensive, and well-understood framework. It includes polling questions and a self-assessment tool to evaluate the effectiveness of current SOX programs, particularly in light of upcoming accounting changes. The call to action emphasizes the importance of program flexibility, employee understanding, and engagement regarding accounting standards.