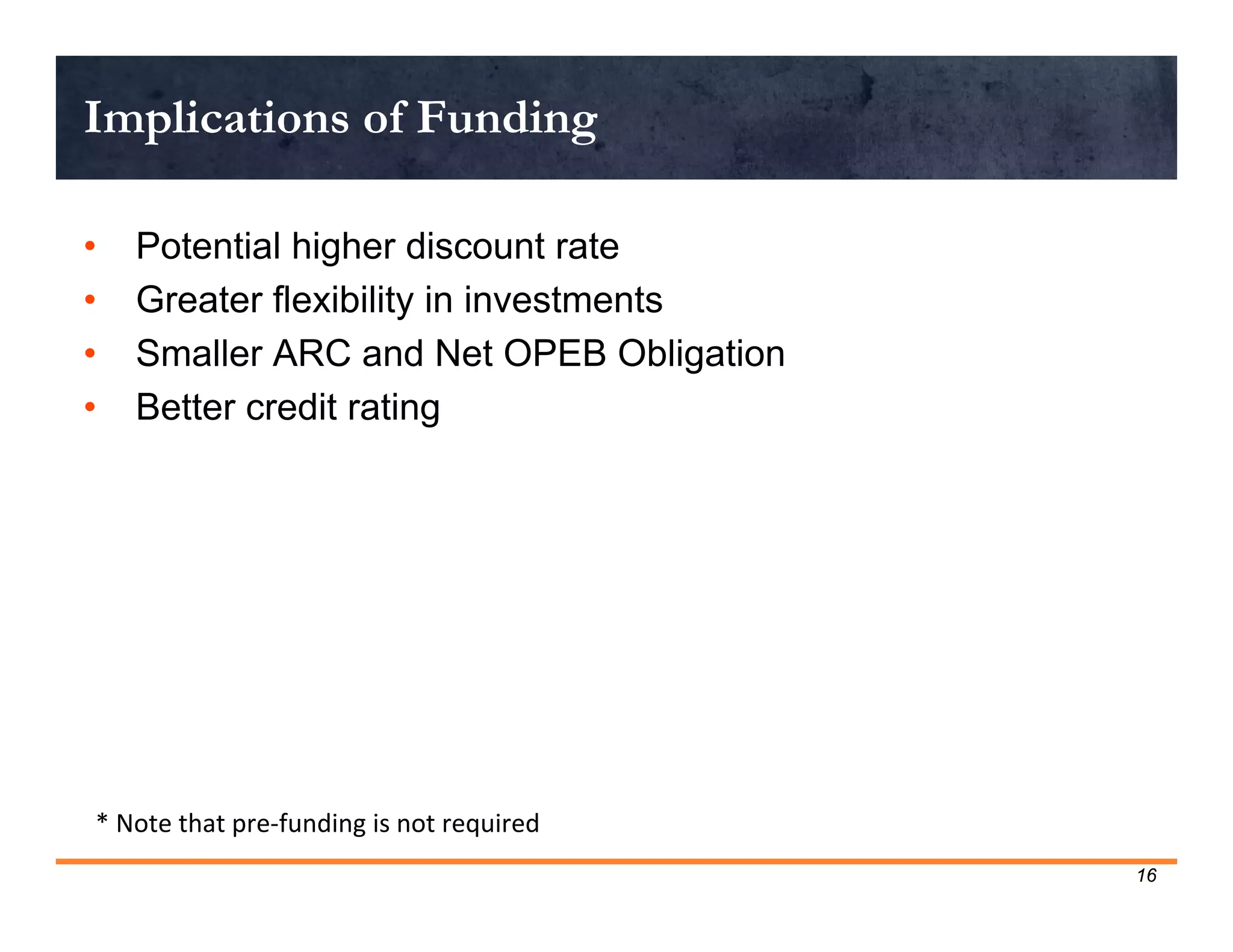

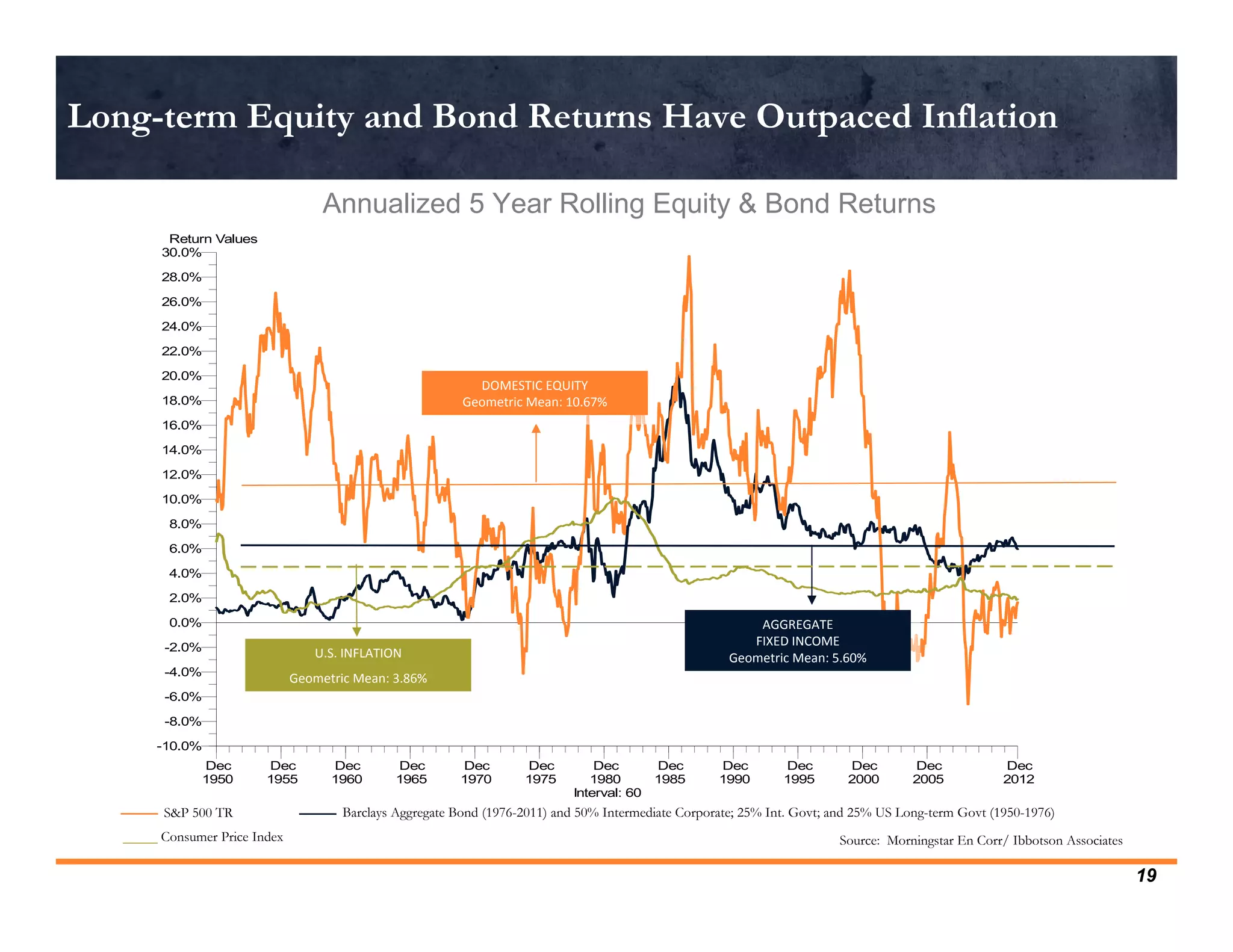

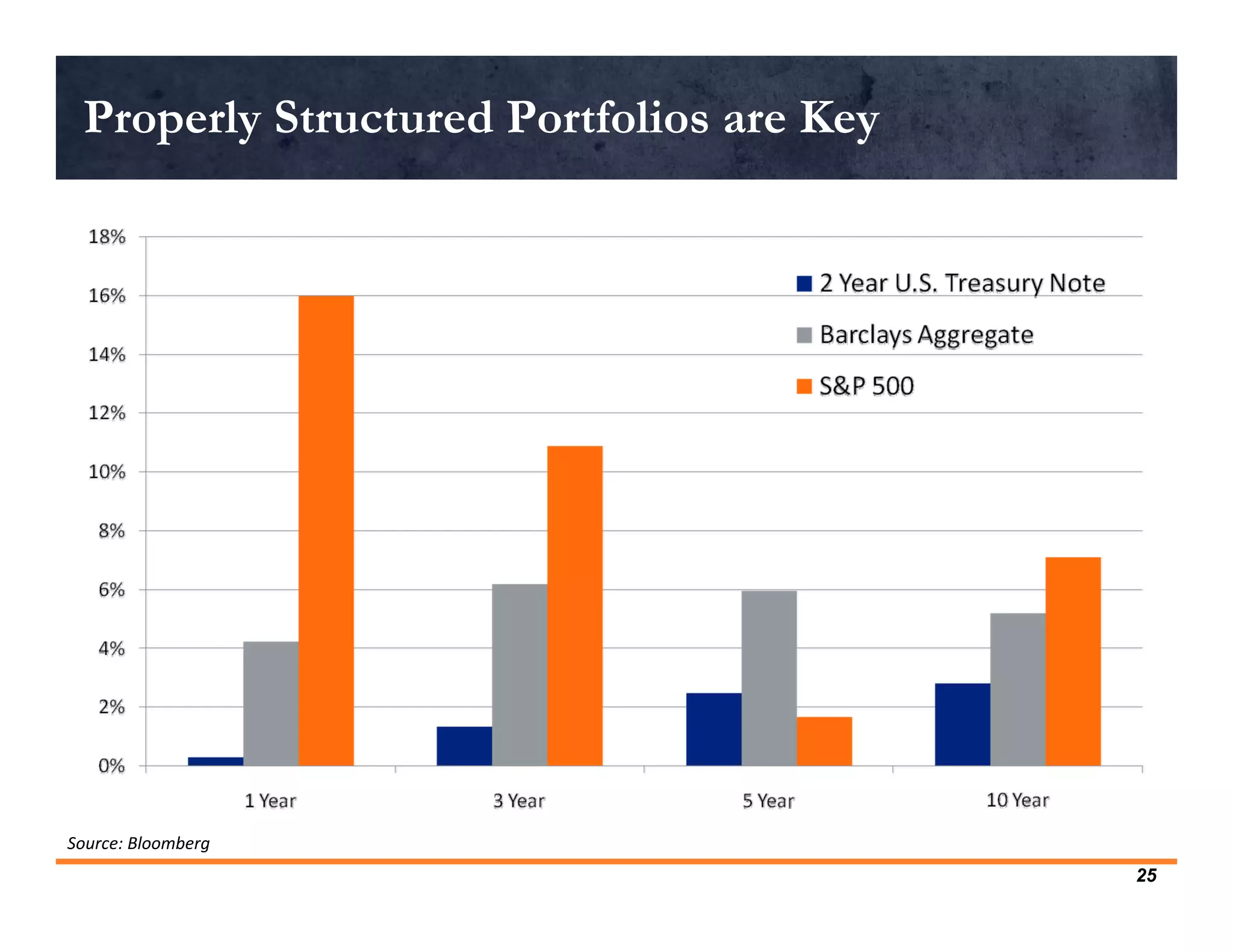

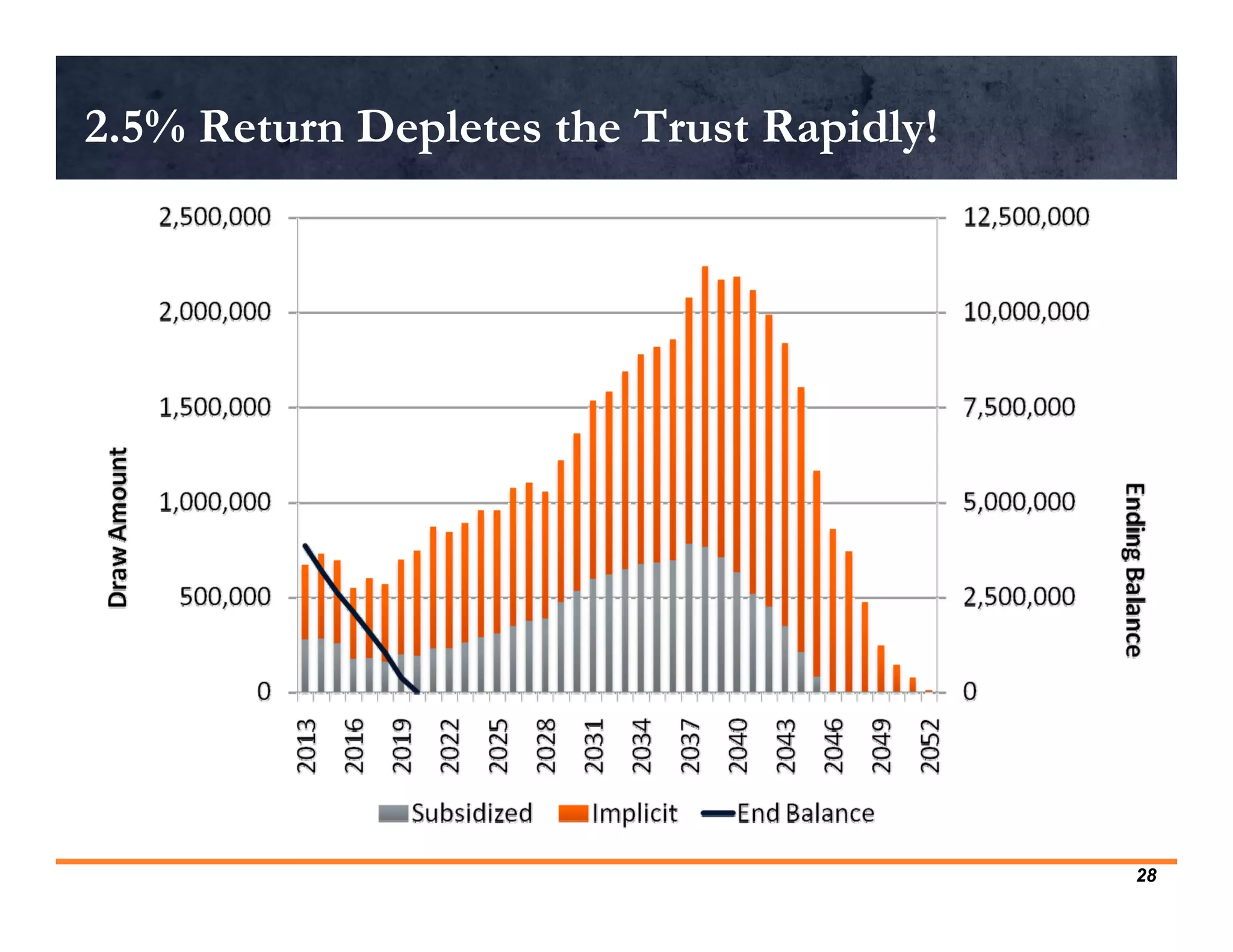

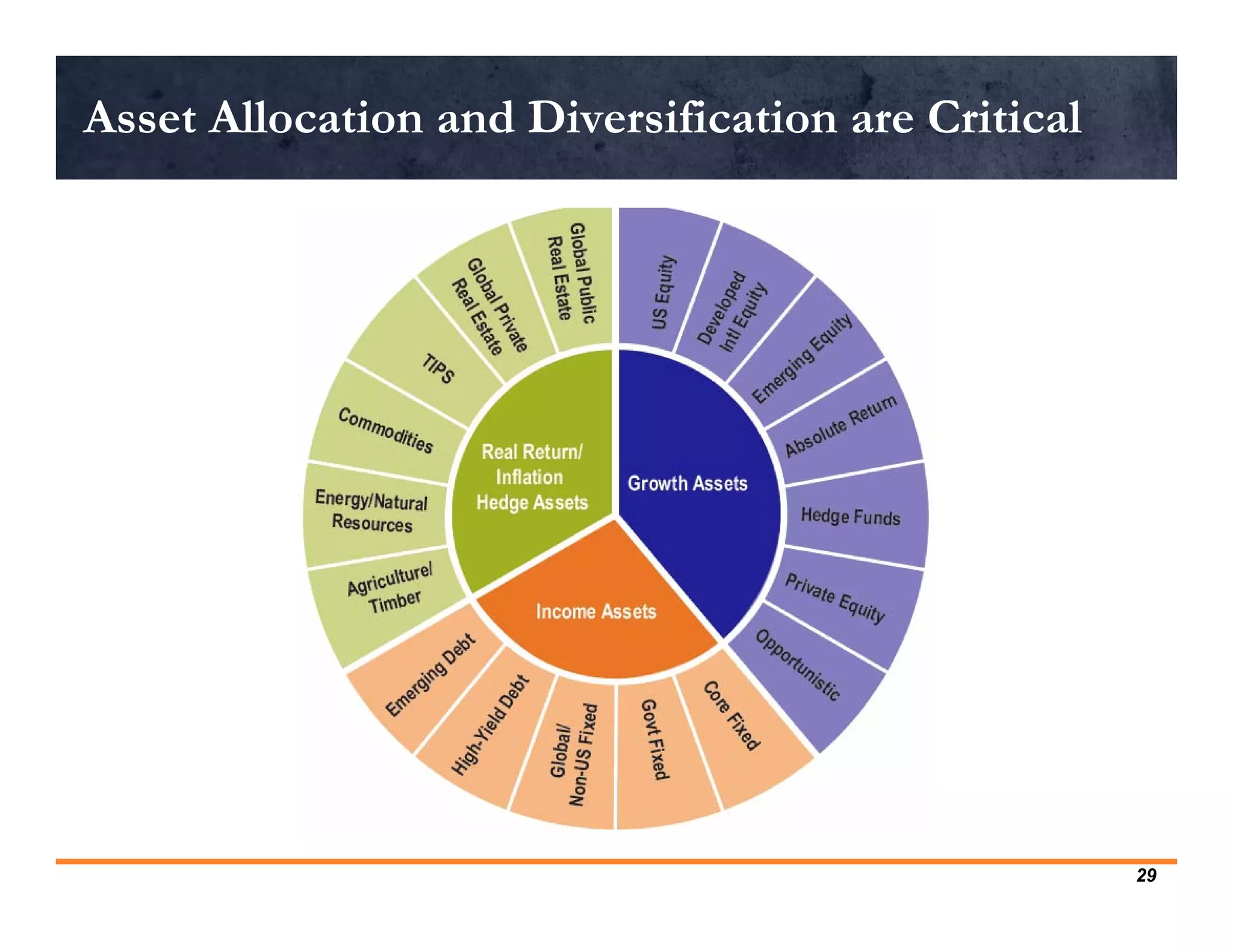

The document discusses investing Other Post-Employment Benefit (OPEB) funds and the implications for school boards. It notes that playing it too safe with OPEB investments, such as keeping funds in low-return savings accounts, poses dangers as the funds may deplete before obligations are met. Diversifying investments and allowing access to higher-returning asset classes like equities can help funds last longer. School boards have a fiduciary duty to ensure investment policies and expertise are in place to prudently manage OPEB investments for the long run. Actuarial analyses are an important starting point but assumptions will change over time.