Download as PDF, PPTX

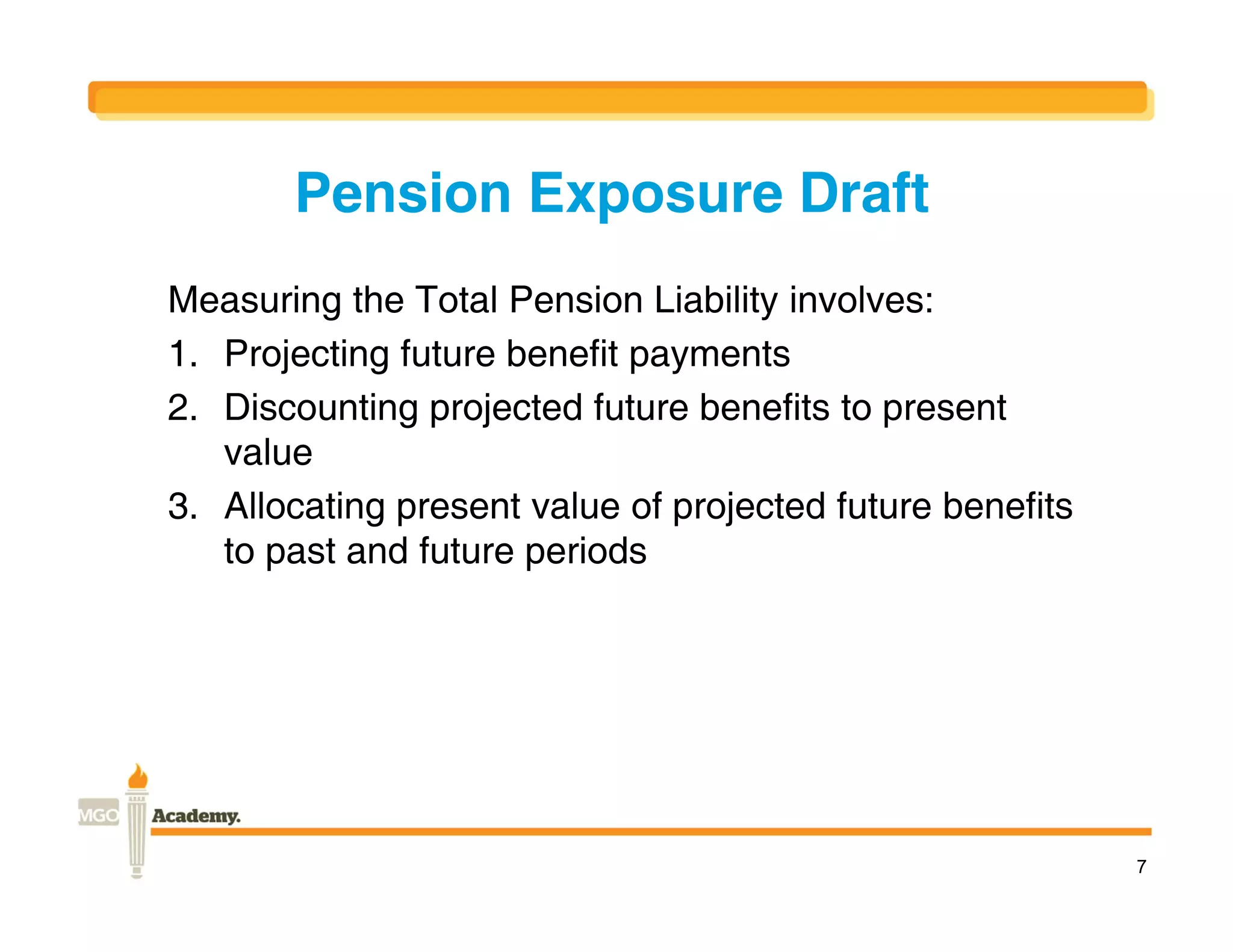

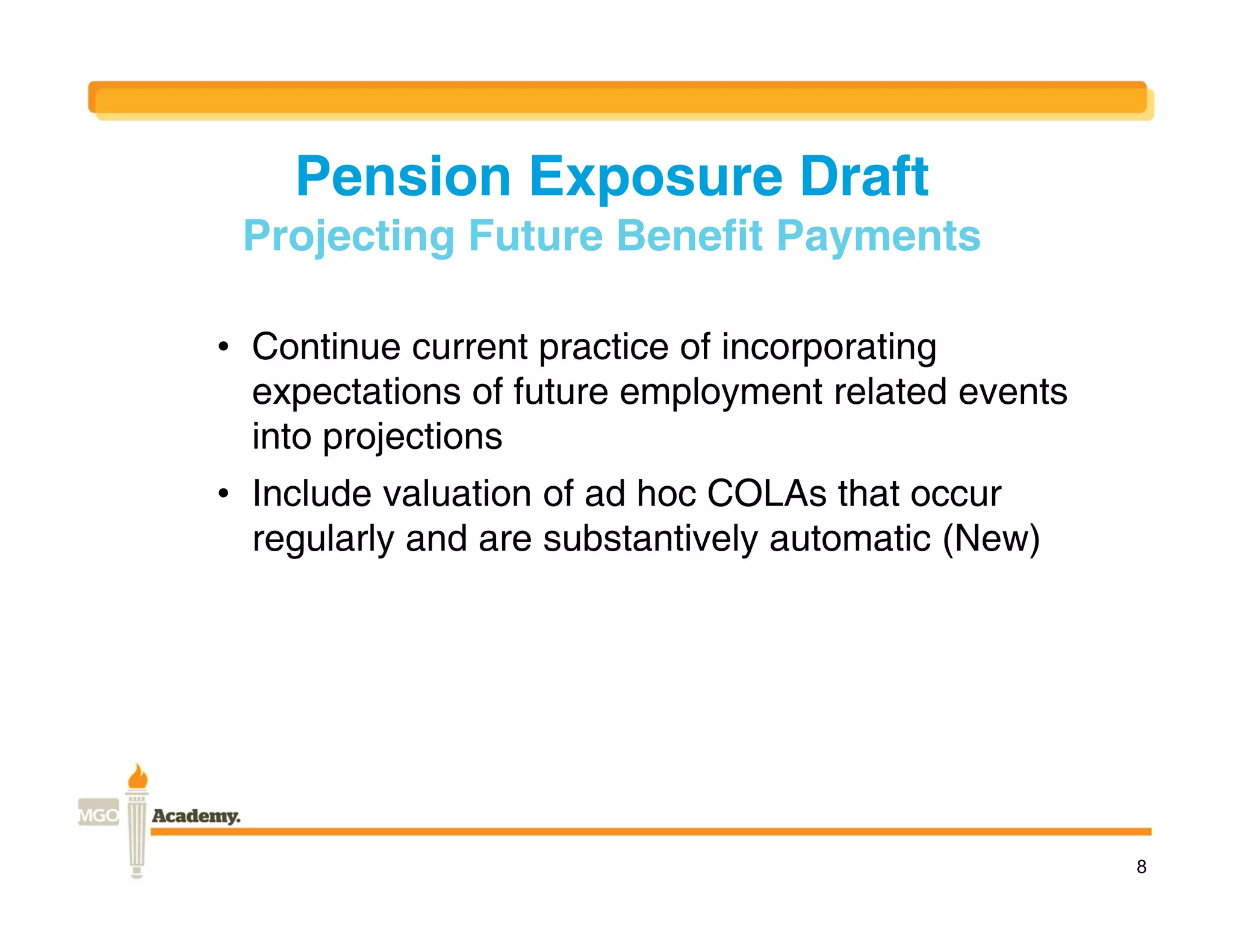

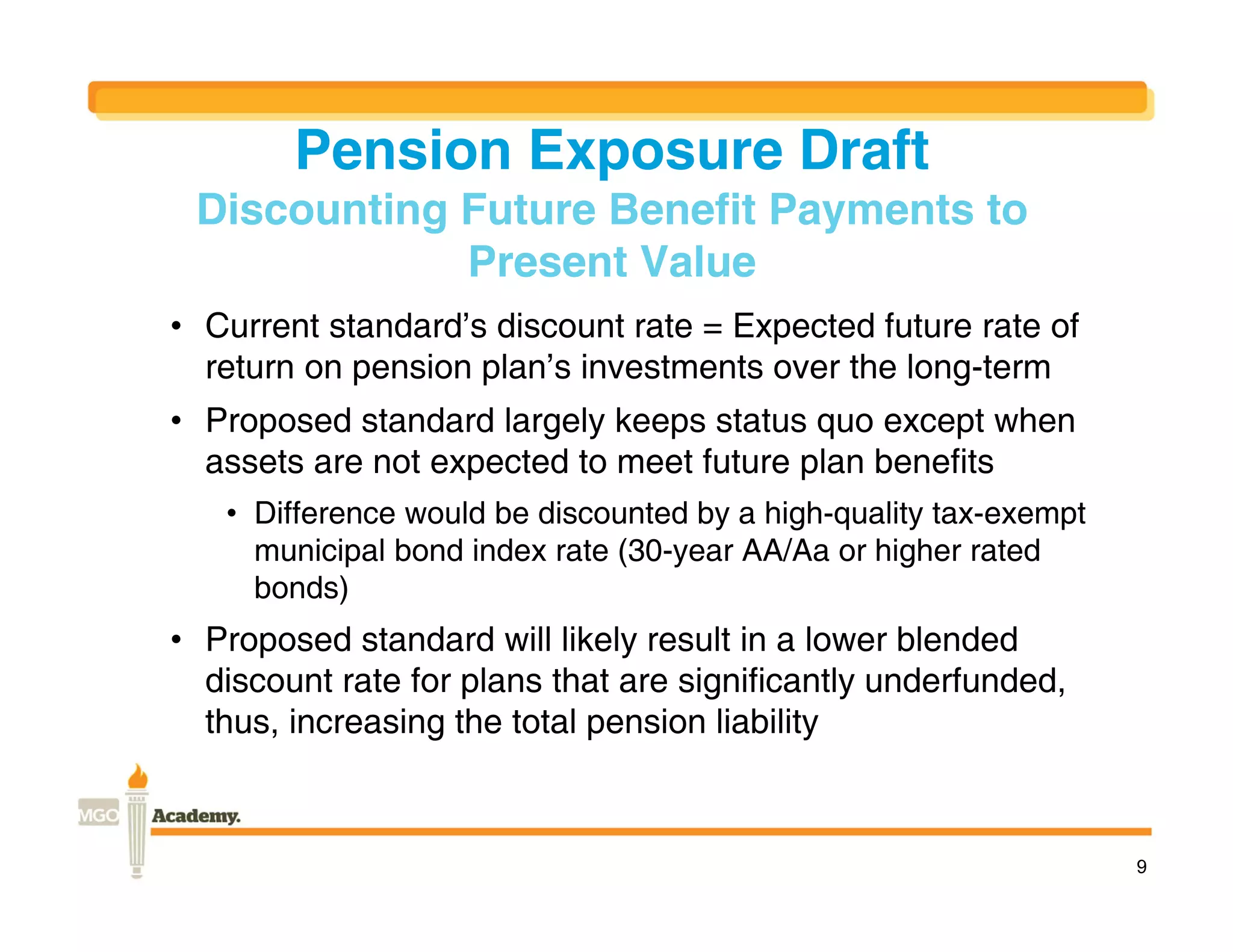

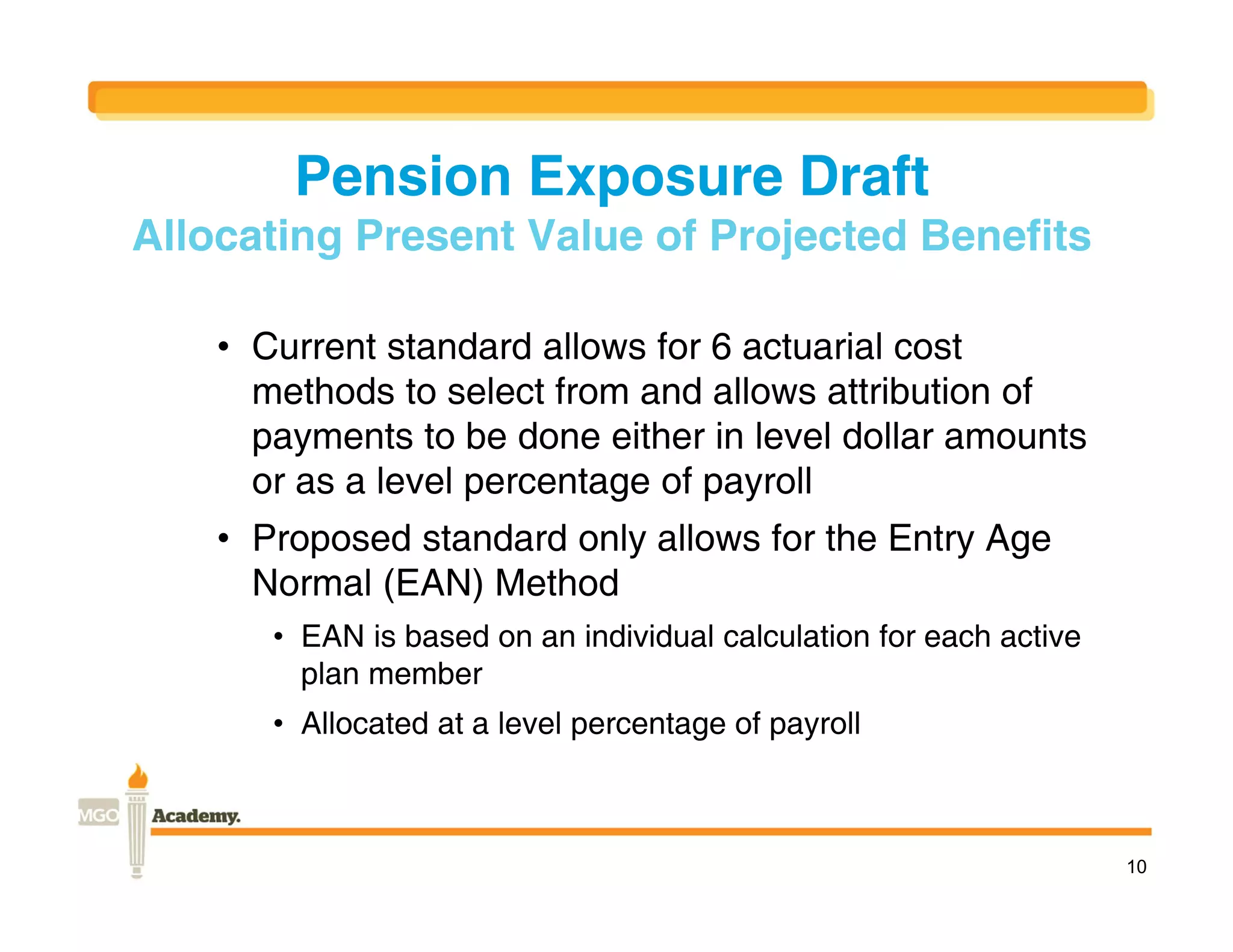

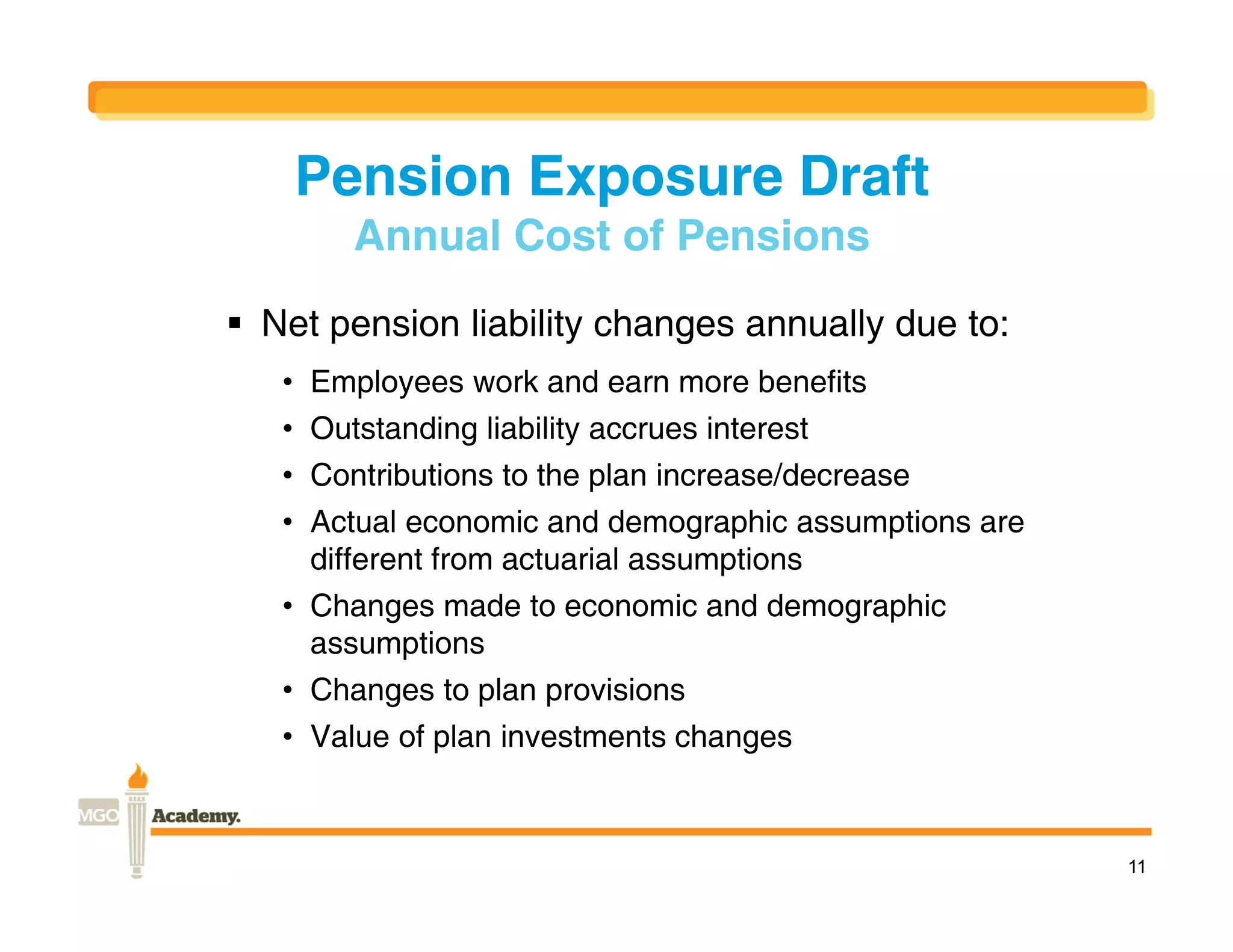

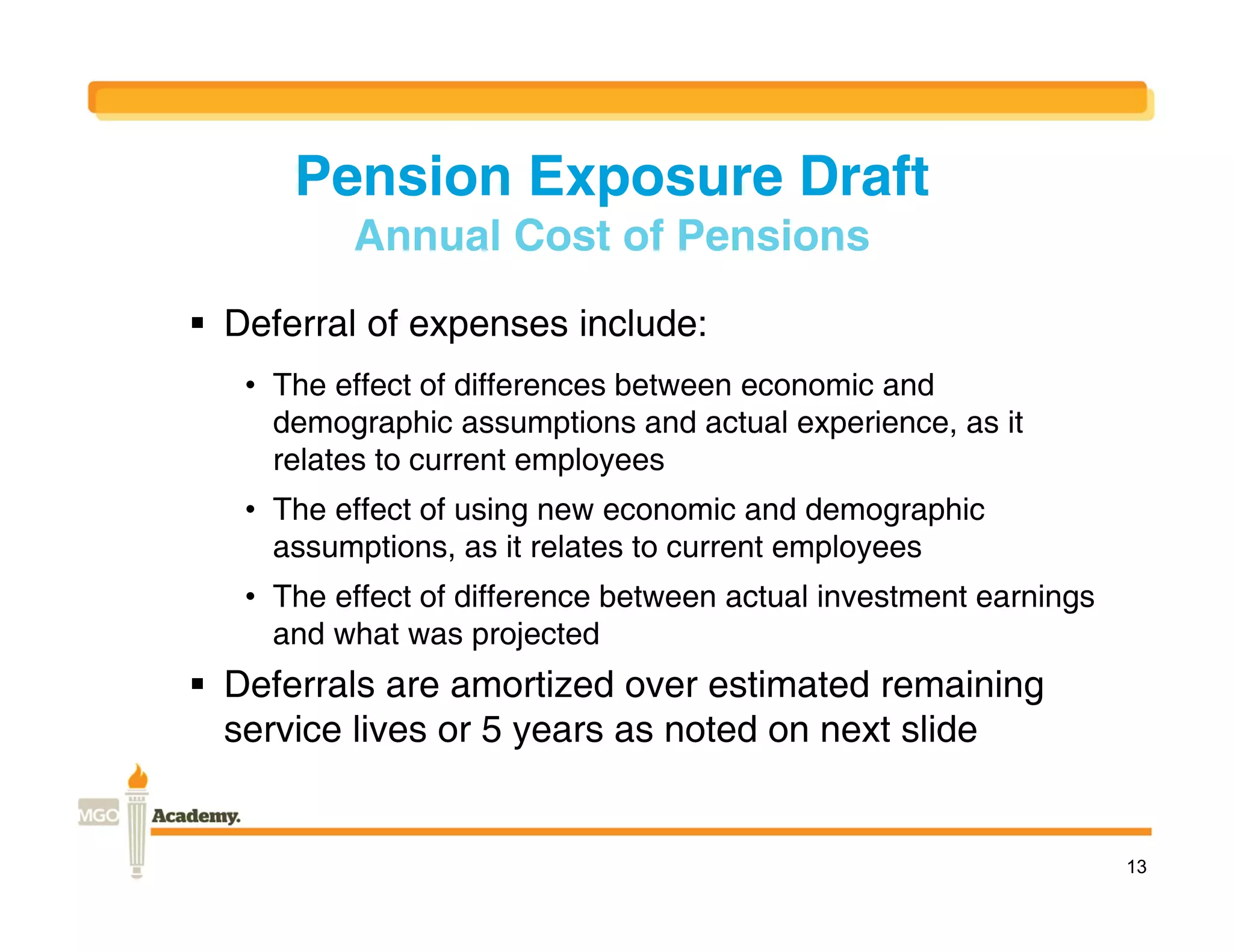

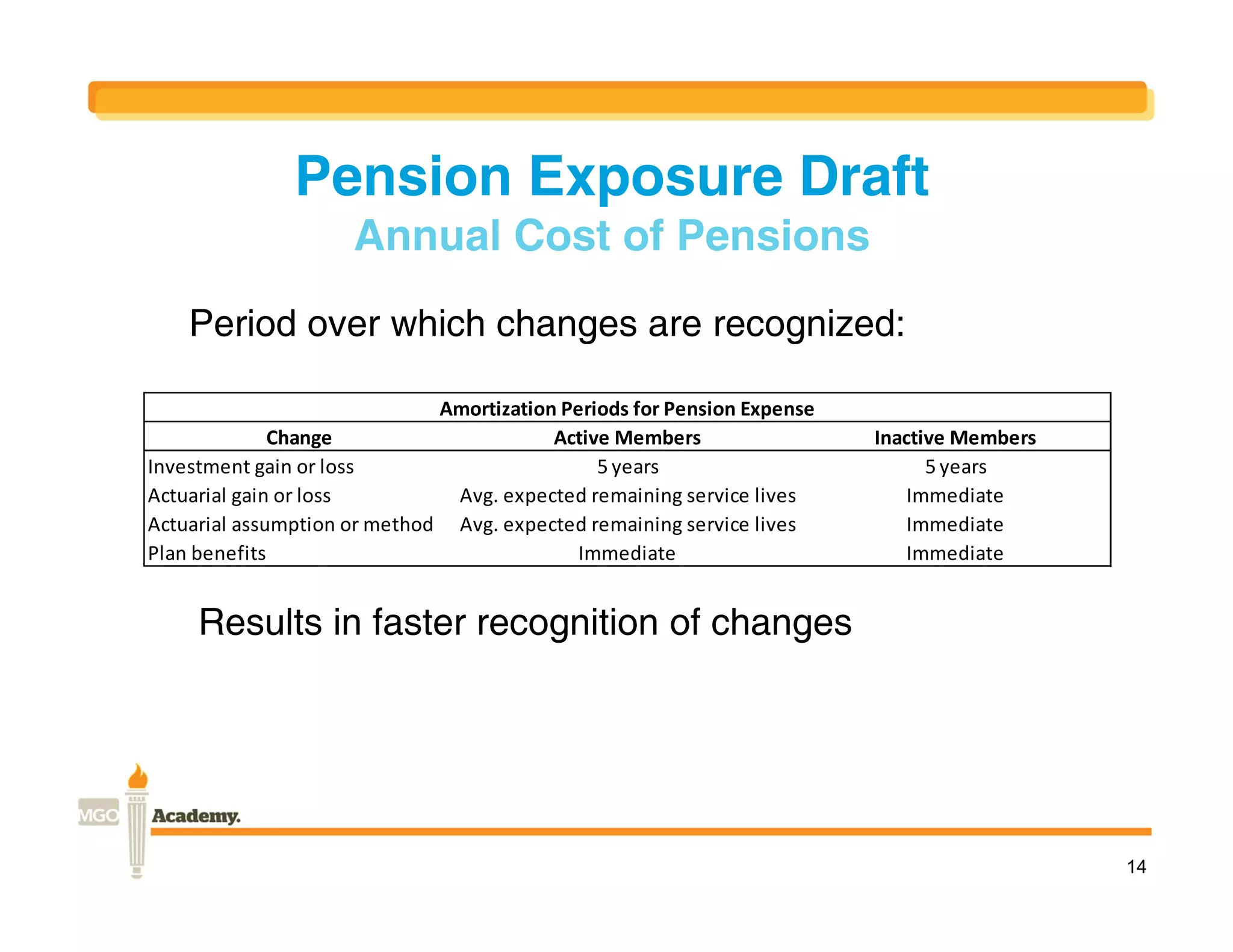

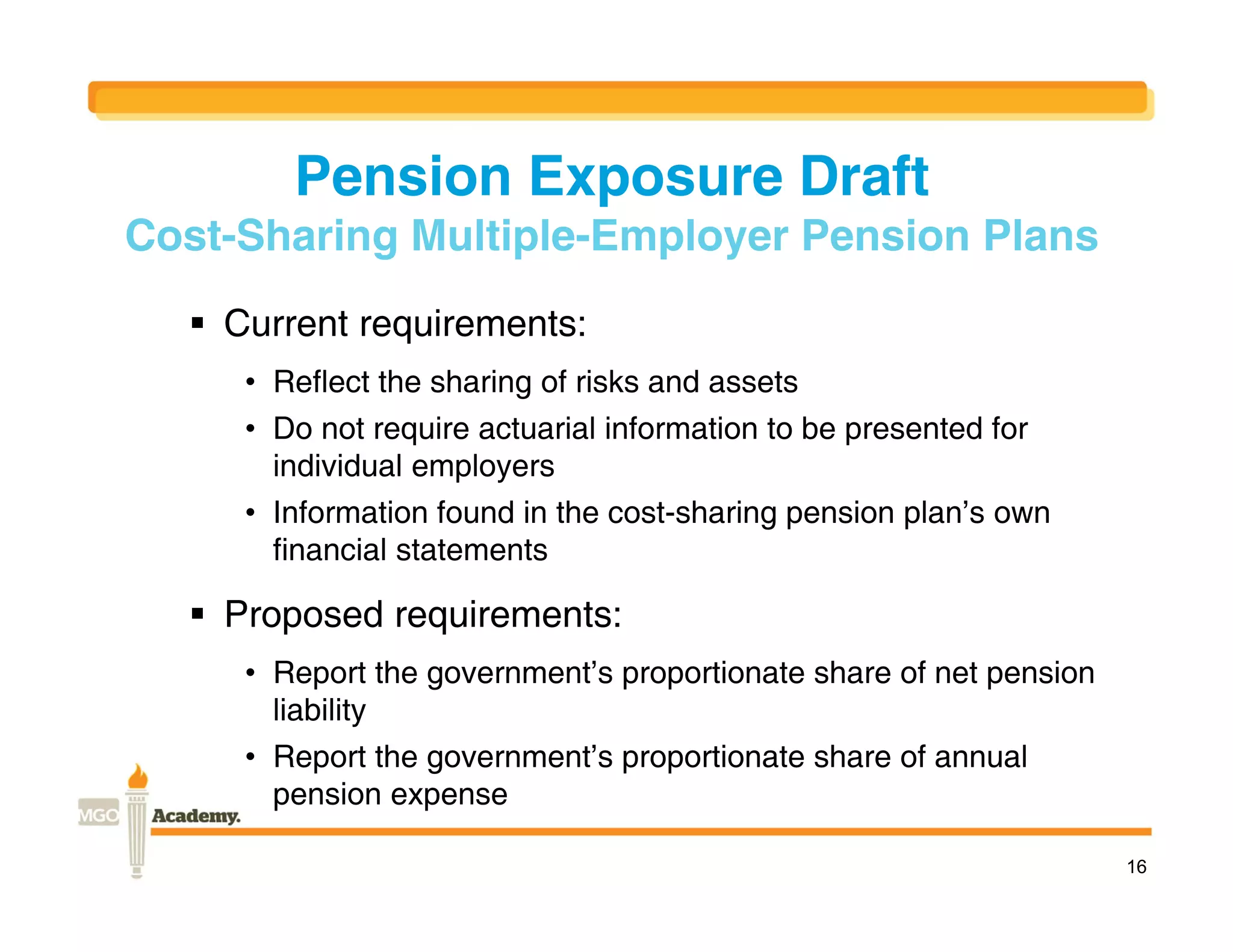

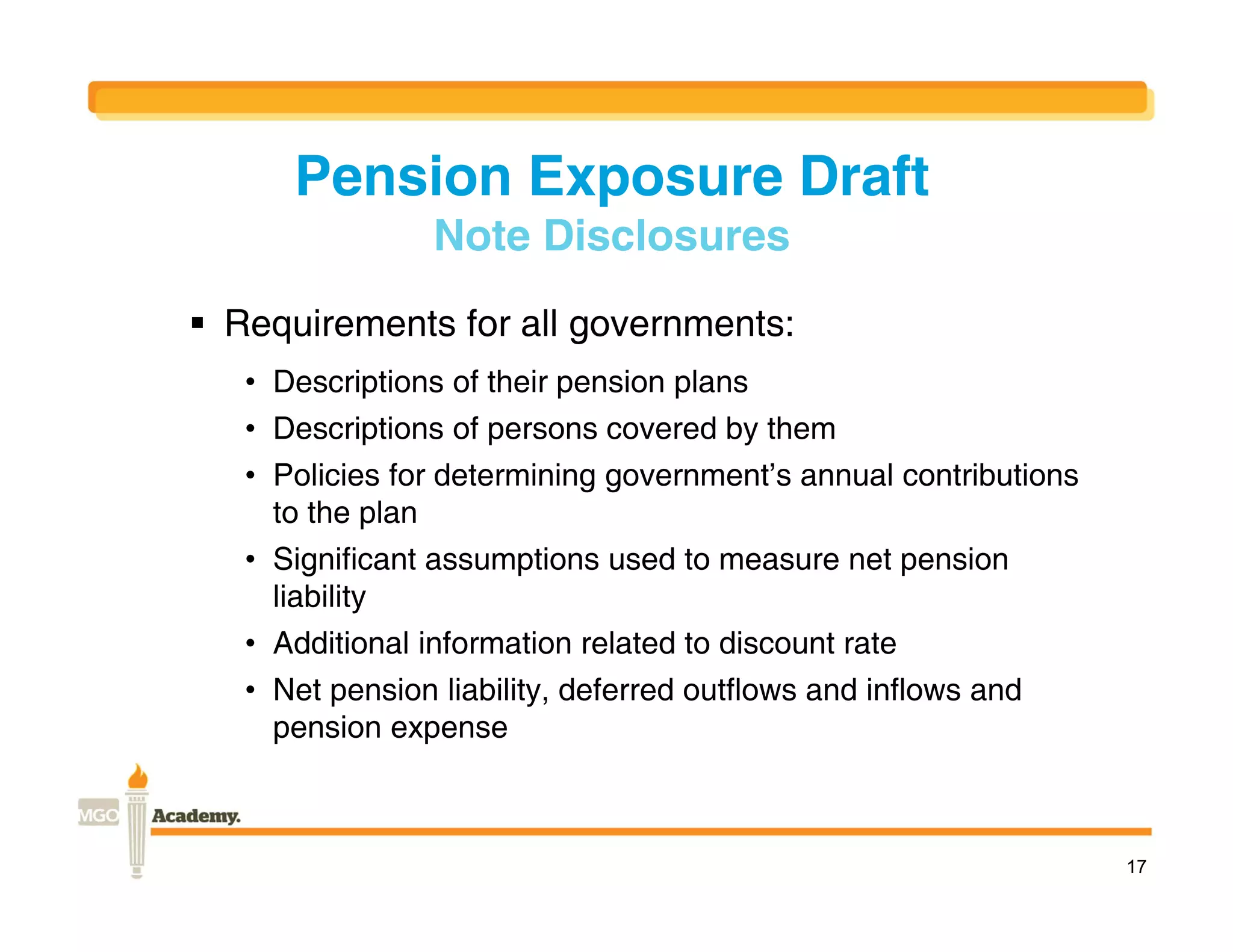

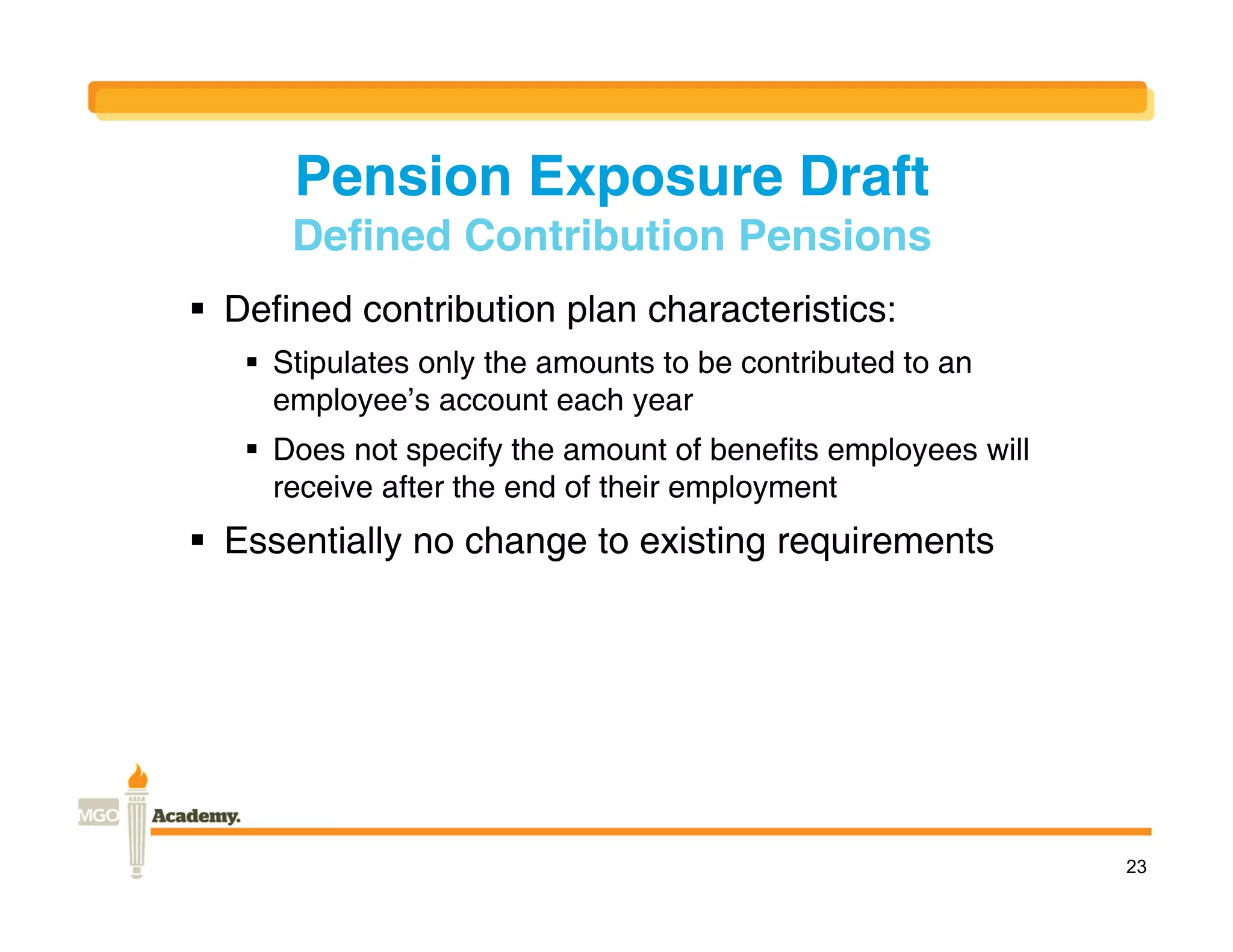

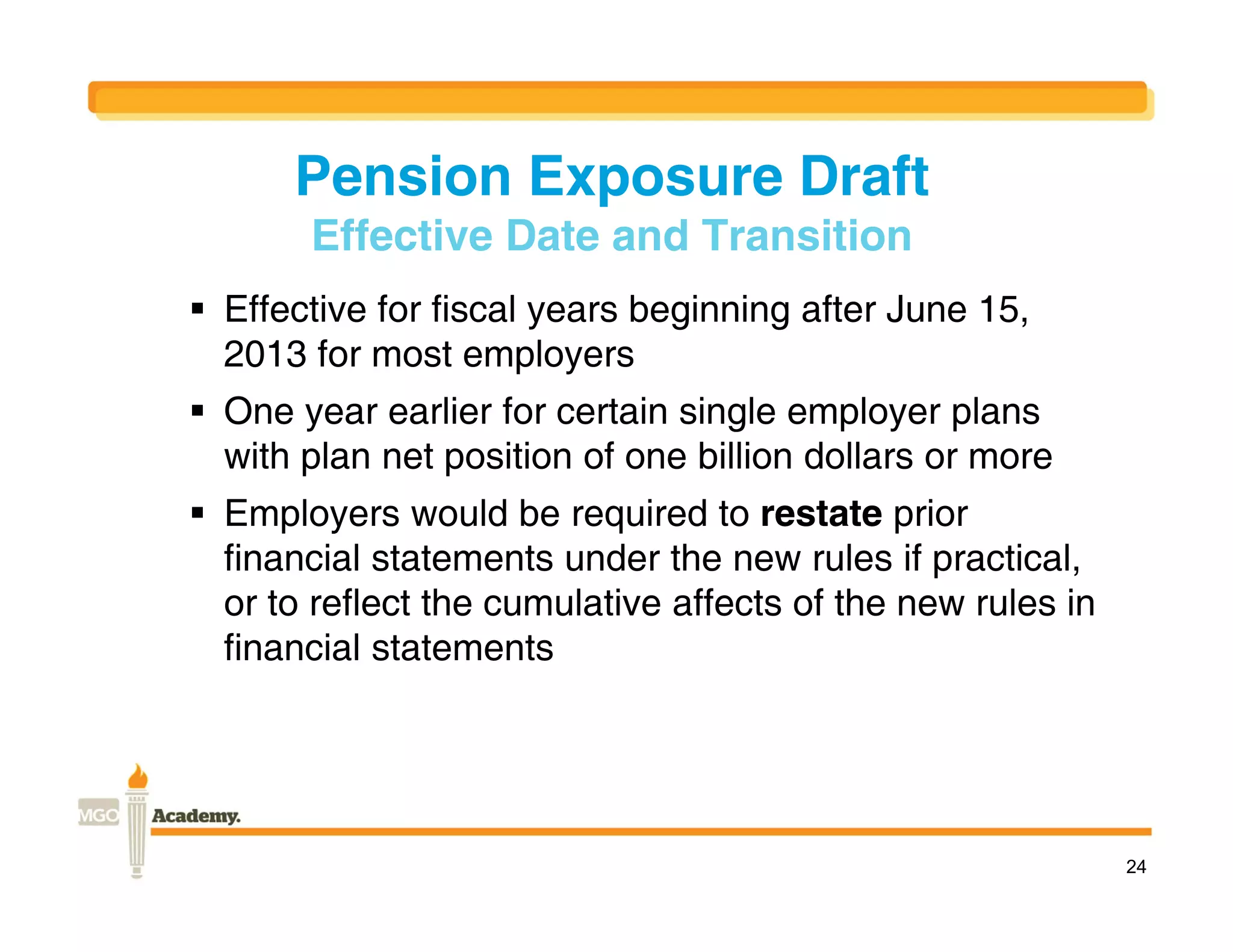

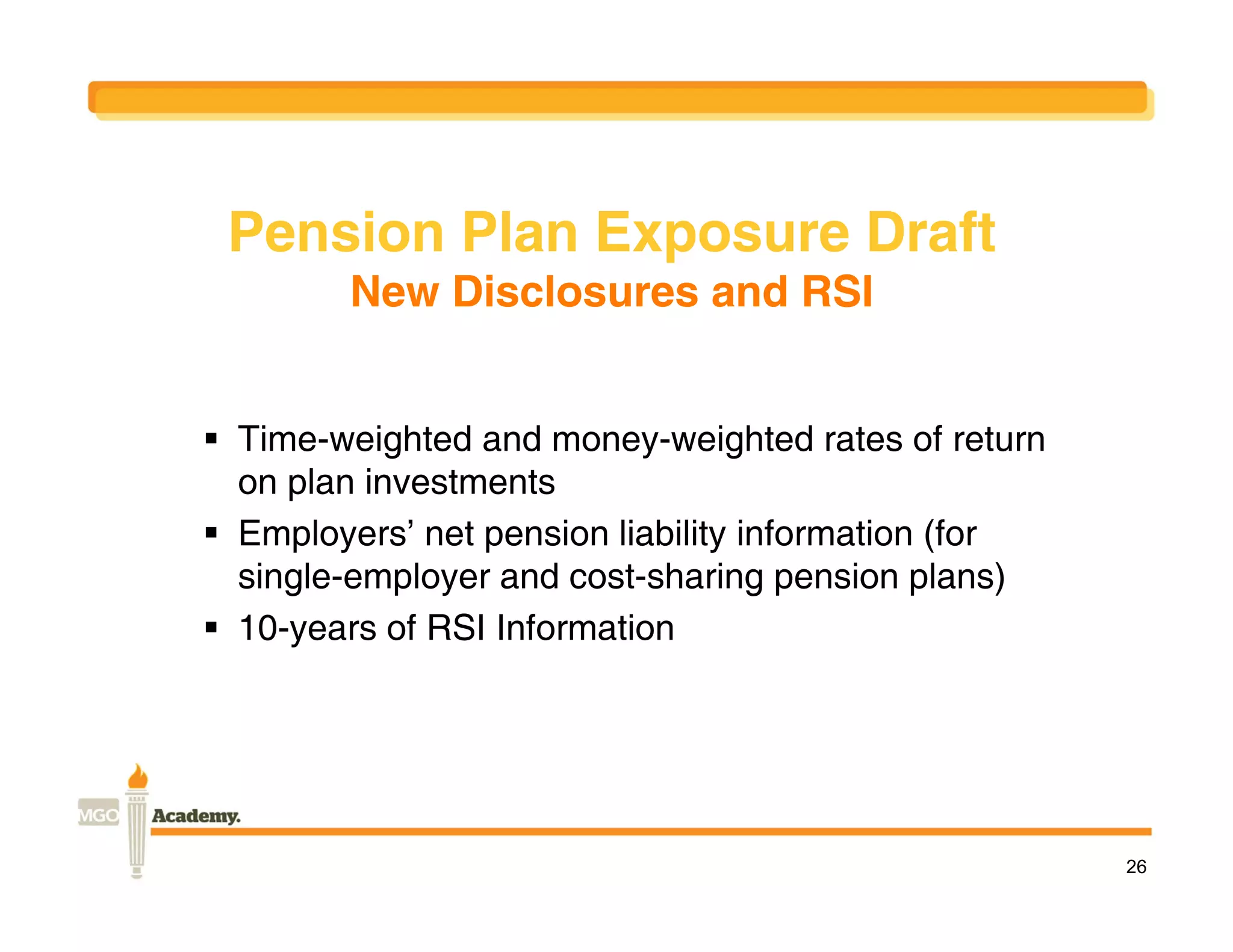

The document summarizes new proposed rules from the Governmental Accounting Standards Board (GASB) regarding pension accounting and financial reporting. The proposed rules would introduce the net pension liability to replace the net pension obligation, separate accounting from funding requirements, and require use of the Entry Age Normal actuarial cost method. If adopted, the rules would substantially increase reported liabilities for most governments and require additional note disclosures and information in required supplementary information. The proposed rules were open for public comment through September 2011.

![[ON-DEMAND WEBINAR] PPP Forgiveness Guidance & CARES Act Impact On Financial ...](https://cdn.slidesharecdn.com/ss_thumbnails/lcpppcaresact-final-200610141735-thumbnail.jpg?width=640&height=640&fit=bounds)