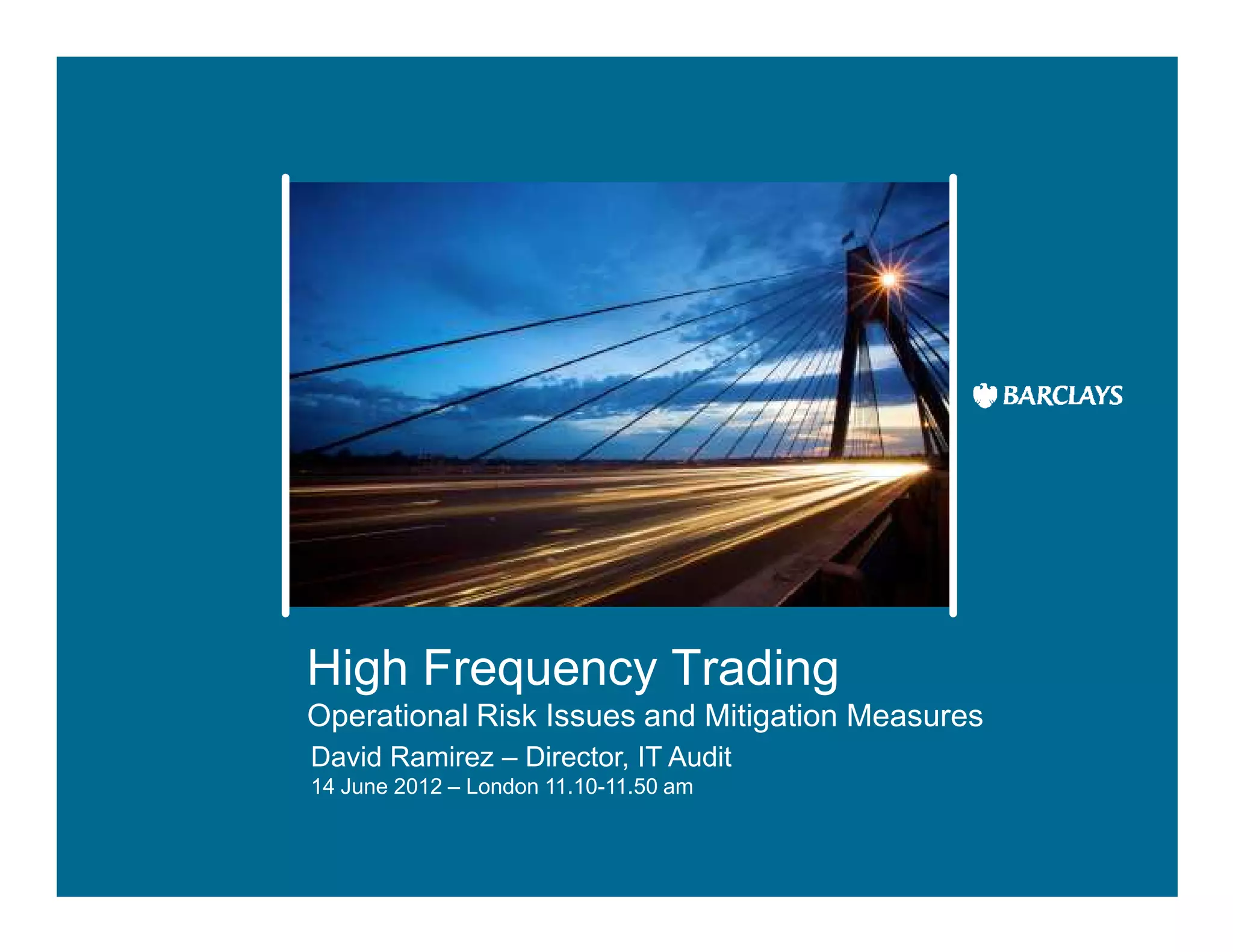

The document discusses operational risk issues in high frequency trading (HFT) and algorithmic trading, including its key concepts, risks, and mitigation measures. Major risks identified include regulatory compliance failures, the removal of human oversight in algorithm execution, extreme market behavior exemplified by the 2010 flash crash, intellectual property theft, and infrastructure security limitations. Mitigation strategies emphasize increased oversight, latency measurement, security reviews, and robust error management to enhance regulatory and operational compliance.