This report analyzes Nike Inc. by four analysts from Temple University's Investment Association. It provides an overview of Nike's operations, financials, strategies, and risks. Nike generates most revenue from footwear but is growing its direct-to-consumer sales. The report recommends buying Nike due to its brand strength, growth in China, and potential for increased revenue and profits through expanding direct online sales and retail stores. However, risks include economic downturns, competition, and reliance on international suppliers.

nike company presentation (nike diversification strategy ) follow me on on instagram @abhasduaxx like share subscribe, hope you like this and enjoy the presentation.

thank you

Brief study on the Nike Sneakers revolution in the sports industry, Background of the company, Founders of the Nike, HARVARD CASE STUDY ON NIKE, SNKRS APP/application revolution, Nike Marketing Strategies, Nike colabaration with NBA Championship,

nike company presentation (nike diversification strategy ) follow me on on instagram @abhasduaxx like share subscribe, hope you like this and enjoy the presentation.

thank you

Brief study on the Nike Sneakers revolution in the sports industry, Background of the company, Founders of the Nike, HARVARD CASE STUDY ON NIKE, SNKRS APP/application revolution, Nike Marketing Strategies, Nike colabaration with NBA Championship,

Shoes On Nike

1

Executive Summary:

Situational analysis

▪ Background data on sales & costs.……………………………………………....Pg. 2

▪ Competitors………………………………………………………………………....Pg. 4

▪ Customers…………………………………………………………………………..Pg. 5

▪ Company …………………………………………………………………………...Pg. 6

▪ Community …………………………………………………………………………Pg. 8

Marketing strategy

▪ Mission ……………………………………………………………………………..Pg. 9

▪ Marketing and financial objectives ……………………………………………...Pg.10

▪ Target Market & Positioning ……………………………………………………..Pg.10

Marketing tactics

▪ Product Offering…………………………………………………………………..Pg. 11

▪ Distribution………………………………………………………………………...Pg. 13

▪ Promotion………………………………………………………………………….Pg. 15

▪ Pricing ……………………………………………………………………………..Pg. 17

Financial projections

▪ Break Even Analysis ……………………………………………………………..Pg. 18

▪ Cost Forecast……………………………………………………………………...Pg. 18

▪ Sales Forecast………………………………………………………………….....Pg. 18

References

▪ References………… ……………………………………………………………..Pg. 20

2

Part 1: Situational Analysis

1.1 Background data on

sales and cost

Nike was founded in the

State of Oregon in January

1996, by a track athlete, Phil

Knight and his coach, Bill

Bowerman (Nike 2017 10-K

Form, 2017).

Being the leader in the

athletic industry, Nike is the world’s largest supplier of athletic wear. Nike’s products are

divided into footwear, clothing, and training accessories. There are eight main

categories of Nike’s brand products. They are: running, soccer, basketball, action

sports, sports-inspired lifestyle products, golf, men’s and women’s training (Nike 2017

10-K Form, 2017).

Comparing Nike’s and

Adidas’ market capitalization

provides evidence of how Nike

grew as a company in athletic

wear during the past 17 years.

In 2001, both Nike and Adidas

started with a market

capitalization of close to 4

3

billion. In 2005, Nike, Inc. gained its lead in the industry, with its market capitalization

grew at a faster rate than Adidas. By 2010, Nike gained a market capitalization of 63.45

billion, and an annual revenue of 19 billion. In 2015, Nike’s market capitalization was

82.6 billion, while market capitalization of Adidas lagged behind at 17.1 billion (image

and text, Leach, 2015). During the 2017 fiscal year, the annual revenue for Nike, Inc. is

$34.4 billion, which rose 8% from the previous year on a currency-neutral basis (Nike

news, 2017).

Nike’s “swoosh” symbol was developed in 1971, and was registered with the

United States Patent and Trademark Office in 1974. Over the years, the Nike brand

became one of the strongest brand in the world. Currently, the Nike brand ranks as the

18th strongest in the world, estimated to be worth 27.0 billion dollars (Interbrand, 2017).

Along with its long-stand slogan “Just Do it,” the Nike brand became the face of the

company. Consumers associate the Nike brand with “superior quality, style, and

reliability” (De.

ProblemThis is a comprehensive problem all contained on this sprea.docxbriancrawford30935

ProblemThis is a comprehensive problem all contained on this spreadsheet tab. FACTS:1. Elliott Incorporated manufactures garden tools, and although the manufacturing equipment is perfectly functional, it is not modern.2. Upgrading to modern equipment would speed up the manufacturing process such that direct labor and variable manufacturing costs would be reduced by 40% on a per-unit basis. Hint: You do not need current units produced to calculate this problem.3. The cost of such an upgrade would equal $1,500,000 per year for depreciation and financing costs net of tax benefits of these costs.4. The additional costs would be accounted for as fixed manufacturing overhead.5. Elliott is currently operating at full capacity and management believes they could increase sales to $6,000,000 at current prices if they had additional capacity.Elliott's current sales and costs are as follows:Sales$4,500,000Direct materials790,000Direct labor1,530,000Manufacturing overhead–variable364,500Manufacturing overhead–fixed750,000Selling expenses–variable110,000Selling expenses–fixed230,000Administrative expenses–variable60,000Administrative expenses–fixed200,000a. Prepare a CVP for Elliott based on the current production.b. Compute contribution margin ratio for current production.c. Compute breakeven dollars for current production.d. Prepare a CVP based on the proposed equipment upgrade.e. Compute contribution margin ratio based on the proposed equipment upgrade.f. Compute breakeven dollars for current production.g. Should Elliott proceed with the proposed upgrade?

RUNNING HEAD: NIKE1

Nike20

Nike

Anita Orzel

Southern New Hampshire University

October 9, 2016

Purpose of the Paper

The aim of the paper is to apply the microeconomic models in the functioning of Nike to ensure that the firm undertakes effective business decisions. The paper will focus on analyzing the history of the Nike Company since its existence until today and evaluate the supply and demand conditions that Nike encounters in the sale of its products. Further, the paper focuses on the price elasticity demand by analyzing the available information that can affect the customer’s responsiveness to purchase their commodities (Distelhorst, Hainmueller, & Locke, 2016). In addition, the paper will discuss the cost of the production by analyzing the cost incurred by the Nike Company in the production process and explore its market performance to ensure that higher profit is generated. This can be done by avoiding and addressing the barriers that are encountered by the company in the marketplace. Finally, the paper will provide effective recommendations that are required to be addressed by the company to manage its future production. This is essential to ensure that the firm achieves its set goals through the evaluation of the demand trends and the price elasticity (Distelhorst, Hainmueller, & Locke, 2016). This paper, therefore, seek to critically analyze th.

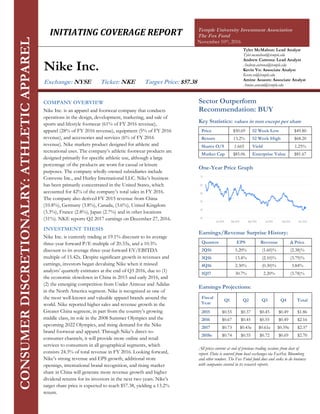

1. INITIATING COVERAGE REPORT Temple University Investment Association

The Fox Fund

November 10th, 2016

Tyler McMahon: Lead Analyst

Tyler.mcmahon@temple.edu

Andrew Cutrona: Lead Analyst

Andrew.cutrona@temple.edu

Kevin Vo: Associate Analyst

Kevin.vo@temple.edu

Amine Aouom: Associate Analyst

Amine.aouom@temple.edu

COMPANY OVERVIEW

Nike Inc. is an apparel and footwear company that conducts

operations in the design, development, marketing, and sale of

sports and lifestyle footwear (61% of FY 2016 revenue),

apparel (28% of FY 2016 revenue), equipment (5% of FY 2016

revenue), and accessories and services (6% of FY 2016

revenue). Nike markets product designed for athletic and

recreational uses. The company’s athletic footwear products are

designed primarily for specific athletic use, although a large

percentage of the products are worn for casual or leisure

purposes. The company wholly-owned subsidiaries include

Converse Inc., and Hurley International LLC. Nike’s business

has been primarily concentrated in the United States, which

accounted for 42% of the company’s total sales in FY 2016.

The company also derived FY 2015 revenue from China

(10.8%), Germany (3.8%), Canada, (3.6%), United Kingdom

(3.3%), France (2.8%), Japan (2.7%) and in other locations

(31%). NKE reports Q2 2017 earnings on December 27, 2016.

INVESTMENT THESIS

Nike Inc. is currently trading at 19.1% discount to its average

three-year forward P/E multiple of 20.33x, and a 10.5%

discount to its average three-year forward EV/EBITDA

multiple of 15.42x. Despite significant growth in revenues and

earnings, investors began devaluing Nike when it missed

analysts’ quarterly estimates at the end of Q3 2016, due to (1)

the economic slowdown in China in 2015 and early 2016, and

(2) the emerging competition from Under Armour and Adidas

in the North America segment. Nike is recognized as one of

the most well-known and valuable apparel brands around the

world. Nike reported higher sales and revenue growth in the

Greater China segment, in part from the country’s growing

middle class, its role in the 2008 Summer Olympics and the

upcoming 2022 Olympics, and rising demand for the Nike

brand footwear and apparel. Through Nike’s direct-to-

consumer channels, it will provide more online and retail

services to consumers in all geographical segments, which

consists 24.3% of total revenue in FY 2016. Looking forward,

Nike’s strong revenue and EPS growth, additional store

openings, international brand recognition, and rising market

share in China will generate more revenue growth and higher

dividend returns for its investors in the next two years. Nike’s

target share price is expected to reach $57.38, yielding a 13.2%

return.

CONSUMERDISCRETIONALRY:ATHLETICAPPAREL

Nike Inc.

Exchange: NYSE Ticker: NKE Target Price: $57.38

Sector Outperform

Recommendation: BUY

Key Statistics: values in mm except per share

Price $50.69 52 Week Low $49.80

Return 13.2% 52 Week High $68.20

Shares O/S 1.665 Yield 1.25%

Market Cap $85.06 Enterprise Value $81.67

One-Year Price Graph

Earnings/Revenue Surprise History:

Quarters EPS Revenue Δ Price

2Q16 5.20% (1.60)% (2.38)%

3Q16 13.4% (2.10)% (3.79)%

4Q16 2.30% (0.30)% 3.84%

1Q17 30.7% 2.20% (3.78)%

Earnings Projections:

Fiscal

Year

Q1 Q2 Q3 Q4 Total

2015 $0.55 $0.37 $0.45 $0.49 $1.86

2016 $0.67 $0.45 $0.55 $0.49 $2.16

2017 $0.73 $0.43e $0.61e $0.59e $2.37

2018e $0.74 $0.55 $0.72 $0.69 $2.70

All prices current at end of previous trading sessions from date of

report. Data is sourced from local exchanges via FactSet, Bloomberg

and other vendors. The Fox Fund fund does and seeks to do business

with companies covered in its research reports.

2. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 2

SEGMENTS OVERVIEW

Geographic Segments

North America Market

Nike Brand & Converse sales in the

United States accounted for

approximately 45% in its 2015 and

2014 fiscal years. Nike Brand, Jordan

Brand, Hurley and converse products

are sold in thousands of retailers

around the country. Products are

found in various footwear stores,

sporting goods stores, athletic

specialty stores, department stores,

skate, tennis and golf shops and other

retail accounts. Nike has 185 Nike

Brand factory stores, 33 Nike Brand

in-line stores, 92 Converse stores, and

29 Hurley stores operating within the

United States.

International Market

For both fiscal 2015 and fiscal 2014, non-U.S. NIKE Brand and Converse sales accounted for 54% of total revenues.

Nike sells its products to retail accounts, through its own Direct to consumer operations as well as through a mix of

independent distributors, licensees and sales representatives around the world. Nike sells to thousands of retail accounts

and ships products to 45 distribution centers outside the United States. Nike has 512 Nike Brand factory stores, 73 Nike

Brand in-line stores, and seven Converse stores operating internationally.

Product Segments

Footwear

Nike’s athletic footwear products are designed primarily for specific athletic use, although a large percentage of the

products are worn for casual or leisure purposes. Nike focuses on innovation and high-quality construction for all of

their products. Sportswear, running, the Jordan Brand and soccer are currently Nike’s best-selling footwear categories.

Apparel

Nike sells apparel covering the above-mentioned categories, which are sold predominantly through the same marketing

and distribution channels as athletic footwear. Footwear, apparel and accessories are often marketed in “collections” of

similar use or by category. Nike apparel is also marketed with licensed college and professional team and league

logos. Nike’s sports apparel, similar to our athletic footwear products, are designed primarily for athletic use and

exemplifies the company's commitment to create innovative and high-quality products. Sportswear, men’s training,

running, soccer and women’s training are currently Nike’s top-selling apparel categories.

Equipment

Nike sells a line of performance equipment and accessories under the NIKE Brand name, including bags, socks, sport

balls, eyewear, timepieces, digital devices, bats, gloves, protective equipment, golf clubs and other equipment designed

for sports activities. The company also sell small amounts of various plastic products to other manufacturers through

our wholly-owned subsidiary, NIKE IHM, Inc.

Other

The Jordan Brand designs, distributes and licenses athletic and casual footwear, apparel and accessories predominantly

focused on basketball using the Jumpman trademark. Hurley, a subsidiary of Nike, designs and distributes a line of

action sports and youth lifestyle apparel and accessories under the Hurley trademark. Sales and operating results for

Hurley are included within the Nike Brand Action Sports category and within the North America geographic operating

segment. Another of Nike wholly-owned subsidiary brands, Converse, designs, distributes and licenses casual sneakers,

apparel and accessories under the Converse, Chuck Taylor, All Star, One Star, Star Chevron and Jack Purcell trademarks.

3. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 3

INDUSTRY OVERVIEW

Footwear Market

The global footwear market has seen

diversified trends across different geographic

regions such as North America, Europe, Asia

Pacific, and Rest of the World. The global

footwear market is driven by factors such as

growing demand for new design of footwear

and growing awareness about healthy and

active lifestyle. Increasing population,

propensity of people to spend more and

emerging retail outlets have also attributed to

the growing demand for footwear across the

global market. Also, there are certain

restraints which are slowing down the growth

of the global footwear market. Increasing

environmental concerns and rising prices of

raw material are the main factors which are

acting as restraints for the global footwear

market. The footwear market has been

divided into three segments: by types of

footwear, by consumer group, and by

geography. Further, the by types of footwear

include athletic footwear and non-athletic

footwear. The report also offers competitive

analysis about sub-segment of athletic

footwear and non-athletic footwear. Athletic

footwear segment offers products of four

categories which include insert shoes, sports

shoes, hiking shoes and backpacking boots.

Sports shoes are expected to have the largest

market in terms of volume globally from

2014 to 2020.

Industry/Consumer Trends

Consumer group, which includes men,

women, and kids. The men's footwear

market accounts for maximum market share

followed by women and kids. In terms of

value, North America is expected to have the

largest market share for consumer group

footwear market from 2014 to 2020.

Globally, Asia Pacific accounts for the

maximum share for consumer group

footwear market in terms of volume during

the forecast period. This market research

study analyzes the global footwear market

and provides estimates in terms of revenue

(USD Million) and volume (Million Units)

from 2014 to 2023. It recognizes the drivers

and restraints affecting the industry and

analyzes their impact over the forecast period

from 2015 to 2023. Moreover, it identifies

the significant opportunities for market

growth in the years to come.

MOATS

Pricing Power: As the leading player in the $320 billion global athletic

footwear, apparel, and equipment market (according to NPD Group

estimates), we believe Nike has developed a wide moat via its superior

product-development capabilities, universally recognized brands, and

economies of scale. Nike's global brand reach, including a strong presence in

emerging markets, is the result of core research and development capabilities

and a marketing budget of more than $3 billion (including endorsements from

some of the most popular global athletes). As a result, consumers have shown

a propensity to pay premium prices for Nike's products. With leading market

share in a variety of categories including sportswear ($6.6 billion), running

($4.9 billion), basketball ($3.7 billion), and athletic training ($3.8 billion in

annual sales), Nike can exert a significant amount of influence over retailers,

many of whom rely on its products to drive customer traffic.

Rights & Endorsements: Nike is a company driven to provide innovative

and quality products for athletes all over the world. Its powerful brand puts

them in position to have rights with and endorsement deals with the biggest

names in sports. Nike has renewed its massive NFL on-field apparel rights

contract, adding three years to the five-year deal that took effect in 2012. The

on the field rights extension also blocks competitors like Under Armour from

the valuable partnership until 2019. Nike also has endorsements deals with

some of the largest athletes in sports that include Lebron James, Kevin

Durant, Cristiano Ronaldo and Rodger Federer. Their ability to have

endorsements with players in all different sports gives their brand exposure in

all athletics. This influential marketing strategy will continue to build Nike’s

brand as well as increase sales for all of their products.

RISKS

Economic Trends: Nike's intrinsic value can be influenced by global

economic trends, including discretionary spending patterns and exchange

rates. Industry competition, particularly from Under Armour, Adidas, and

Puma is always present and could also come from new entrants in developing-

market economies such as China. Changes in consumer tastes and preferences

are always a risk in athletic footwear and apparel categories, and despite

performance attributes, products do have a strong element of fashion. As

sportswear and women's segments grow faster than core sports apparel, sports

footwear and equipment, we believe there could be greater volatility and

fashion risk. With more than half of its sales coming from outside the U.S.

and a heavy concentration of Asia-based suppliers, the firm does face the risk

of increased import costs and currency volatility, which cannot be hedged

indefinitely.

Future Growth: Nike has experienced strong growth in its home market as

the brand's popularity has been ever increasing in recent years. We note that

some athletic segments, such as basketball where Nike is dominant, tend to be

somewhat cyclical with fashion trends and investors should be wary of

extrapolating trends too far into the future. Other categories, such as running,

have a more functional component and brand loyalty as runners are wary of

switching brands for fear of injury. Currently, Nike appears to be gaining from

an increase in sports participation globally. Although the company has always

succeeded with a wholesale-dominated strategy, recent gains and increasing

management emphasis on direct-to-consumer channels pose execution risks.

Retail channels require greater investment and higher overhead; profits also

tend to be more cyclical with the economy. In the near term, direct-to-

consumer sales could increase growth and profitability, but investors run the

risk that such investments could dilute returns in the longer term.

4. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 4

CATALYSTS

Direct-to-Consumer Sales

Nike’s (NKE) DTC (direct to consumer)

channel includes sales made online on

Nike.com and through its own retail stores.

Nike’s direct to consumer operations sell

NIKE Brand, Jordan Brand, Hurley and

Converse products to consumers. At the end

of FY 2015, Nike had about 931 retail

locations, in which it expanded its store

count by 73 in FY 2015. At the end of FY

2016, Nike had about 1045 retail locations,

expanding its store count by 114 in its most

recent FY. In contrast, Adidas (ADDYY)

closed a net total of 191 stores in 2015.

While wholesale revenues remain the largest

component of overall NIKE Brand

revenues, Nike continues to expand its DTC

businesses in each of its geographies. Nike's

direct-to-consumer business helps cut out

the middleman that would normally pocket a

percentage of sales. Through e-commerce, Nike can eliminate much of the fixed cost associated with physical stores

while also increasing its ability to up-sell products. For instance, the company's NikeID service allows customers to

create custom shoes with their own designs and colors, for a fee of course. The contribution from the DTC channel has

been rising steadily over the past few quarters for Nike. For FY 2016, DTC revenues represented approximately 26% of

total NIKE Brand revenues, up from 20% in FY 2014 and 23% in FY 2015. It is likely to make up even more of the top

line in the future as the company continues to invest in digital infrastructure and increase its number of owned stores.

On a currency-neutral basis, DTC revenues increased 25% for FY 2016, driven by strong online sales growth, the

addition of new stores and comparable store sales growth of 10%. While total sales rose 8%, Nike.com sales increased a

full 49% YoY. This follows a 46% rise between FY 2015

and 2016. In FY 2016, online sales represented

approximately 22% of total NIKE Brand DTC revenues. In

2015, Nike outlined a goal of reaching $50 billion in revenue

by 2020, an increase on the top line of $20 billion from

$30.6 billion in FY 2015. Half of that growth is expected to

come from the direct-to-consumer (DTC) channel, which

includes Nike's own stores and e-commerce as it expects

DTC to grow from $6.6 billion in FY 2015 to $16 billion in

FY 2020. In other words, the burden on futures orders or

wholesale to deliver growth will be significantly less than it

has been in the past. E-commerce will be a key driver of

that growth. Nike expects E-commerce revenue to reach $7

billion by FY 2020. The surge in online sales comes not only

from the growing trend toward online shopping, but also from some key investments Nike has made. A few such

investments include creating seamless ways to shop both in Nike stores and online by having tablets in store to order

anything not in stock at that time. Another investment has been building out a series of mobile apps that connect with

consumers more personally and to allow them to make purchases easily from their smartphone. The next generation of

Nike's mobile shopping plan was recently launched called Nike+. Nike+ is a mobile app that allows users to track

workouts, contact Nike support, see trending news, and utilize the in-app shopping feature, which makes

recommendations based on the user's activities and habits. The gross margin Nike enjoys on its direct-to-consumer sales

is higher than when its items are sold wholesale, Nike gets to charge a higher selling price for online customized NikeID

gear without much change in material or manufacturing, and Nike is expanding internationally by building out more

robust online sales channels and doubled its number of local online storefronts in specific countries from 20 to 40. All

of these initiatives will continue to grow Nike's online sales which will directly benefit the company's bottom line.

5. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 5

China Emerging Market

Nike is a leader in the sportswear industry and its brand visibility is growing immensely in China as fitness is becoming a

staple in Chinese daily life. In June, China’s State Council approved a National Fitness Plan which sets ambitious targets

to improve national fitness, increase sports participation and encourage people to incorporate regular physical activities

into their weekly routines. The government will invest in the construction of new public sports facilities such as fitness

centers, sports venues and stadiums, and implement fitness and sports activities programs. Assuming, rather

conservatively, that China's fitness industry grows in line with the country's GDP, it is likely to be worth more than $200

billion by 2020. Currently, China accounts for $3,785 million dollars in sales (11.7% of total sales) which is 32% of all

international sales. Sportswear, basketball and Jordan have all been driving revenues for Nike in China. As it stands,

footwear is Nike's leading revenue contributor in China but apparel could reduce the gap with the rise of the Chinese

fitness industry. Since FY 2014 Nike’s sales in China have from $2.602 billion to $3.785 billion, a 45.5% increase over

two years. This will boost demand for Nike's athletic merchandise immensely. Analysts believe global name brands such

as Nike who endorse big name athletes are dominant players for accelerated growth as China brands have yet to

successfully penetrate the market. Nike endorses iconic athletes and sports teams around the world such as LeBron

James, Christiano Ronaldo, FC Barcelona, etc. contributes heavily to their commitment to innovative products and

continued sales growth around the world. Nike’s sales in China are projected to rise to $4,967 billion in FY 2018, a 29%

increase from sales in 2016. We believe this is a conservative estimate as China has a growing middle class of nearly 220

million citizens compared the United States 121 million. Due to Nike’s strong brand reputation and awareness, we

believe Nike has an extreme growth opportunity in China as it is the global leader in sports footwear, apparel and

equipment internationally. Nike will continue to have great international growth as it isn't a business that merely sells

apparel or athletic footwear, it thrives by selling its brand.

Seasonal Revenue Headwinds

Retail industries benefit particularly well from the Thanksgiving to New Year’s period. Retailers do 20 to 30 percent of

the year’s business during the holiday season. Nike has seen superb growth after the holidays in Q3 (November to

February) as it reported earnings growth of 17.1% YoY growth from FY 2014 to FY 2015 and 23.6% YoY growth from

FY 2015 to FY 2016. Holiday spending is expected to increase 10% compared to the 2015 holiday season which is its

highest point since the Great Recession. Consumer purchases climbed 0.5% in September, the most in three months as

incomes grew, signaling momentum in the biggest part of the U.S. economy. We believe this trend will continue into the

holidays as consumer will spend an average of $935.58 during the holiday season. The increase in spending will certainly

help boost retail sales especially for a leading footwear and apparel retailer like Nike.

6. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 6

FINANCIALS

Revenue

Nike derives its revenue from five

segments: Footwear (61.4% of FY 2016

revenue), Apparel (28.0%), Equipment

(4.5%), Global Brand Divisions (0.2%),

and Converse (6.0%). Since FY 2013, total

revenue has grown from $25.3 billion to

$32.4 billion, illustrating an 8.5% CAGR.

Sales from its Footwear segment increased

by 8.5% YoY, accounting 51.1% ($3.6

billion) of all revenue growth since 2013.

Every geographical segments are expected

to generate higher sales for FY 2016, in

part from its direct-to-consumer channels

consisting 22.4% of total revenue. Due to

high demands for the company’s brand

products, its strong initiative for

innovation will develop further brand

connections and compelling retail experiences to consumers online and across NIKE-owned and retail partner stores.

International success is a key factor to Nike’s growth as every international region achieved double-digit growth in sales

on a currency neutral basis. Going forward, Nike will increase its revenue at 8.31% CAGR from $32.4 billion to $37.9

billion in FY 2018, driven by innovation and strong growth in brand product lines.

North America (45.5% of FY 2016 Revenue)

The North America segment increased its revenue from $11.2 billion to $14.8 billion from FY 2013 to FY 2016, at a

CAGR of 9.7%. Sales of footwear accounted 63.0% of total revenue in FY 2016, which grew 9.3% YoY from $8.5

billion in FY 2015 to $9.3 billion. The company’s strength in footwear sales, due to higher demand and preferences for

the Jordan Brand footwear, have generated higher revenue growth in this segment. With the emergence of direct-to-

consumer channels through online shopping and retail stores, Nike has the advantage to drive up sales in the domestic

market.

Europe (22.6% of FY 2016 Revenue)

The Europe segment reported revenue of $7.31 billion at the

end of FY 2016, an increase of 34.9% from $5.42 million in

FY 2013 (10.5% CAGR). Revenues in Western Europe

increased by 14% with double-digit growth in every territory,

leading the pack by UK & Ireland, and AGS (Austria,

Germany and Switzerland), with growth rates of 12% and

16% respectively. Sales from DTC grew 28% for FY 2016,

due to the strength of online sales growth, the addition of

new stores, and the growth of comparable store sales at 13%

within this segment.

Greater China / Japan (14.4% of FY 2016 Revenue)

Revenue from the Greater China and Japan segment have

grown at a CAGR of 4.5%, from $3.35 billion in FY 2013 to

$3.82 billion in FY 2016. Sales in China attributed all of

revenue growth with $1.3 billion, offsetting losses of $7

million from the Japanese market since 2013. China’s massive

market size, with the growth of the country’s middle class and rising popularity of basketball, will provide the advantage

to boost demand for Nike’s products. With the company’s market share over 10% in China, Nike is expected to drive

higher revenues and sales in this segment.

Emerging Markets (11.4% of FY 2016 Revenue)

Revenue from the Emerging Markets segment fell from $3.8 billion in FY 2013 to $3.7 billion, the only geographical

segment to report revenue losses.

7. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 7

Margins

From FY 2014 to FY 2016 gross margin has expanded

from 44.8% to 46.2%, operating margin has expanded

from 13.2% to 13.9% and profit margin has expanded

from 9.7% to 11.6%. NIKE, Inc. gross margin

expanded 20 basis points between FY 2015 and FY

2016. Gross margin increased primarily due to higher

full-price average selling price and the favorable impact

of growth their higher-margin direct to consumer

(DTC) businesses. However gross margin expansion

was partially offset by higher product costs, primarily

due to shifts in mix to higher-cost products and labor

input cost inflation, higher off-price mix and

unfavorable changes in foreign currency exchange rates.

NIKE Brand product’s higher full-price average selling

price (ASP) increased gross margin approximately 190 basis points in FY 2016 due to innovative premium products with

higher prices and, to a lesser extent, inflationary price increases. Growth in Nike’s higher-margin direct to consumer

(DTC) business increased gross margin approximately 20 basis points in FY 2016. Higher NIKE Brand product costs

decreased gross margin approximately 70 basis points in FY 2016 due to a shift in their product mix to higher-cost

products and input labor cost inflation which was only slightly offset by lower input material costs. Clearing excess

inventory in North America through off-price products decreased gross margin approximately 30 basis points in FY

2016. Unfavorable changes in foreign currency exchange rates decreased gross margin approximately 40 basis points in

FY 2016. Higher product design and development costs decreased gross margin approximately 20 basis points in FY

2016. Converse’s shift to a lower-margin product mix decreased gross margin approximately 20 basis points in FY 2016.

In FY 2015, Nike’s gross margin expanded 120 basis points over FY 2014. Nike’s gross margin benefited from

delivering innovative, premium products that command higher prices while maintaining a balanced price-to-value

proposition for consumers. Nike has been steadily changing its sales mix toward higher priced products which has

helped to increase sales revenue faster than sales volume. For example, in FY 2015 Nike increased footwear unit sales

9% while growing revenue 13% and 17% excluding foreign currency fluctuations, showing the effect of Nike's pricing

power in footwear. The company forecasts re

aching $50 billion in annual sales by 2020. At its current profit margin, that would mean net income of $5.81 billion, a

35% increase over fiscal year 2016. From the premium pricing to efficiency gains and cost management, Nike is likely to

see its profit margin increase even further as net income continues to increase. Currency exchange rate fluctuations and

excess inventories or inventory shortages could result in lower revenues and higher costs which could hinder future

margin expansion.

Earnings

CVS Health has missed earning in Q1 and Q2 on FY

2016. Although the official earnings numbers reflected a

decrease from the prior-year-periods, the news was not

surprising or that concerning. The negative comparisons

stemmed from the costs related to the acquisitions of

Omnicare and Target’s in-store pharmacies and clinics

that took place in December of 2015. As mentioned

before, besides paying $542 million of debt and $114

million in interest expense during Q2 of FY 2016

compared to Q2 of FY 2015, the company reported $81

million more in integration costs related to these

acquisitions. On a positive note, non-GAAP earnings

per share grew from $1.32 from $1.22 in the prior year

period, which exceeded investors’ expectations. Prior to

Q1 & Q2 of FY 2016, CVS Health has surpassed earnings expectations 17 out of last 18 periods with an average

earnings surprise of 15.92%. Our sector has forecasted EPS of $5.08 in FY 2016 (9.7% YoY growth) and $6.18 in FY

2017 (21.7% YoY growth). CVS Health has shown the ability to consistently grow earnings and we are very bullish that

the company will continue to do so going forward as it continues to expand and see success in both of its segments.

8. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 8

Free Cash Flow

Nike expects to grow its Free Cash Flow, or FCF, at a faster pace compared to net income over the next five years

through fiscal 2020. In fiscal 2015, FCF grew by ~74%, compared to the 21.5% growth in net income. The growth in

FCF has been supported by Nike’s expanding margins, and a slight fall in capital expenditure relative to sales.

Shareholder Return

Nike currently has a dividend yield of 1.27%. The company paid $266.4 million of cash dividends as of Q3 2016, with

quarterly payments of $.16 per share spanning back to the first quarter of 2016. As of November 19, 2015, the company

approved a four-year repurchase program of shares worth $12 billion, in addition to a 2-for-1 stock split for class A and

class B shares. Since the stock split will not have any effect on the company’s equity, the repurchasing of shares signifies

the increase in value of remaining shares, thus boosting the potential of higher returns for investors and shareholders.

Debt

As of May 31, 2016, Nike has a total debt outstanding of $9.14 billion, an

increase of 2.8% YoY from $8.89 billion in FY 2015. The change in

Nike’s total debt illustrates the rise of long-term debt as the company

sold more 10- and 30-year corporate bonds, thus increasing from $1.08

billion in FY 2015 to $2.01 billion. Short-term debt, on the other hand,

eventually decreased from $6.33 billion in FY 2015 to $5.36 billion. Nike

has debt principle payments of $500, $1000, $500, $1000, and $500

million due in 2023, 2026, 2043, 2045, and 2046 respectively. The

company also has a $2 billion revolver expiring in 2020. Overall, its Debt

to Equity (D/E) ratio holds at 74.5% as of FY 2016, along with the S&P

credit rating of AA-, well above investment grade.

VALUATION

Peer Group Analysis

The competitor gaining the most ground as of 2015 is Under Armour. The company is actively pursuing lucrative U.S.

sponsorship deals similar to Nike’s, giving it a growing piece of market revenue. In Europe, Adidas is developing new

products to compete head to head with the giant. Chinese companies Anta and Li Ning show a steady increase in sales

within China. Nike's goal is to grow its annual revenues to $50 billion by 2020. It intends to accomplish this by

significantly increasing its direct sales and e-commerce revenues in developed markets. The company also sees significant

growth opportunities in China and in its women-focused product lines.

Adidas expects to grow its top-line revenue by 15% annually through 2020. It plans to create this growth through

investments to increase its speed of new products to market, which will allow the company to adapt more quickly. It also

intends to invest strategically in marketing in growing urban cities across the globe, as the company recognizes the

movement of population, particularly younger and more athletic segments of the population, to urban areas. The

company boasts a market capitalization approaching $19 billion and trailing 12-month revenues over $16 billion. The

stock ended 2015 priced around $48 per share and with a price-to-earnings (P/E) ratio just over 8. The stock ended

2015 near its 52-week high, which was approximately $50 per share. It also yields a dividend around 1.8%.

Under Armour has a market capitalization around $15.5 billion and trailing 12-month revenues of $3.6 billion. The

stock ended 2015 trading around $80 per share with a P/E ratio of approximately 40. As a younger growth-phase

company, the stock does not currently pay a dividend. the company has consistently found ways to innovate products

that penetrate mature markets. It tends to appeal to younger market segments, and it often prices its products at a

premium for its perceived quality of innovative materials and designs.

9. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 9

Undervaluation

Nike, Inc. is currently trading at 19.5% discount to the company’s average three-year forward P/E multiple of 24.21x. In

Q1 of FY 2016, Nike reported $9.1 billion in sales, a 8.3% YoY increase. Despite surpassing top line expectations,

investors began discounting Nike when it reported single-digit growth for future orders in Q1 of FY 2016. Although

sales were impressive, many analysts were concerned with Nike’s ‘future order’ numbers. Future orders are a Nike-

invented system that gets distributors to agree to future contracts for the sale of products before Nike ships it. Those

numbers were down to 5% growth worldwide and 1% in North America YoY. Analysts believe these numbers indicate

short-term growth within the company. The primary reason future orders are down being due to Nike’s decreasing

market share within footwear and apparel to competitors like Under Armour, Adidas and Lululemon Athletica Inc.

Future orders figures serve to be misleading and outdated as it is just one of many revenue streams for Nike and

therefore Nike has decided to stop reporting it after this quarter. Future orders do not take into account Nike’s direct-to-

consumer sales. The contribution from direct-to-consumer sales has been steadily rising over the past few quarters,

making up 24% of the Nike brand’s revenue in Q1 & Q2 of FY16, compared to 22% in FY15. We believe that with the

news that Nike will no longer report “future orders” this will keep analyst more optimistic about short term growth. The

combination of our valuation methodologies, strong Q1 earning results and the attractive growth of both e-commerce

and China sales solidifies our opinion that Nike is a value opportunity with favorable growth prospects.

Fair Value Calculations

To calculate a fair target price, we used two different valuation multiples/methodologies to see the various ranges of

target prices. Our sector calculated our fair value estimates using forward P/E and historical EV/EBITDA multiples.

Using consensus NTM EPS of $2.37 estimates with an average three-year forward P/E multiple of 24.21x we calculated

a fair value estimate of $57.38. Using consensus LTM EBITDA estimates of $13,192 million with an average one-year

historical EV/EBITDA multiple of 19.98x we calculated the fair value estimate of 56.27$. Our sector decided to derive

our target price using the company’s average three-year forward P/E multiple of 24.21x, which calculates a fair value of

$57.38, implying Nike Inc. is trading 18.21% below its intrinsic value.

10. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 10

APPENDIX

Exhibit I: Three-year price graph

Exhibit II: Three-year historical and forward P/E

11. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 11

Exhibit III: Three-year historical and forward EV/EBITDA

12. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 12

DISCLAIMER

This report is prepared strictly for educational purposes and should not be used as an actual investment guide.

The forward looking statements contained within are simply the author’s opinions. The writer does not own any

Nike stock.

TUIA STATEMENT

Established in honor of Professor William C. Dunkelberg, former Dean of the Fox School of Business, for his

tireless dedication to educating students in “real-world” principles of economics and business, the William C.

Dunkelberg (WCD) Owl Fund will ensure that future generations of students have exposure to a challenging,

practical learning experience. Managed by Fox School of Business graduate and undergraduate students with

oversight from its Board of Directors, the WCD Owl Fund’s goals are threefold:

Provide students with hands-on investment management experience

Enable students to work in a team-based setting in consultation with investment professionals.

Connect student participants with nationally recognized money managers and financial institutions

Earnings from the fund will be reinvested net of fund expenses, which are primarily trading and auditing costs

and partial scholarships for student participants.