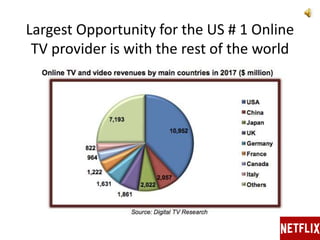

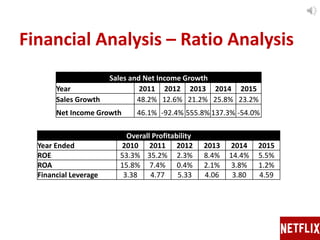

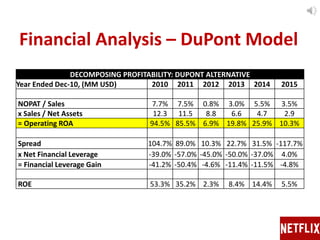

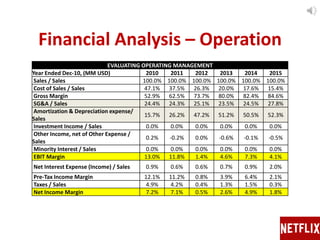

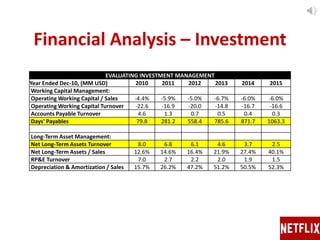

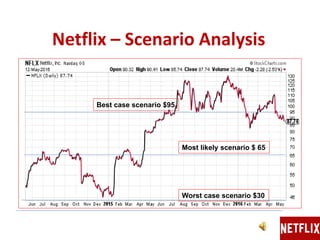

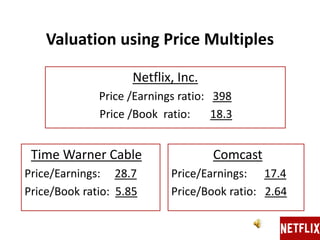

Netflix is the leading online TV provider with 75 million subscribers globally and a competitive strategy focused on content differentiation and customer preference analytics. The company's market position faces challenges from increased competition, rising costs, and negative cash flows, prompting a sell rating with a fair value estimate of $65 per share. Despite previous high profitability, Netflix's stock trades at a premium that may not be sustainable as it expands internationally and confronts a competitive landscape.

![Getting Started with Apache Spark: Big Data Made Simple [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/apachesparkgettingstarted-260203175547-8361bcc3-thumbnail.jpg?width=640&height=640&fit=bounds)