Download to read offline

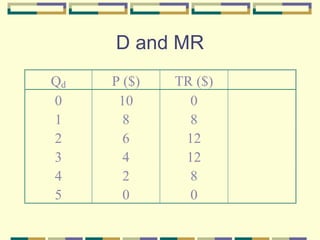

A monopoly is a market structure with a single firm that produces all output and faces no close substitutes. Barriers to entry such as control of raw materials, economies of scale, patents/copyrights, and legal restrictions prevent other firms from entering the market. A monopolist chooses its profit-maximizing quantity where marginal revenue equals marginal cost and charges the highest price consumers are willing to pay for that quantity. While monopoly may encourage innovation, it results in deadweight loss from producing less output than would be produced under perfect competition.

![What Is Blockchain Technology A Simple Beginner’s Guide [2026]](https://cdn.slidesharecdn.com/ss_thumbnails/whatisblockchaintechnologyasimplebeginnersguide2026-260101112141-cf432b44-thumbnail.jpg?width=640&height=640&fit=bounds)