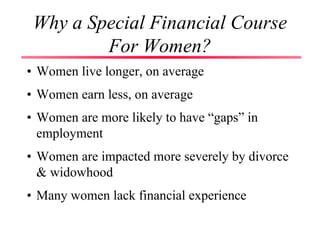

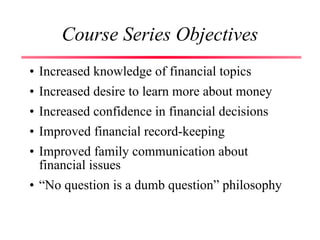

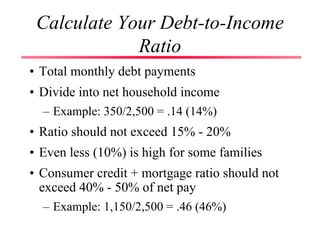

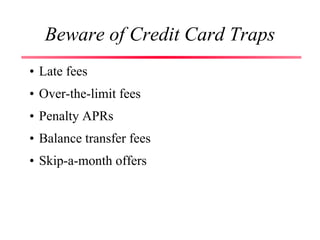

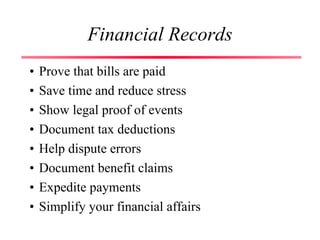

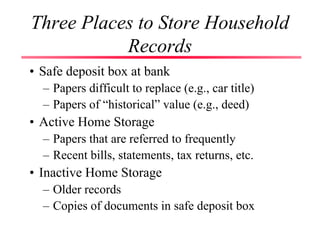

This document provides an overview of the first session of a financial education series for women. It discusses why such a course is beneficial for women, as women on average live longer but earn less and are more impacted by life events like divorce. The course objectives are to increase financial knowledge, confidence, and family communication around money. The session covers topics like understanding one's relationship with money, setting SMART financial goals, assessing financial fitness, managing cash flow, calculating net worth, smart borrowing tips, and financial record-keeping. Participants are encouraged to discuss their personal money values and financial goals.