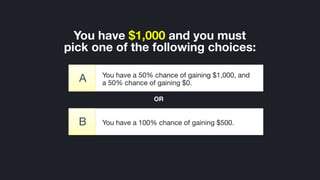

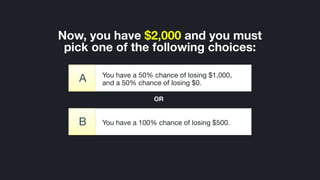

This document provides a summary of key concepts in personal finance. It begins with caveats that personal finance is poorly covered in education but has a massive impact. It then outlines five fast finance basics: 1) understanding behavioral finance biases, 2) valuing liquidity, 3) the importance of cash flow, 4) the power of compounding returns, and 5) that good investing is boring through low-cost index funds. The document provides examples and explanations for each of these high-level concepts in personal finance.