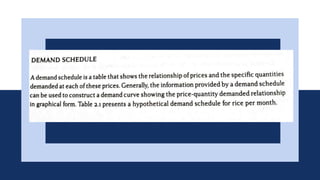

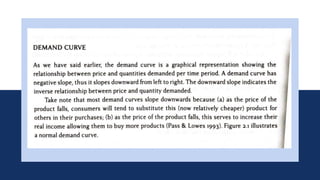

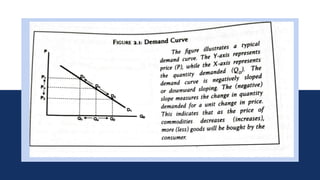

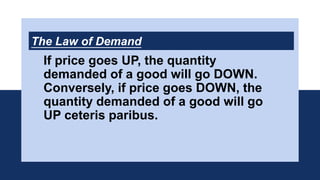

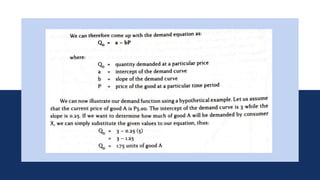

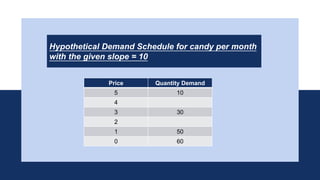

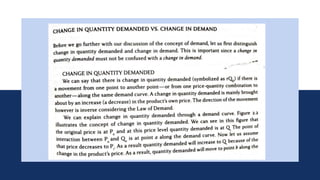

This document discusses the basic concepts of demand and supply analysis. It defines a market as where buyers and sellers meet. It explains the law of demand, which states that if price increases, quantity demanded decreases, and vice versa. It also discusses demand and supply schedules and curves, and how market equilibrium occurs when quantity demanded equals quantity supplied. Forces that can shift demand and supply such as income, tastes, prices of substitutes, and technology are also outlined.