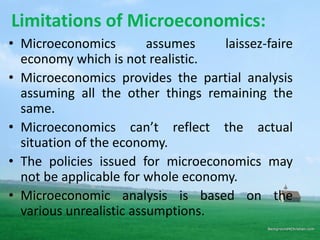

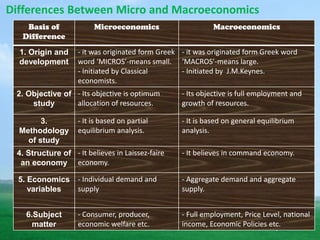

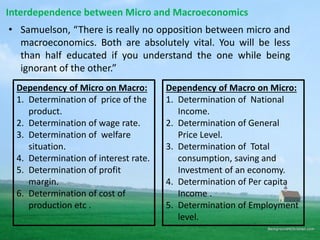

This document provides an introduction to microeconomics, including its definitions, scope, and the differentiation between micro and macroeconomics. It outlines key concepts such as positive and normative economics as well as various methodologies like deductive and inductive analysis. The document also discusses the historical development of economic thought and highlights the practical applications and limitations of microeconomics.