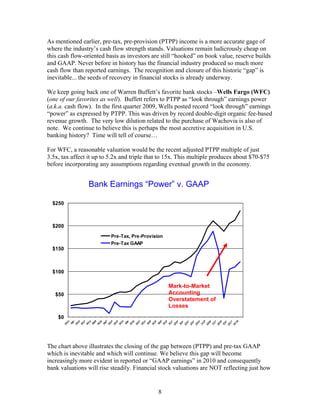

Download to read offline

The Western Reserve Master Fund rose significantly in Q1 2010, outperforming benchmarks. As of late April, the fund's year-to-date return was 40.1%. The document discusses Charles Mackay's 19th century book on economic bubbles and irrational behavior. It argues the recent financial crisis would make a good addition to Mackay's work. Several bank stocks, including Citigroup, are highlighted as attractive long investments due to inaccurate fair value accounting and an improving credit outlook.

![How to launch a event ticketing sales business on mobile [Part 5 - Mobile media]](https://cdn.slidesharecdn.com/ss_thumbnails/5-140128020612-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)