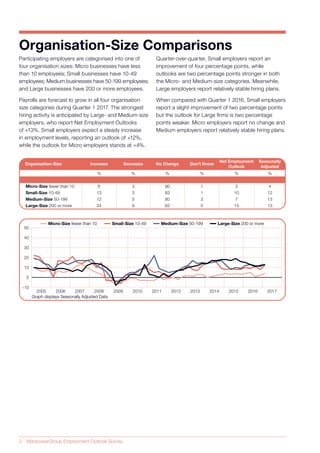

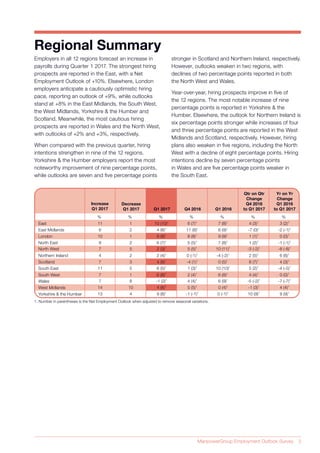

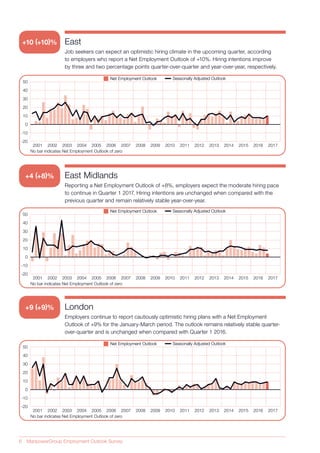

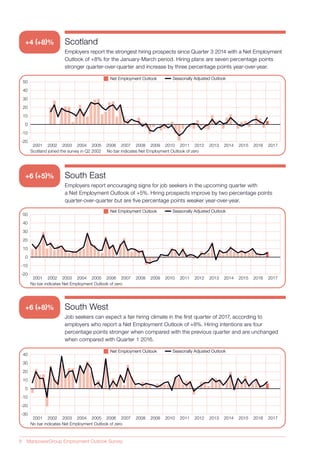

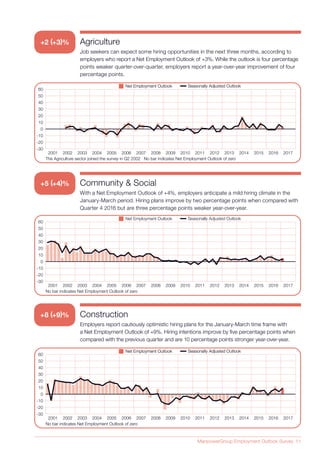

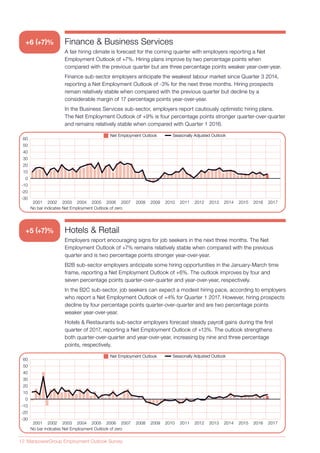

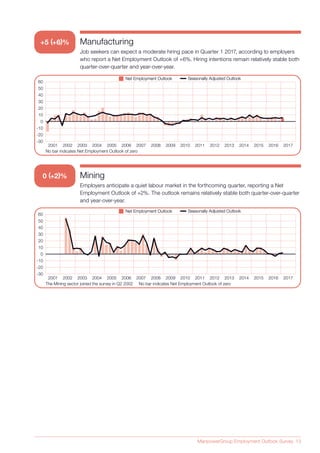

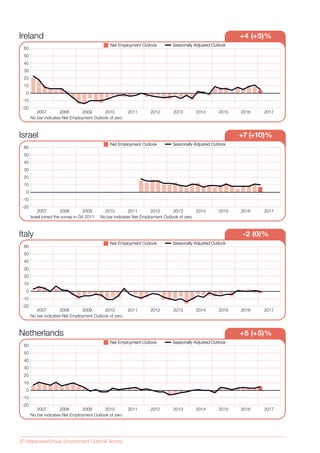

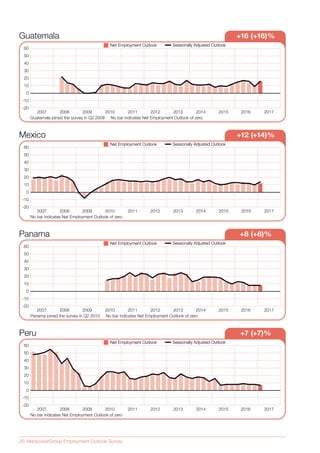

UK employers expect modest hiring activity in the upcoming quarter, with a Net Employment Outlook of +6%. The survey interviewed over 2,000 employers and found that 9% expect to increase staffing levels, 3% expect decreases, and 87% expect no change. Hiring prospects are strongest in the East region and several industry sectors, including utilities, while they are weakest in Wales and the transportation sector.

![Meos Q4 2010[1]](https://cdn.slidesharecdn.com/ss_thumbnails/meosq420101-12838654389617-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![User Experience Design [UXD]](https://cdn.slidesharecdn.com/ss_thumbnails/userexperiencedesign-130313135915-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)