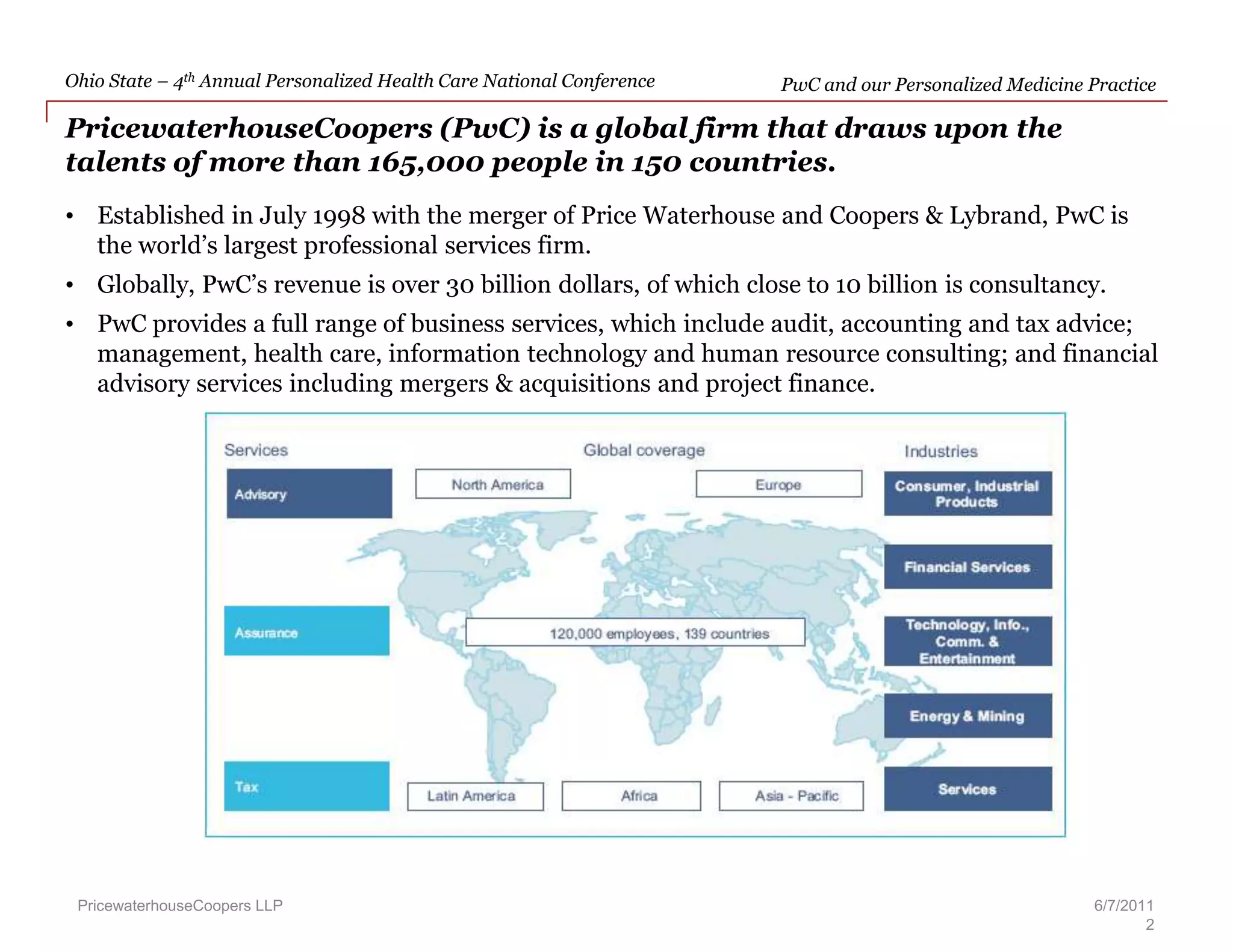

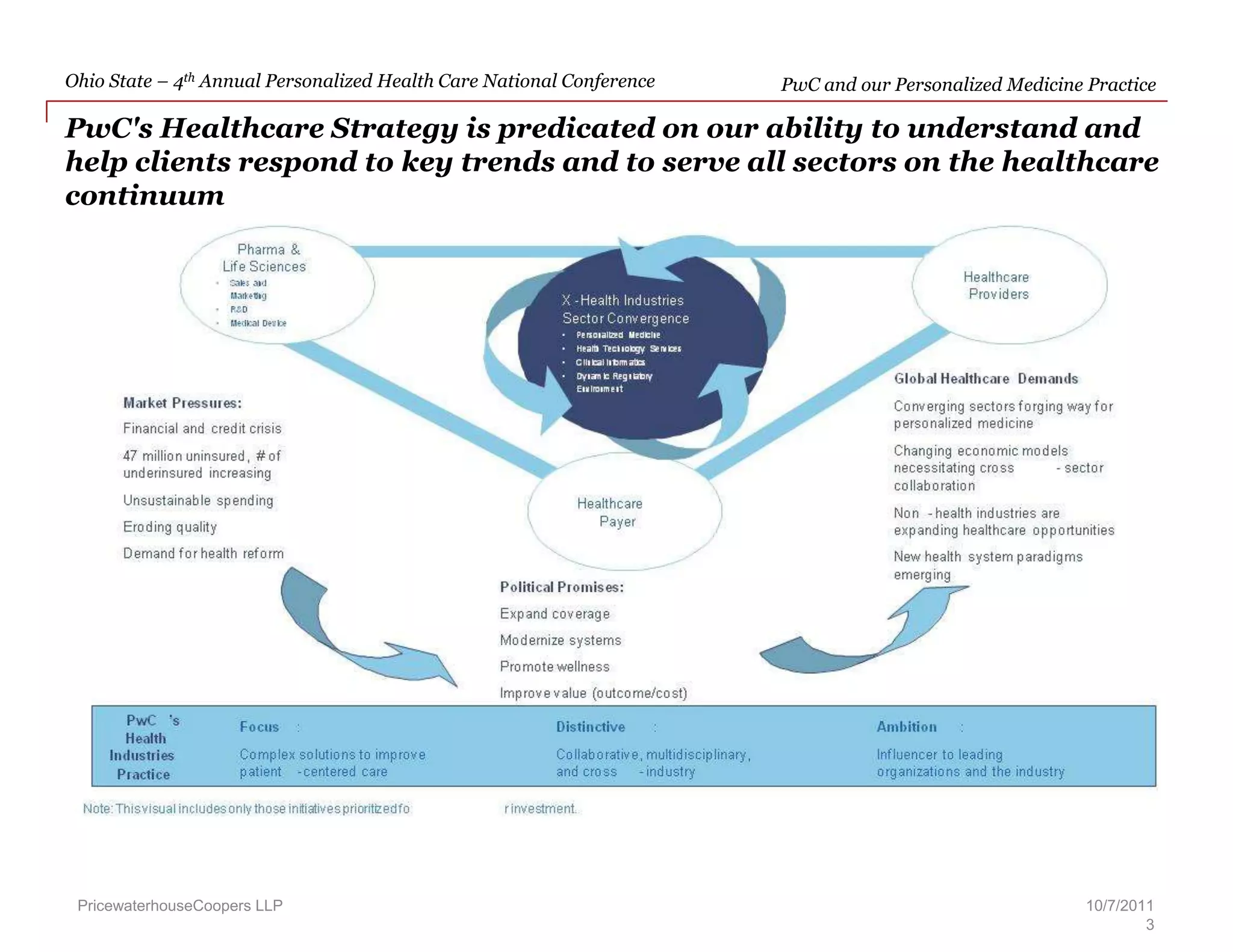

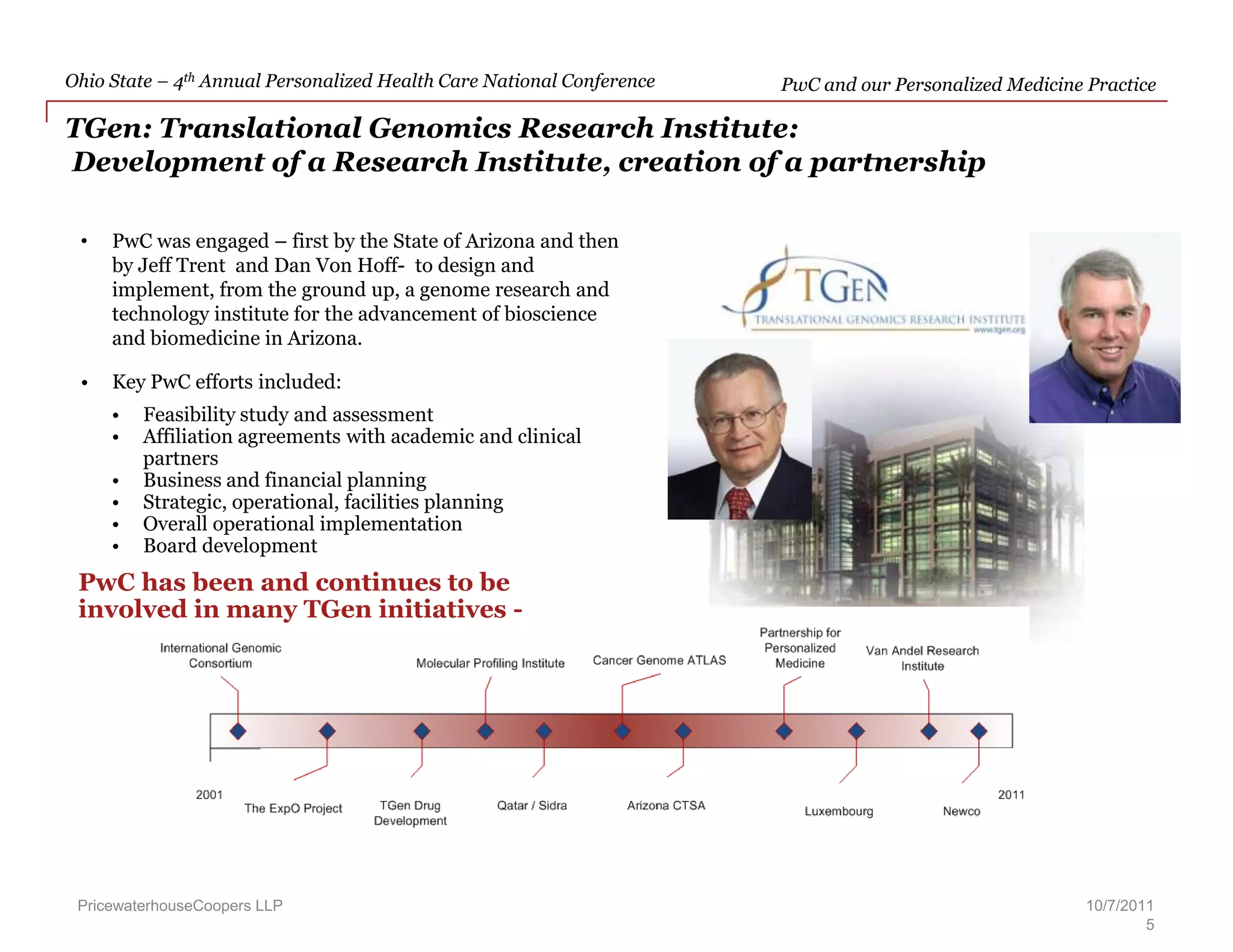

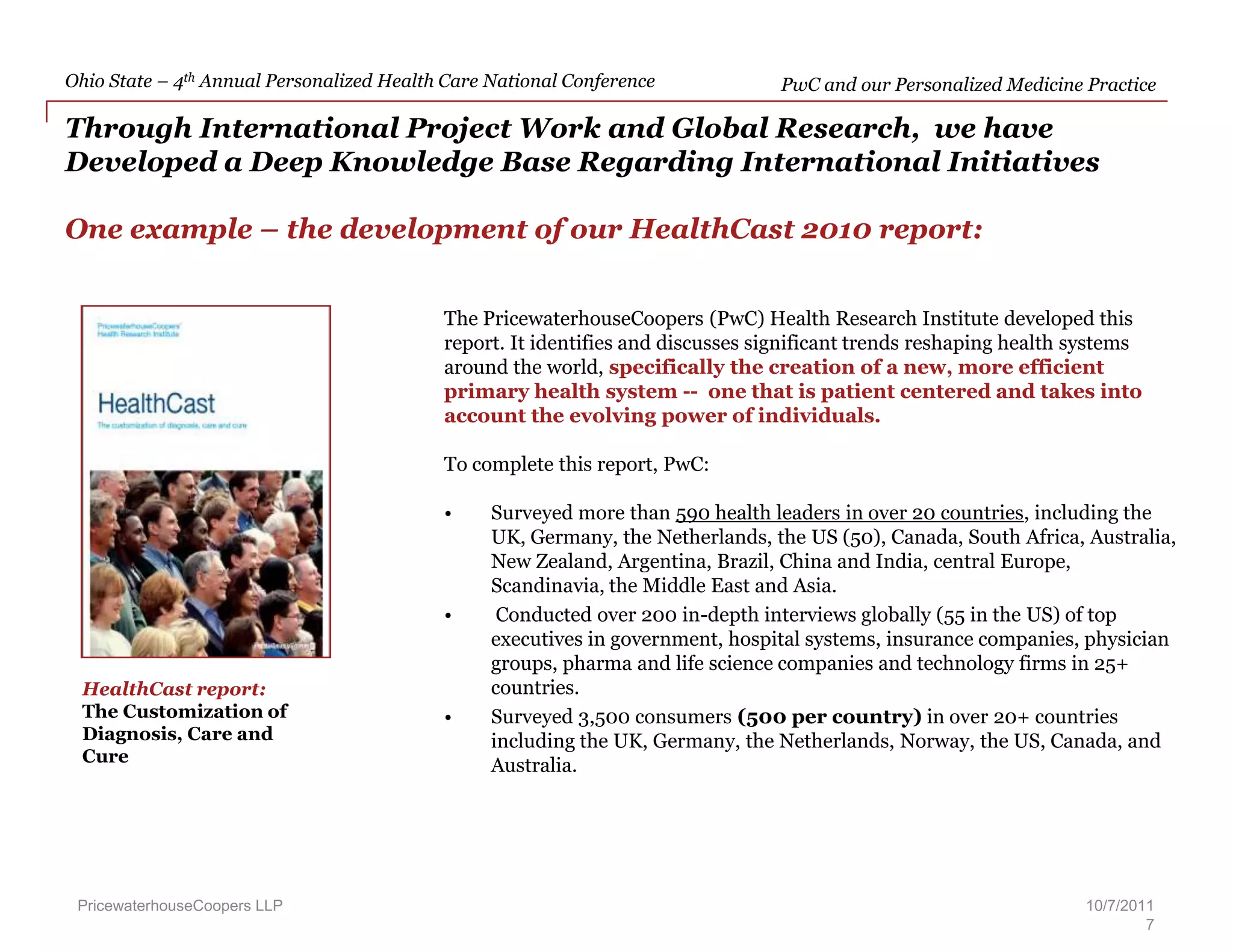

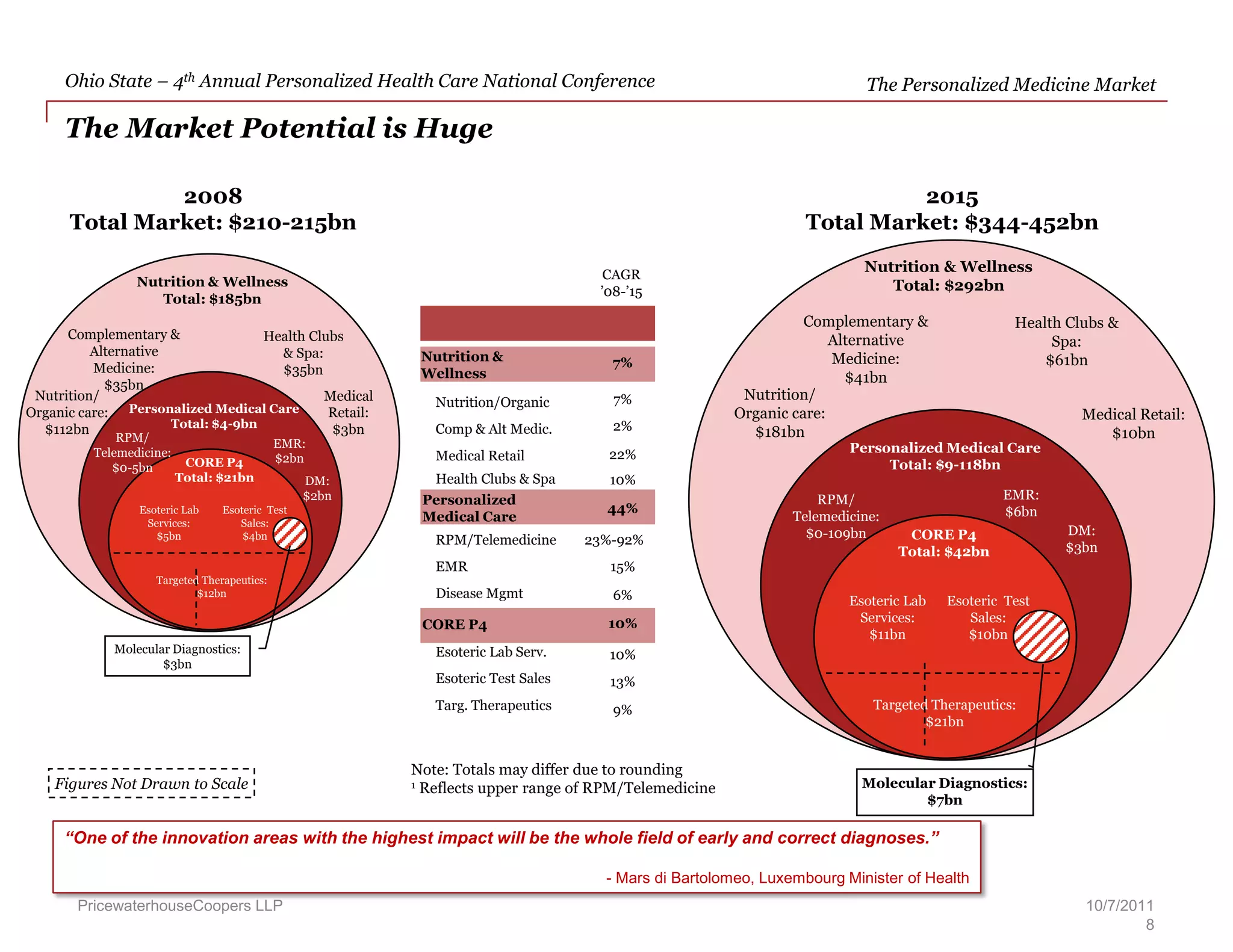

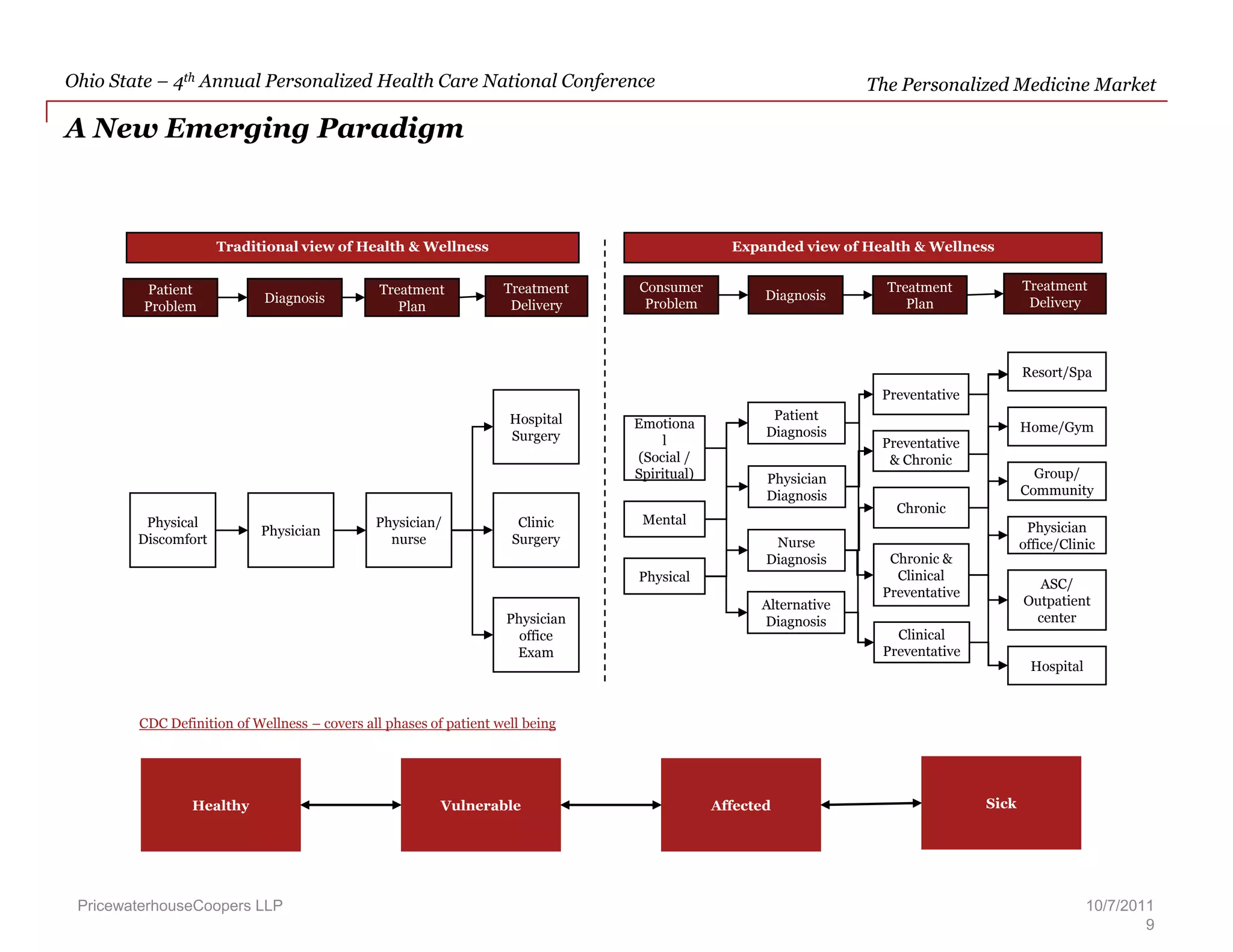

PwC is a global professional services firm that provides audit, tax, and consulting services. It has established a Personalized Medicine practice to help clients respond to trends in personalized healthcare. PwC has worked on several initiatives involving personalized medicine, including establishing a genome research institute in Arizona and facilitating partnerships between institutions in the US and Luxembourg to advance bioscience research. PwC utilizes surveys, interviews, and research to develop reports on trends in healthcare, including the growth of personalized medicine.

![Apporach to lung biopsy [Auto-saved].pptx latest](https://cdn.slidesharecdn.com/ss_thumbnails/apporachtolungbiopsyauto-saved-251211225655-93258539-thumbnail.jpg?width=640&height=640&fit=bounds)