Download as PDF, PPTX

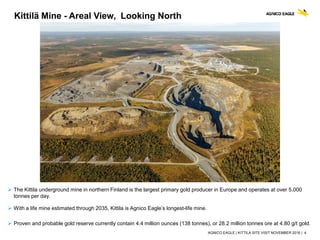

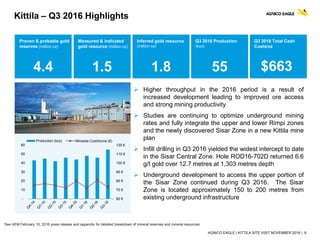

The document provides an overview of Agnico Eagle's Kittila mine site visit in November 2016. Some key points: - Kittila is Agnico Eagle's largest gold mine in Europe and has estimated reserves to continue operations through 2035. - Underground development and mining rates are being optimized to fully access the Rimpi and newly discovered Sisar zones. - Drilling in Q3 2016 yielded the widest intercept to date in the Sisar Central Zone of 6.6 g/t gold over 12.7 metres. - The processing plant uses pressure oxidation in an autoclave to treat the refractory gold ore, followed by milling, flotation, leaching and electrowin