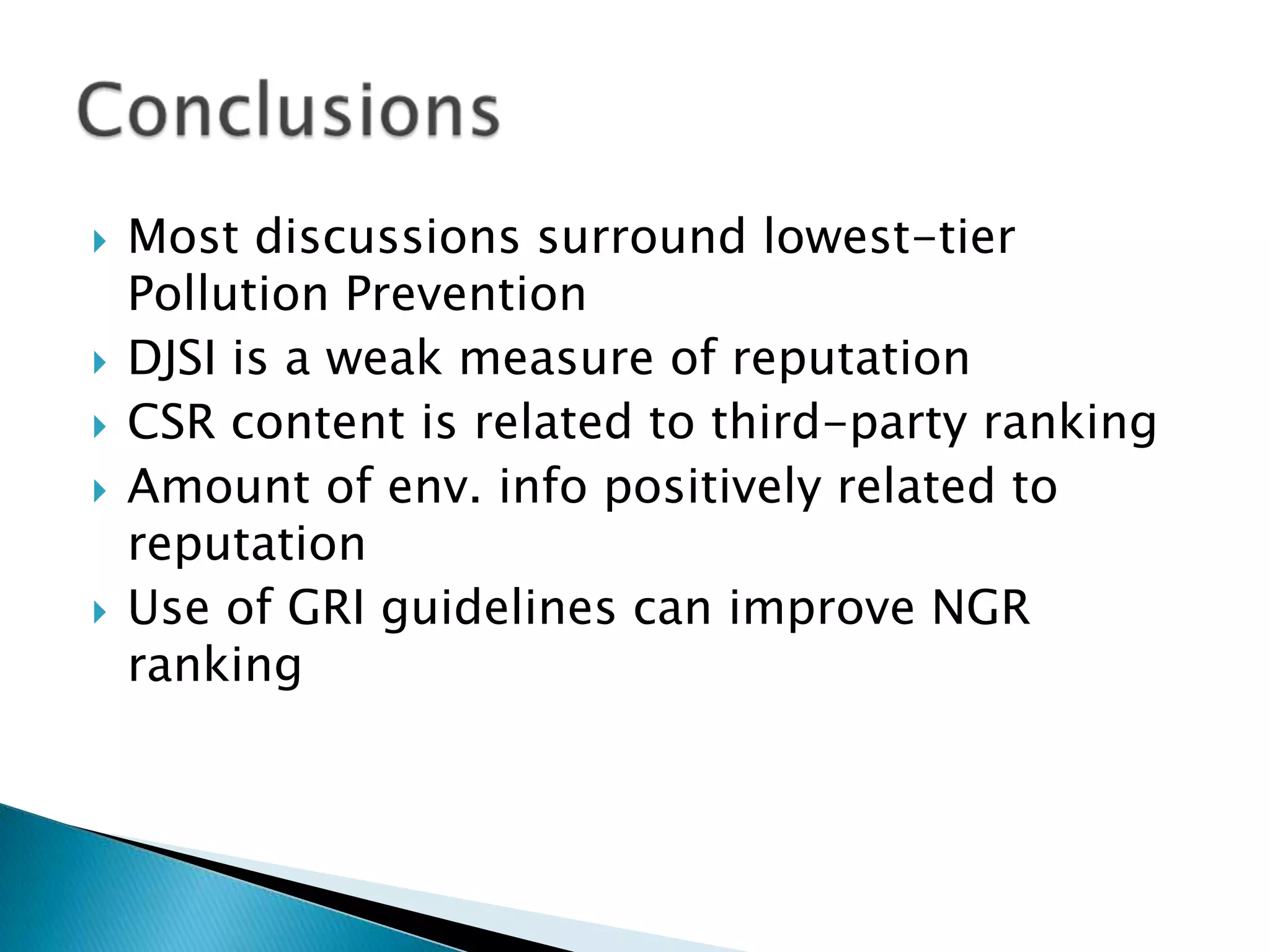

This document analyzes the impacts of sustainability report content and standardization on firm reputation. It finds that:

1) Firms that report more sustainability activities are seen as more reputable, though reputation and legitimacy are not yet fully institutionalized.

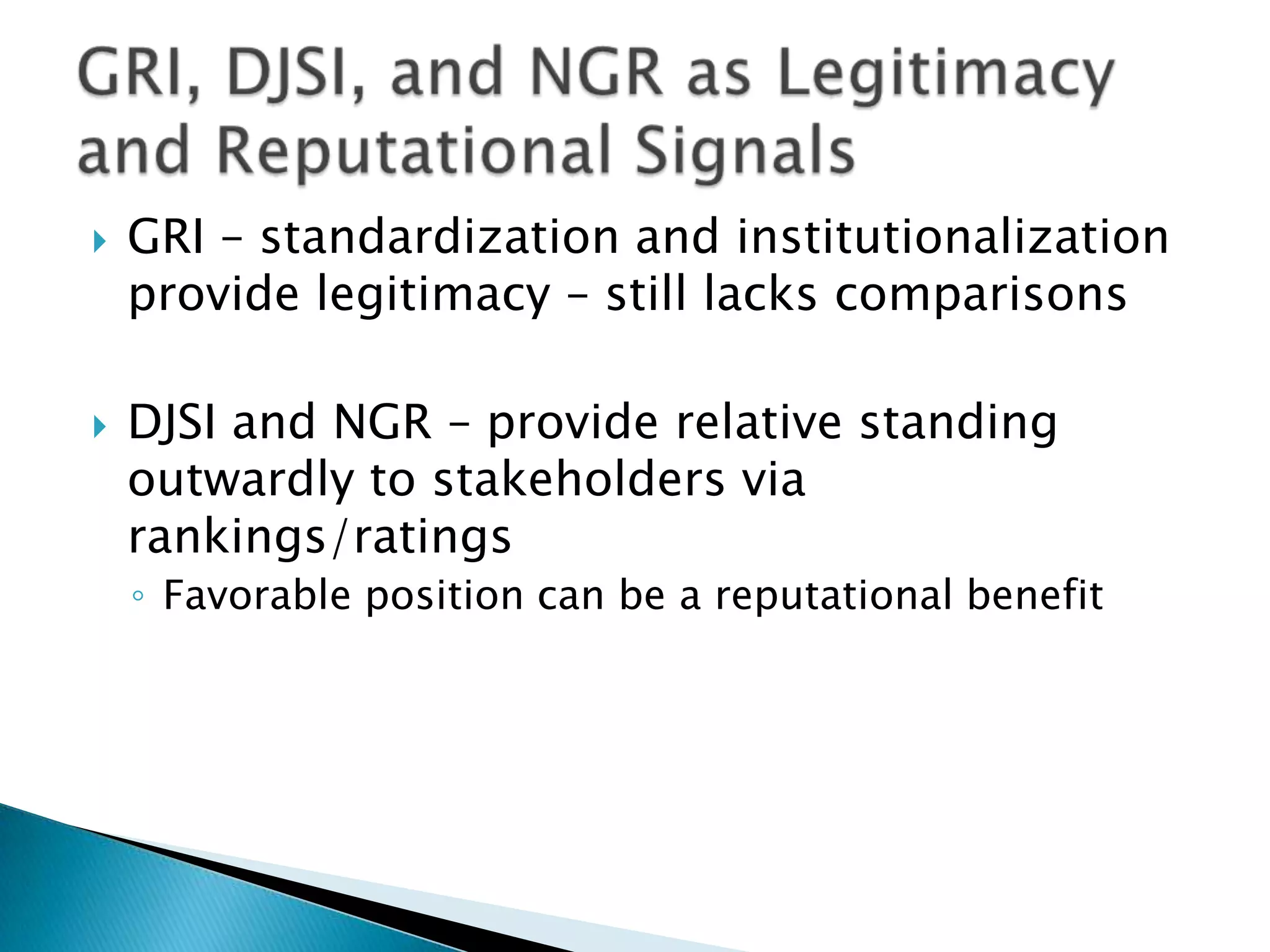

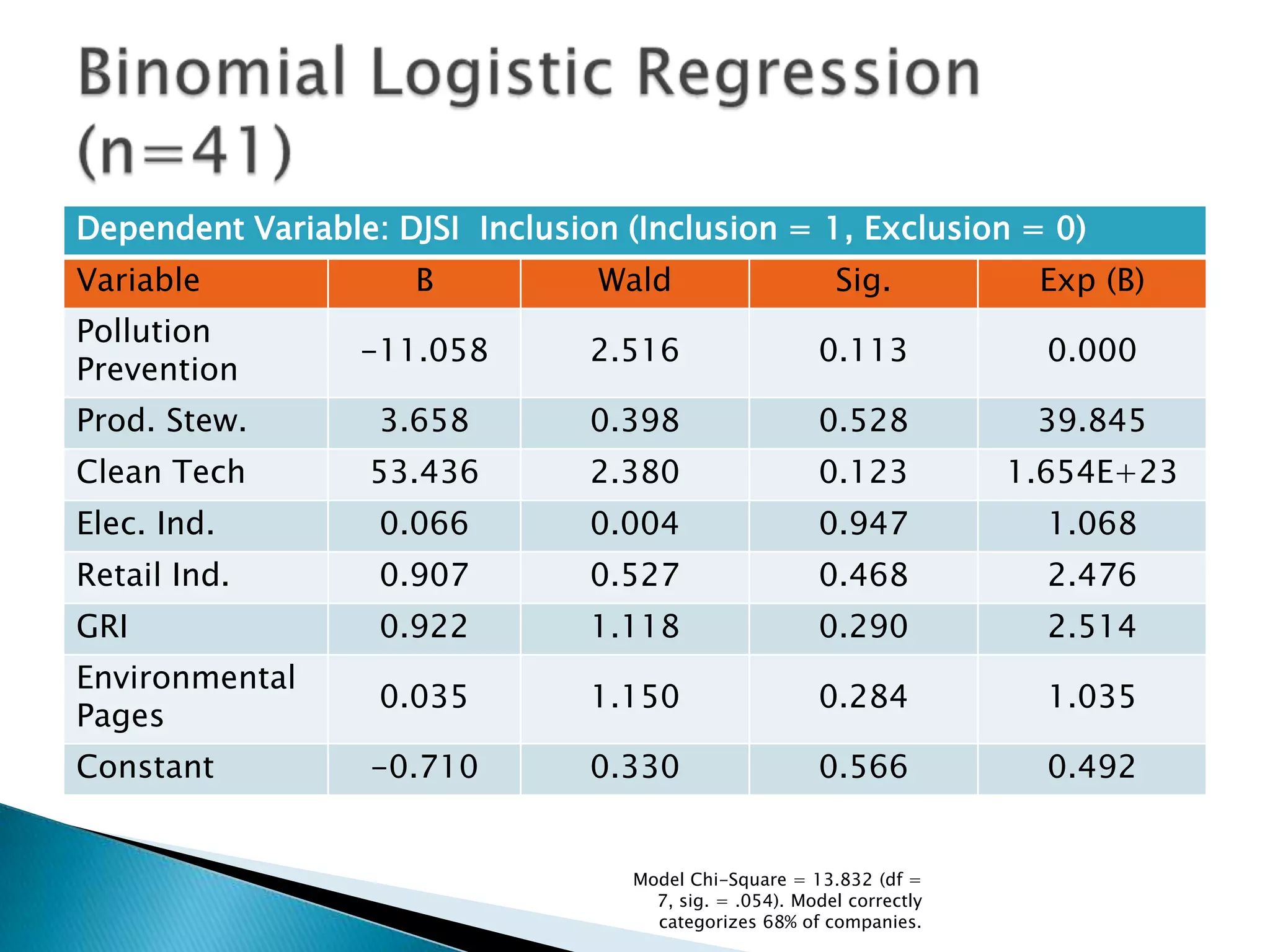

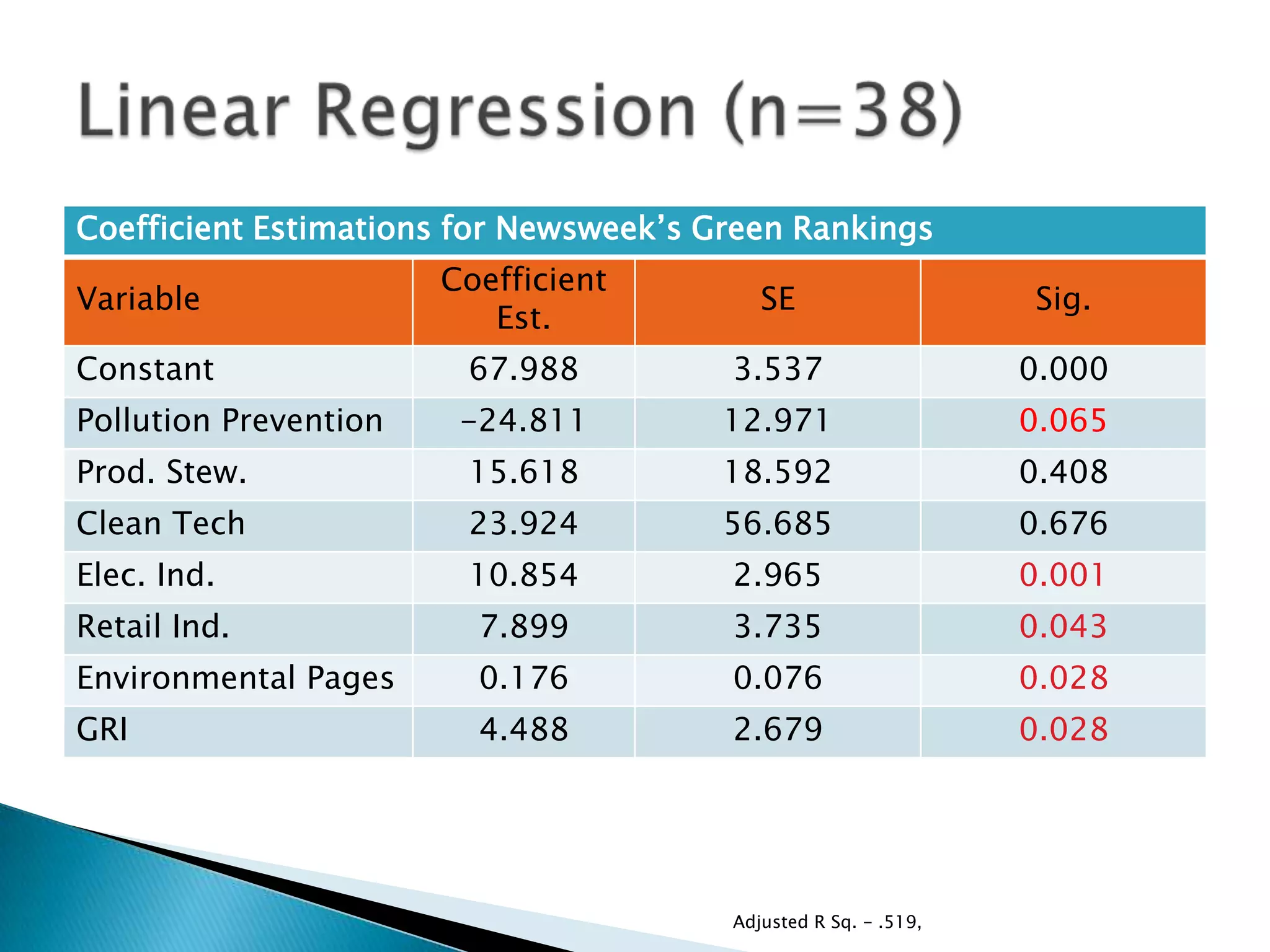

2) Firms conforming to standards like the Global Reporting Initiative guidelines can improve their rankings on third-party sustainability indexes.

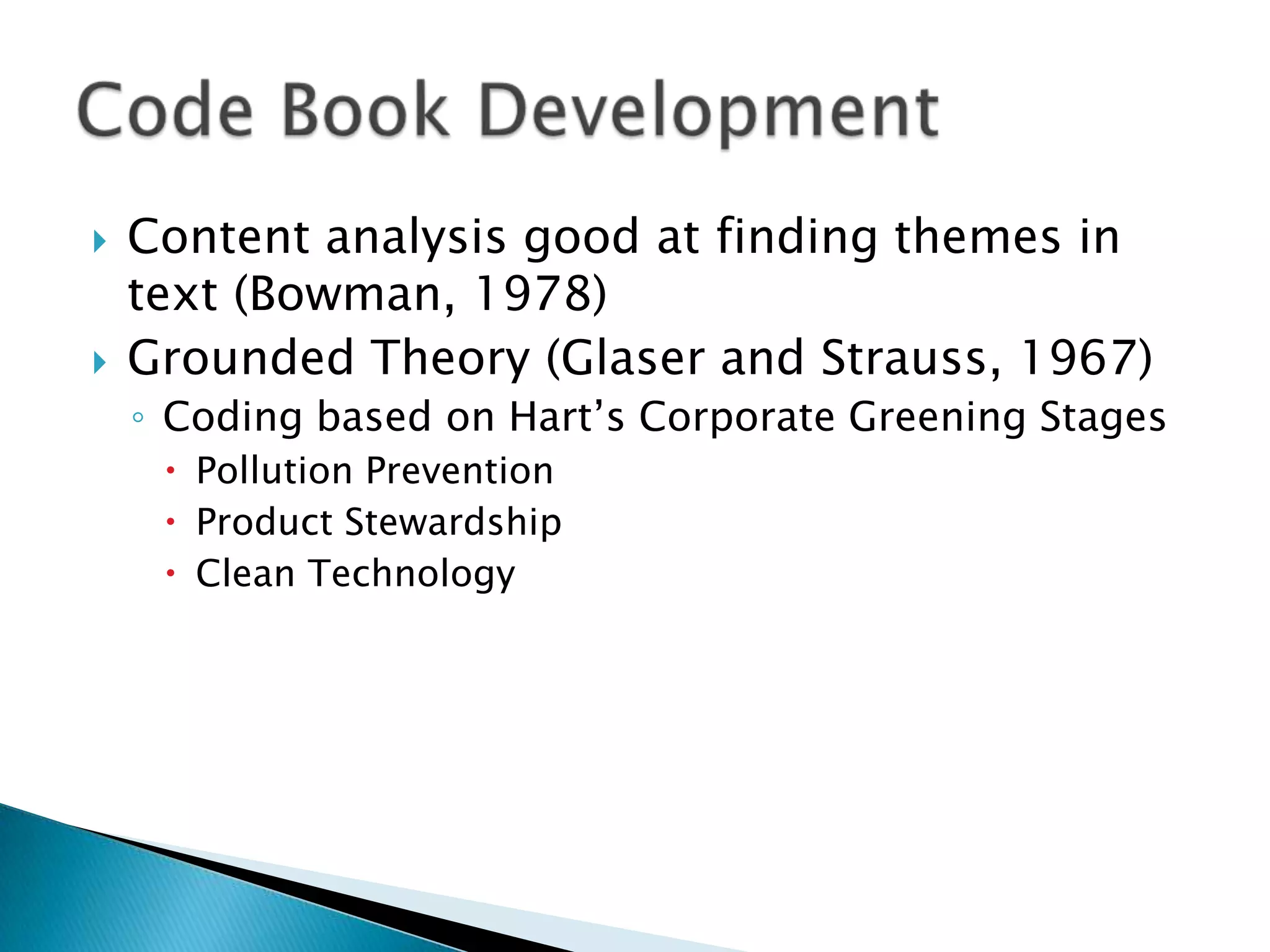

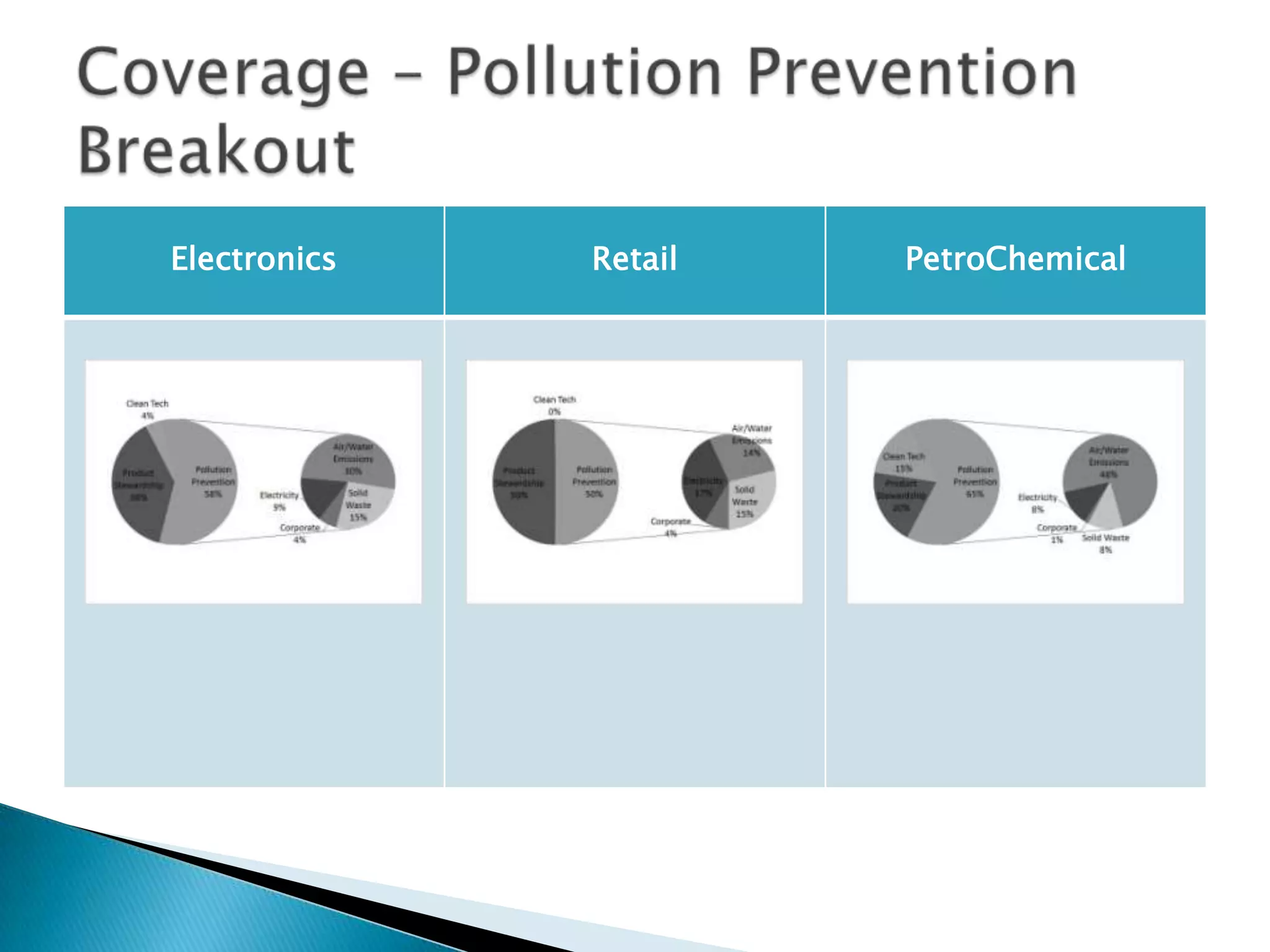

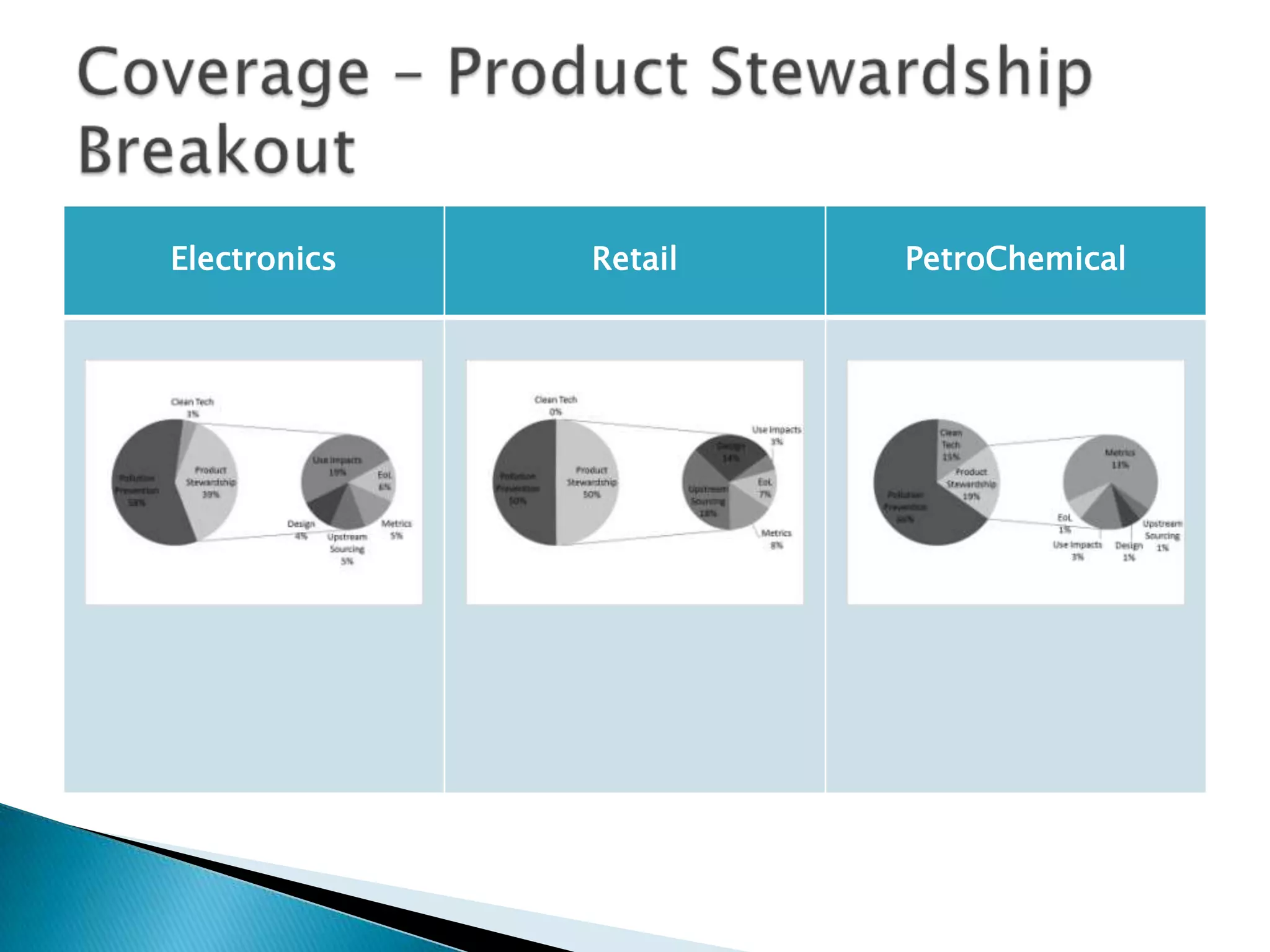

3) The amount of environmental information disclosed in reports is positively correlated with firm reputation, but most companies only discuss basic pollution prevention practices rather than more advanced strategies.