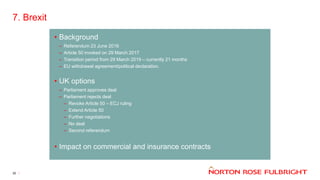

![4. Damages for Late Payment of Claims

22

The Old Law

• “Hold harmless” principle

• No “damages on damages”

• Sprung v Royal Insurance (UK)

Ltd [1999] 1 Lloyd’s Rep IR 111

The New Law

• Applies to all contracts of

(re)insurance written on or after 4

May 2017

• Implied term of every insurance

contract that Insurers

must pay any sums due in

respect of the claim within a

“reasonable time”](https://image.slidesharecdn.com/marineinsuranceseminar2-ppt-181130094724/85/Marine-Insurance-seminar-22-320.jpg)

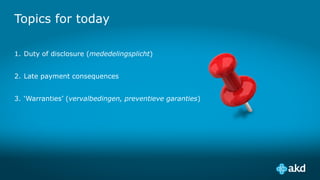

![4. Damages for Late Payment of Claims

24

Consequences of a Breach

• Insured may have a claim

for damages

• Insured would need to establish:

– Actual loss suffered

– Causation

– Loss was foreseeable (Hadley v

Baxendale [1854] 9 Ex 341)

– Reasonable steps taken to mitigate

the loss

Disputed Claims

• Reasonable grounds?

• Insurers’ conduct](https://image.slidesharecdn.com/marineinsuranceseminar2-ppt-181130094724/85/Marine-Insurance-seminar-24-320.jpg)

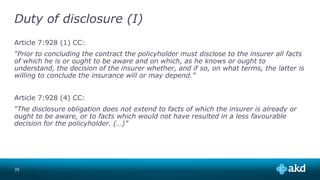

![5. Fraudulent Claims – what are they?

27

Definition

False representation made:

• in the knowledge that it is false; or

• without belief in its truth; or

• recklessly, careless as to whether

it is true or false

• Derry v Peek [1889]

Types of Fraudulent Claim

• Fabrication of entire claim

• Exaggeration of genuine claim

• “Fraudulent device”?

– Claim is genuine but the insured supplies

false information in support.](https://image.slidesharecdn.com/marineinsuranceseminar2-ppt-181130094724/85/Marine-Insurance-seminar-27-320.jpg)

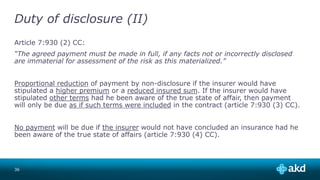

![5. Fraudulent Claims – what are they?

28

Versloot Dredging BV v HDI Gerling

Industrie Versicherung AG [2016]

UKSC 45

• Engine room flooding.

• Vessel managers alleged that the

bilge alarm had sounded.

• At first instance, this lie resulted in

forfeiture of entire claim.

• Decision upheld by Court of

Appeal.

• Supreme Court (4:1) held that the

use of a fraudulent device or

“collateral lie” to support a valid

claim did not render the claim

fraudulent.

• “The lie is dishonest, but the claim

is not”.](https://image.slidesharecdn.com/marineinsuranceseminar2-ppt-181130094724/85/Marine-Insurance-seminar-28-320.jpg)

This document provides information about an upcoming marine insurance seminar. It will include opening remarks by Pieter den Haan and presentations on English marine insurance law given by Chris Zavos and Patrick Foss from Norton Rose Fulbright LLP. Robert Hoepel from AKD Transport & Energy will give a presentation on some lessons from Dutch marine insurance law. Finally, there will be a discussion moderated by Haco van der Houven van Oordt. Contact information is provided for all the presenters.