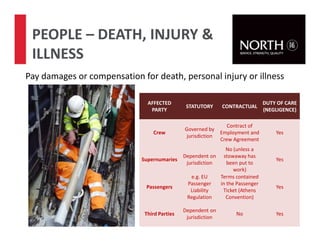

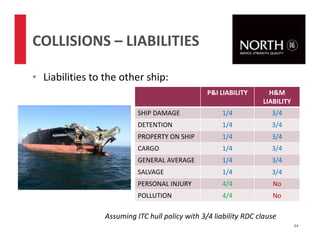

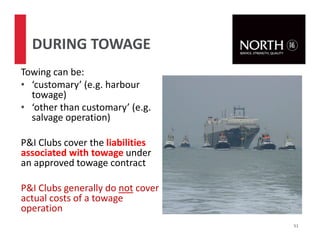

This document provides information about marine liability insurance and law courses offered at Newcastle University in October 2017 and January 2018. It includes the course modules, lecture and tutorial dates, assignment due dates, and exam information. The document also summarizes the key types of marine insurance including Hull and Machinery (H&M) Insurance, Protection and Indemnity (P&I) Insurance, and Freight, Demurrage and Defense (FD&D) Insurance. It describes the risks each covers and obligations of shipowners.