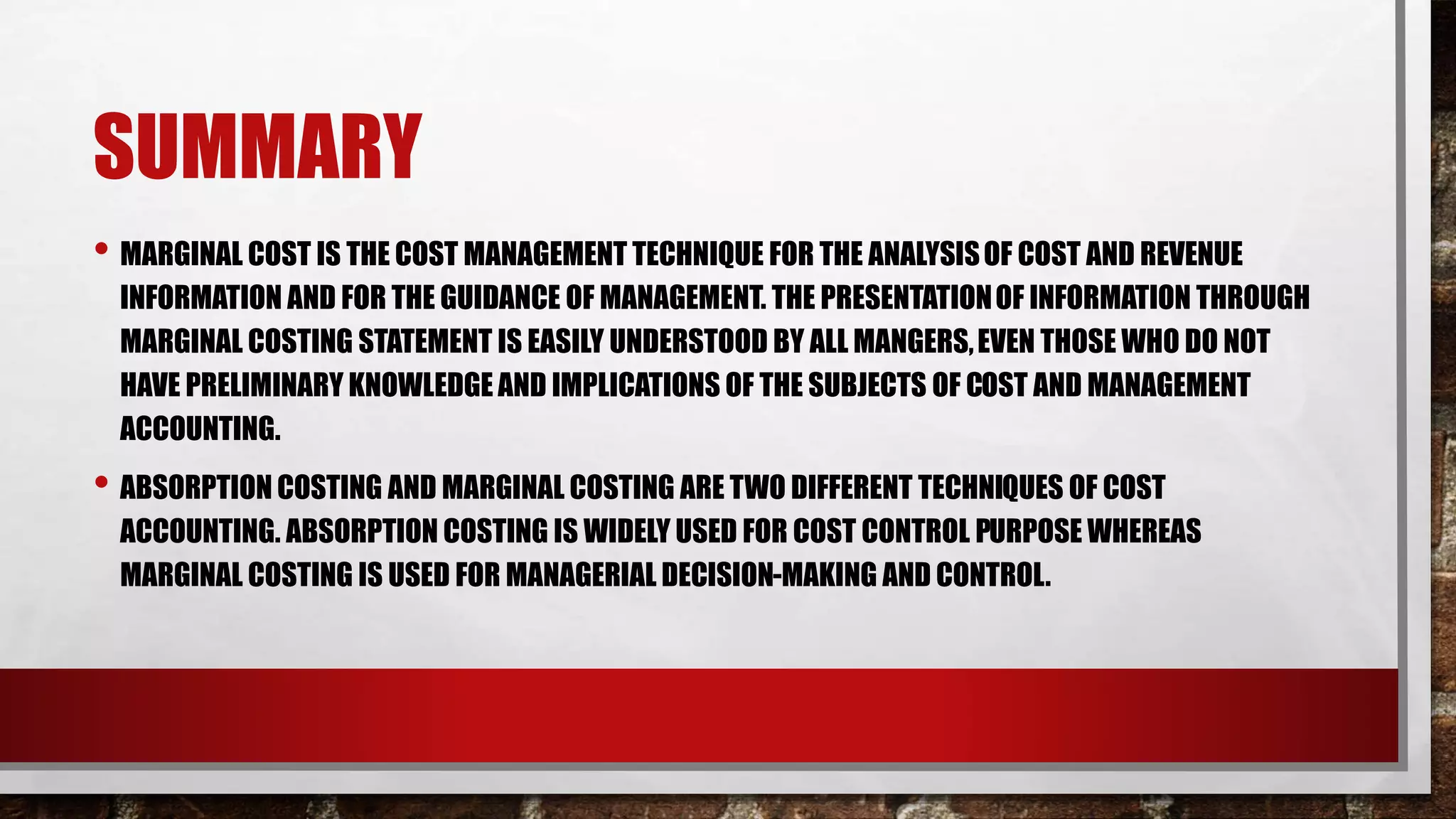

This document compares and contrasts marginal costing and absorption costing techniques. It defines marginal costing as a method that treats variable costs as product costs and fixed costs as period costs, while absorption costing treats both fixed and variable costs as product costs. The document outlines the key differences between the two methods in how they calculate cost per unit, treat opening and closing inventory costs, measure profitability, and classify overhead costs. It also provides examples of the different report formats used for marginal costing and absorption costing statements.