Download as PDF, PPTX

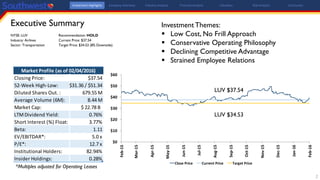

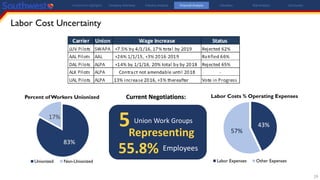

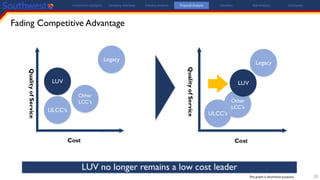

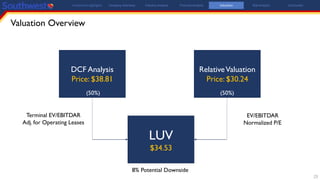

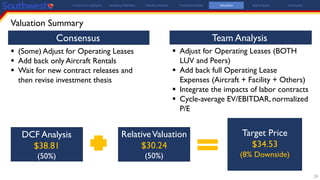

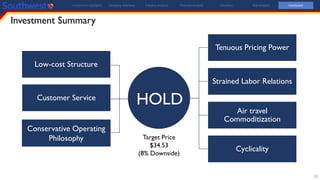

Southwest Airlines has a current stock price of $37.54 per share and the analyst assigns a target price of $34.53, representing an 8% downside. While Southwest once had a competitive advantage due to its low cost structure, this advantage has diminished as other carriers have improved their own cost efficiency. Employee relations have also become strained as the company negotiates new contracts with five unionized work groups. Despite recent fuel cost savings, the analyst believes Southwest's fading competitive position and labor uncertainties warrant a HOLD recommendation on the stock.

![UT Dallas CFA IRC Report - 2016 LUV [104644]](https://cdn.slidesharecdn.com/ss_thumbnails/1cd984f1-f2df-4149-bf66-708c92c2bf8f-160308220340-thumbnail.jpg?width=640&height=640&fit=bounds)