Local market san francisco

•

1 like•345 views

From NAR's REALTOR.org research department. A great overview of the real estate market in San Francisco.

Recommended

More Related Content

What's hot

What's hot (17)

Viewers also liked

Viewers also liked (8)

Similar to Local market san francisco

Similar to Local market san francisco (20)

More from Better Homes and Gardens Real Estate

More from Better Homes and Gardens Real Estate (20)

Recently uploaded

Recently uploaded (20)

Local market san francisco

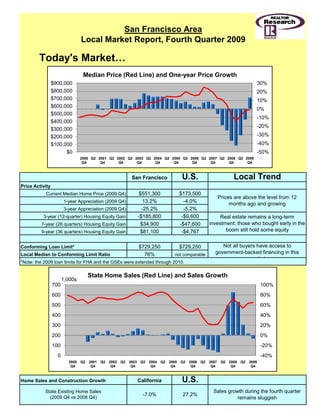

- 1. San Francisco Area Local Market Report, Fourth Quarter 2009 Today's Market… Median Price (Red Line) and One-year Price Growth $900,000 30% $800,000 20% $700,000 10% $600,000 0% $500,000 -10% $400,000 -20% $300,000 $200,000 -30% $100,000 -40% $0 -50% 2000 Q2 2001 Q2 2002 Q2 2003 Q2 2004 Q2 2005 Q2 2006 Q2 2007 Q2 2008 Q2 2009 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q4 San Francisco U.S. Local Trend Price Activity Current Median Home Price (2009 Q4) $551,300 $173,500 Prices are above the level from 12 1-year Appreciation (2009 Q4) 13.2% -4.0% g g months ago and growing g 3-year Appreciation (2009 Q4) -25.2% 25 2% -5.2% 5 2% 3-year (12-quarter) Housing Equity Gain -$185,800 -$9,600 Real estate remains a long-term 7-year (28 quarters) Housing Equity Gain $34,900 -$47,600 investment: those who bought early in the 9-year (36 quarters) Housing Equity Gain $81,100 -$4,767 boom still hold some equity Conforming Loan Limit* $729,250 $729,250 Not all buyers have access to Local Median to Conforming Limit Ratio 76% not comparable government-backed financing in this k t *Note: the 2009 loan limits for FHA and the GSEs were extended through 2010. State Home Sales (Red Line) and Sales Growth 1,000s 700 100% 600 80% 500 60% 400 40% 300 20% 200 0% 100 -20% 0 -40% 2000 Q2 2001 Q2 2002 Q2 2003 Q2 2004 Q2 2005 Q2 2006 Q2 2007 Q2 2008 Q2 2009 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Home Sales and Construction Growth California U.S. State Existing Home Sales Sales growth during the fourth quarter -7.0% 27.2% ( (2009 Q4 vs 2008 Q4)) gg remains sluggish

- 2. Drivers of Local Supply and Demand… Local Economic Outlook San Francisco U.S. Not 1-year Job Change (Dec) -77,000 Job losses are a problem and will weigh Comparable on demand, but layoffs are declining Not 1-year Job Change (Nov) -79,000 which could help buyer confidence Comparable Not 3-year Job Change (Dec) -111,300 San Francisco's unemployment situation Comparable 10.1% 10.0% is worse than the national average and Current Unemployment Rate (Dec) weighs on confidence Year-ago Unemployment Rate 7.1% 7.4% 1-year (12 month) Job Growth Rate -3.8% -4.3% Weak, but better than most markets State Economic Activity Index California U.S. The economy of California is weaker than 12-month change (2009 - Dec) -4.2% -2.2% the rest of the nation, but improved 36-month change (2009 - Dec) -4.5% -1.3% modestly from last month Local Fundamentals San Francisco U.S. 12-month Sum of 1-unit Building Permits through The current level of construction is 84.7% 2,238 not comparable Dec 2009 below the long-term average Excess supply reduction could result in Long-term average for 12-month Sum of 1-Unit price escalation over the longer-term if, in 14,622 , not comparable p Building Permits the future there is a rapid and robust future, increase in demand Single-Family Housing Permits (Dec 2009) Construction is down from last year, but -4.8% -23.7% 12-month sum vs. a year ago appears to have bottomed. Construction: 12-month Sum of Local Housing Permits (Historical Average Shown in Red Dashed Line) 30,000 25,000 20,000 15,000 10,000 5,000 0

- 3. Affordability Affordability - Local Mortgage Servicing Cost-to-Income (Local Historical Average Shown in Red, U.S. Average in Green) 40% 35% 30% 25% 20% 15% 10% 5% 0% 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 Monthly Mortgage Payment to Income San Francisco U.S. Ratio for 2008 19.6% 15.4% Historically strong and an improvement Ratio for 2009 Q4 21.6% 14.8% over the third quarter of this year Historical Average 30.1% 22.6% Weaker affordability than most markets Recent Trend - Local Mortgage Servicing Cost to Income (Historical Average Shown in Red Dashed Line) 35% 30% 25% 20% 15% 10% 5% 0% 2008 Q1 2008 Q2 2008 Q3 2008 Q4 2009 Q1 2009 Q2 2009 Q3 2009 Q4

- 4. Median Home Price to Income San Francisco U.S. Ratio for 2009 7.9 6.2 Local affordability has improved, but Ratio for 2009 Q4 8.9 6.1 could be better Historical Average 9.9 7.2 More expensive than most markets Ratio of Local Median Home Price to Local Average Income (Local Historical Average Shown in Red, U.S. Average in Green) 16.0 14.0 12.0 10.0 8.0 6.0 4.0 2.0 0.0 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 The Mortgage Market 30-year Fixed Mortgage Rate and Treasury Bond Yield (%) 3.0 7.0 6.5 2.5 6.0 2.0 5.5 5.0 1.5 4.5 4.0 1.0 3.5 0.5 3.0 2.5 0.0 2.0 2004 Q4 Q2 2005 Q4 Q2 2006 Q4 Q2 2007 Q4 Q2 2008 Q4 Q2 2009 Q4 Spread (left axis) 30-Year FRM (Right axis) 10-Year Treasury Bond (Right Axis) The spread between the 30-year fixed rate mortgage and the 10-year Treasury is now at comfortable, pre-crisis levels. However, the Federal Reserve and Treasury will stop buying mortgage backed securities (MBS) on March 31st. The agencies had been buying MBS to keep mortgage rates low. Consequently, the end of the program has some market observers concerned about a possible increase in rates. However, the Fed has slashed its purchases of MBS in recent weeks and the private sector has scooped up any remaining MBS. With yields on other investments low, the returns on the MBS, even at 5%, are desirable. The Fed has promised that it stands ready to intervene in the market, presumably by resuming purchases, in case there is a sudden increase in mortgage rates. Low mortgage rates have been critical to the improved home sales that are at the core of the housing market and economic recovery.

- 5. Looking Deeper…. State Total Foreclosure Rate vs. U.S Average (U.S. Average in Blue Dashed Line) 7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% Source: Mortgage Bankers' Association Monthly Market Data - November 2009 San Francisco U.S. 11.7 14.4 Suprime mortgages make up a larger S i t k l Market Share: % % 85.6% 88.3% than average share of the San Francisco Prime (blue) vs. 85.6 88.3 market, but rising prime foreclosures are Subprime + Alt-A % % also becoming a problem 14.4% 11.7% There was a substantial increase versus 2.2 2.2% 2.6% PRIME: 1.8 2.6% October of this year % 2.1% Foreclosure + REO % Rate Compared to the national average, 1.8% 2.1% Oct-09 Nov-09 Oct-09 Nov-09 today's local rate is low The local foreclosure rate has fallen 21.2% 18.4 18.0% SUBPRIME: 24.4 relative to last month % 21.2 % 18.0 Foreclosure + REO % % Rate The current local rate is high given the 24.4% 18.4% Oct-09 Nov-09 Oct-09 Nov-09 U.S. average Relatively little local change versus 12.7% 14.8% ALT-A: 12.7 14.8 October of this year 12.4 % 14.0 % Foreclosure + REO % % Rate The November rate for San Francisco is 12.4% 14.0% Oct-09 Nov-09 Oct-09 Nov-09 low compared to the national average The "foreclosure + REO rate" is the number of mortgages, by metro area, that are either in the foreclosure process or have completed the foreclosure process and are owned by banks divided by the total number of mortgages for that area. Source: First American CoreLogic, LoanPerformance data