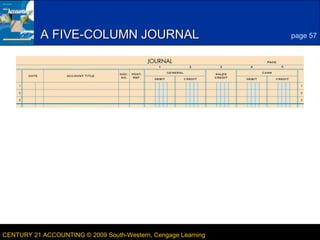

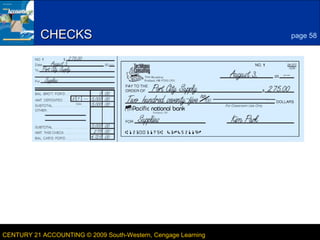

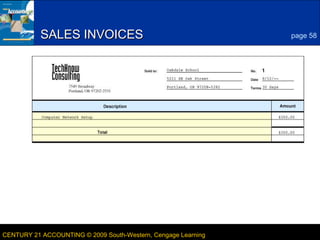

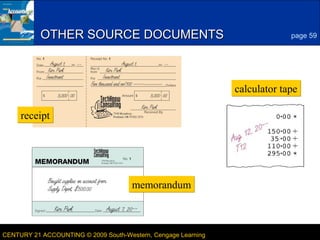

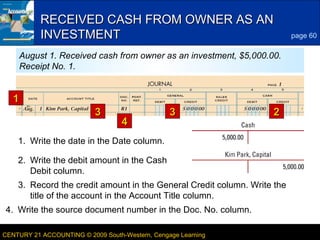

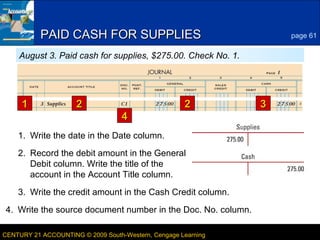

This document discusses journals, source documents, and recording entries in a journal in accounting. It describes a five-column journal and common source documents like checks, sales invoices, receipts, and memorandums. It provides an example of recording the receipt of cash from the owner as an investment in the journal, with details on filling out each column. It also demonstrates recording the payment of cash for supplies in the journal. Finally, it lists key terms discussed in the lesson like journal, journalizing, entry, source document, check, and invoice.