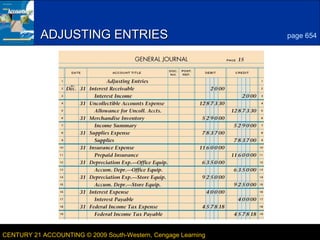

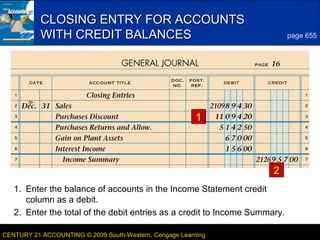

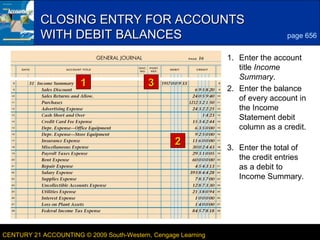

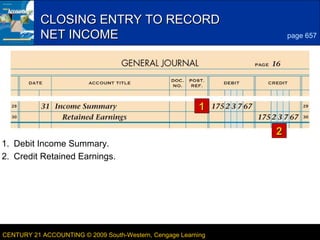

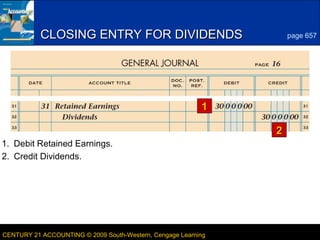

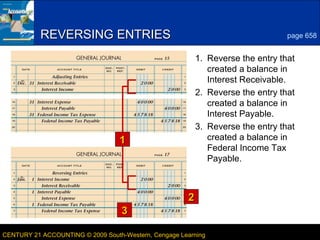

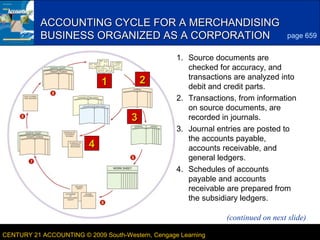

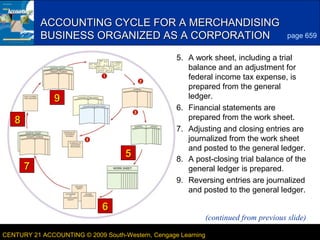

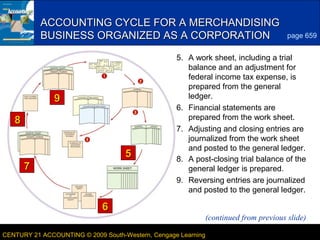

This document discusses the accounting cycle for a corporation, including adjusting, closing, and reversing entries. It explains how to close accounts with credit or debit balances, record net income, dividends, and reversing entries. The accounting cycle steps are outlined as: 1) recording transactions, 2) posting to journals and ledgers, 3) preparing a work sheet and financial statements, 4) making adjusting and closing entries, 5) preparing a post-closing trial balance, and 6) making reversing entries.

![[SAMPLE] L4 Finance for Managers PPT Task 1.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/samplel4financeformanagersppttask1-240129005404-f8b0f1f0-thumbnail.jpg?width=640&height=640&fit=bounds)