Downloaded 31 times

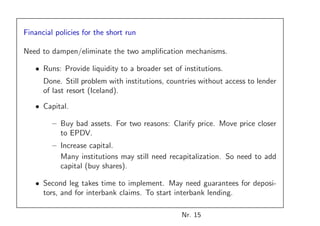

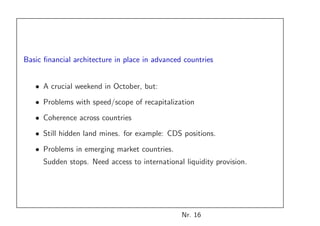

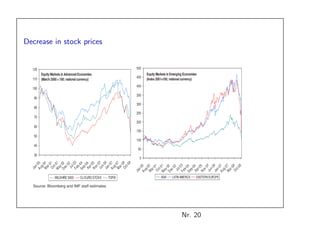

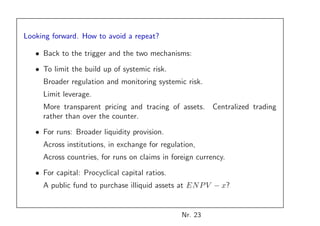

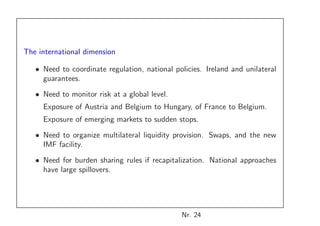

This document discusses the financial crisis that began in 2007. It describes the initial conditions that led to the crisis, including risky subprime assets and complex financial products. It then explains two amplification mechanisms: runs on financial institutions due to bad assets, and declining capital ratios. These mechanisms strongly interacted and spread contagion across institutions, assets, and countries. The document analyzes the dynamics of the crisis in real time and discusses appropriate short-run policies to address liquidity and capital issues. It also notes ongoing financial and economic challenges.